Introduction

In the 1990s, an instructional reference book series soared to fame as non-intimidating guides for readers new to various topics. As its popularity grew worldwide – to the point of attracting a cult following of “collectors” proudly displaying each edition on their bookshelf – the series expanded rapidly to around 2,500 titles available in numerous languages. Like so many other nascent businesses, an industrious mind identified a burgeoning trend and capitalized on the untapped market demand with a product geared towards evolving consumer preferences. In this case, the creators of the For Dummies franchise catapulted to instant success because they accurately presaged a world that was becoming increasingly information-rich but time-poor and then introduced a clever solution. Sadly though, its once-promising prospects would soon be thwarted by the advent of the Internet – which could offer the consumer vastly more content, instantly and free of charge. However, we argue that there is at least one use case where a comeback would be both highly impactful and enthusiastically received across the globe: Public Policy. Unlike earlier titles, the intended audience wouldn’t be the everyday novice seeking basic proficiency or a broadened skillset. Instead, Public Policy for Dummies would be targeted to the “expert class” as required reading for all current and future policymakers prior to assuming their post. We presume taxpayers would gleefully pick up the tab for funding this new program, as its relatively low cost would be more than outweighed by its overwhelming benefits. To ensure compliance and guarantee ease of comprehension, we recommend that this edition be only one page in length consisting of three easy steps:

Step 1: Recognize, accept, and acknowledge the reality of major policy issues smacking you in the face. Fight the instinct to deny their existence, downplay their risks, or silence those sounding the alarm – even if politically unpalatable.

Step 2: Do something to address the most concerning issues first, without making matters worse. If your policy ideas would exacerbate the problem, do nothing at all.

Step 3: Repeat Steps 1 & 2 (in that order).

Obviously, this proposal – a hyperbolic and overly simplistic solution to a complex problem – is intended solely as satire. It is merely our attempt at humorously underscoring the serious, real-world consequences of recent public policy action (or inaction). In our January 2022 market commentary, The Inflation Spiral Everyone Could See Coming, we discussed in detail how the current inflation cycle was easily foreseeable and not at all transitory. Had policymakers implemented any number of responsible measures at their disposal to address the looming crisis – or at least avoided aggravating an already precarious situation – the severity of inflation’s painful repercussions on consumers, workers, asset prices, and the economy could have been mitigated or potentially avoided altogether. However, after appearing to have peaked in June 2022, inflation’s significance as the primary determinant of growth prospects and in policymaking calculus should steadily subside over the next 12 months. For this reason, it is imperative that we now recalibrate our priorities from solely focusing on the short-term battle being fought to preparing for what may lie ahead. In our view, the potential fallout from the accumulation of misguided policy decisions since the COVID-19 pandemic will shape the economic landscape investors must reckon with in the coming years. And, as we discuss in more detail later, limiting the damage from this fallout and repairing structural issues that continue to deteriorate will require a coherent set of proactive policy solutions.

Where We Are Now: A Recap of 2022

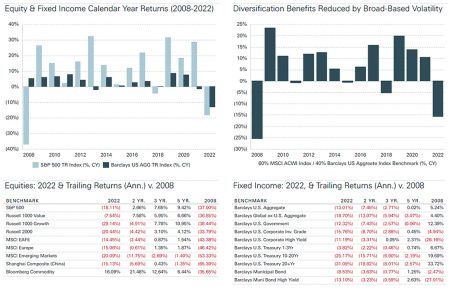

Markets closed out 2022 with the worst calendar year performance since 2008 as inflation, monetary policy tightening, slowing growth, the Russia-Ukraine war, China’s “Zero-Covid” measures, and other geopolitical events tore through the global economy and upended the optimism of the post-pandemic boom. This confluence of factors led to most major asset classes moving increasingly in tandem, and the ensuing volatility wreaked havoc across the investment universe. Both equities and fixed income markets suffered their largest annual declines in 15 years with the S&P 500 Index down more than -18% and the Barclays U.S. Aggregate Bond Index losing -13%. Unlike in 2008, fixed income provided little benefit to downside risk mitigation or volatility dampening as rapidly rising rates inflicted double-digit declines upon wide swaths of the universe. As a result, the frequently referenced model for a diversified portfolio – a 60% Global Equity and 40% Investment Grade Fixed Income allocation – struggled mightily on its way to finishing the year down almost -16% (see Figure 1). Financial assets with higher correlations to inflation (e.g., commodities, infrastructure), an appreciating U.S. dollar, or rising interest rates significantly outperformed during this period. Illustrative of the latter, the effect of rate volatility on disparate equity styles was stark. Value and Dividend stocks – companies with stronger current cash flows and lower valuation multiples – materially outpaced Growth stocks, which have higher future earnings potential and frothy valuations more sensitive to changes in interest rates (as measured by Russell 1000 Value Index, -7.54% and Russell 1000 Growth Index, -29.14%).

Figure 1: Calendar Year Trailing Market Returns (12/31/2007 to 12/31/2022)1

Capital markets were plagued by large swings in momentum and elevated uncertainty as investors oscillated in their collective outlook for inflation, interest rates, and the economy. All in all, 2022 proved to be a landscape in which bottom-up fundamentals played almost no part in the setting of price levels. And it is likely that this pattern will continue throughout 2023 given the persistent divergence between the market’s expectations for future monetary policy and the Fed’s planned course of action. The more these forecasts deviate from one another, the greater the turbulence that will be injected into trading when investors are ultimately forced to reconcile their opinions with reality.

Where We Go from Here: Reckoning with the Pandemic & Inflation Fallout

Understanding that prudent preparation now will be pivotal to successfully navigate the post-inflation world, we have bifurcated our outlook to address two distinct environments we anticipate encountering going forward. The first encompasses the near-term period – approximately the next 12 months – where inflation will remain a material factor in prevailing conditions. Then, looking further out on the horizon, the second period seeks to evaluate the fallout from policy choices made over the past several years and their potential for aggravating longer-term structural issues that have been building for some time. For clarity, we outline each separately in the following two sections.

Part I – Fighting the Fed is a Fool’s Game

As we embark on a new year with inflation marching steadily lower (U.S. CPI came in at 6.4% for January from 9.1% in June 2022; U.S. CPI ex-Food & Energy was 5.6% in January down from 6.6% in September 2022),² the consensus has grown increasingly convinced that the Fed has done enough to slay the inflation dragon and is quickly approaching the end of this monetary tightening cycle. This view is reflected by current market data that has priced in two final 0.25% rate hikes (one of which came in February), rate cuts in the second half of the year, and headline inflation falling to 3.7% by year-end.³ With conviction around this view solidifying further since December, interest rates began a retracement, positive sentiment gathered momentum, and both equities and fixed income experienced a significant relief rally. However, our confidence that this is anything more than a short-lived trend is close to zero.

Our outlook for 2023 remains consistent and little changed from the past 12-24 months. We believe that inflation and interest rates will prove to be sticky for some time, lingering at higher levels for longer than current forecasts suggest. Despite recently announced layoffs across certain sectors and a slight slowing of wage growth, the U.S. labor market’s resilience in the face of tightening financial conditions has defied expectations of late and might even be picking up steam. January’s surprising employment report saw an acceleration of job growth as employers added 517,000 jobs (nearly three times more than expected), previous month’s figures were revised materially higher, and the unemployment rate fell to a 53-year low of 3.4%.4 Job openings ticked up as well. With about two open positions for each person currently seeking a job, demand for labor continues to significantly outstrip available supply.5 While large cuts by companies like Amazon and Microsoft may make headlines, the tech-heavy information sector makes up only 2% of all private sector jobs. In contrast, service industries – such as healthcare, education, leisure and hospitality – account for 36% of private payrolls and 63% of all job growth over the past six months.6 These latest monthly reports have not only reversed five months of slowing growth, but they portend a scenario where employment and wage growth are likely to resume putting upward pressure on inflation.

Economic data of this ilk is backward-looking and notoriously difficult to forecast. Thus, the extrapolation of a singular month’s data into the future would be highly susceptible to error and provide negligible predictive value. So, for argument’s sake, we set it aside to assess the substance of other factors which may influence how 2023 unfolds.

Dating back to 1970, a cardinal rule of sound portfolio management has long been “Don’t Fight the Fed.” Its invocation is so ubiquitous – such that even amateur investors grasp the concept – because of its perfect record against those who fail to heed the warning. Yet today, for some inexplicable reason, market participants have assured themselves that their elusive first win is finally within reach; this time things will be different. For more than a year now, Fed Chairman Jerome Powell has been transparent and clear in his communications outlining the policy steps the central bank would take to break inflation while consistently emphasizing their commitment to achieving this goal. Here are a few recent examples:

Given the outlook, I don’t see us cutting rates this year.

We’re going to be cautious about declaring victory and sending signals that the game is won. We’re in the early stages of disinflation [and it’s] going to take time.

We think we’re going to have to do further [rate] increases, and we think we’ll have to hold policy at a restrictive level for some time.

We’re going to react to the data. So if we continue to get, for example, strong labor market reports or higher inflation reports, it may well be the case that we have to do more and raise rates more than has been priced in.7

In our opinion, this is indisputable evidence of the Fed’s planned course of action. How anyone could interpret such explicit, unambiguous language and arrive at a contradictory conclusion strains credulity. Has the investment community lost faith in the central bank or Jerome Powell? Is he not credible? Do investors really want to bet that the Fed lacks the fortitude to follow through on their plans? Trying to surmise why the Fed’s intentions are becoming so distorted as each statement is released, digested, and then translated into market pricing leaves us scratching our heads. Maybe it’s simply a case of mass-scale wishful thinking.

Consequently, we again find ourselves playing the role of contrarian. Going along with the “wisdom of the crowd” is often comforting because evolutionary conditioning has taught us there is safety in numbers, but just as often, it is a false sense of security luring us into a dangerous trap. Given a dearth of evidence to the contrary, we are satisfied that any clear-eyed, unbiased assessment of currently available information, especially those detailed above, would align with the major contours of our thesis. We therefore remain steadfast in our outlook that inflation and interest rates will hold at higher levels for longer than currently anticipated. While there is always a possibility that market dynamics can exhibit irrational characteristics for extended periods, the past year has demonstrated the market’s tendency towards forecasting errors, both in frequency and magnitude. And though this places us back in direct conflict with consensus expectations, the evidence is too compelling to ignore – prudent management requires responsible action to mitigate foreseeable pitfalls. In our estimation, the way portfolios are positioned in relation to inflation and interest rate risk will be a key point of differentiation in realized performance.

Part II – A Return to Secular Stagnation

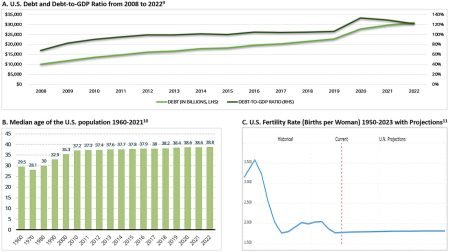

A theory first introduced by the economist Alvin Hansen during the Great Depression, secular stagnation refers to an economy suffering from meager or no long-term growth and structurally low private demand, requiring very low interest rates to boost demand and reach potential output. During the historically sluggish recovery from the 2008 financial crisis, this concept was resurrected in public discourse. For years its validity as a theory as well as its accuracy in describing economic conditions at the time were contentiously debated. While the causes of secular stagnation have yet to be proven empirically, a Bank of International Settlements 2015 paper cites the following potential explanations: “secular deficiency in aggregate demand, slowing innovation, adverse demographics, lingering policy uncertainty, post-crisis political fractionalization, debt overhang, insufficient fiscal stimulus, excessive financial regulation, and some mix of all of the above.”8 Assuming that these hold true, even the casual observer would recognize the tell-tale signs of stagflation’s prevalence in today’s global economy. We highlight a few such conditions in the nearby charts (Figure 2) but, for brevity’s sake, will leave further examination to future dispatches.

Figure 2: Stagflationary Indicators

Conclusion: Portfolio Allocation Update

We conclude with an update on portfolio positioning. Asset classes with strong cash flows, contracted and predictable revenues, and lower sensitivity to elevated interest rates are likely to outperform on a relative basis over the coming period. As such, we remain comfortable with our tactical underweight to Emerging Market equities, U.S. Growth equities, and longer-duration bonds in favor of Value/Dividend equities and short-duration bond sectors. And finally, our strongest short-to-medium term conviction continues to be a shifting of portfolio risk budgets from public to private market exposure (where appropriate). Given that we anticipate muted returns in public markets over the near term, this tactic possesses multiple potential benefits today in our opinion – not only can private assets serve as a risk dampener during volatile markets but, in the current regime, may also increase long-term return potential. As always, we are long-term investors and manage portfolios accordingly. However, in a rapidly evolving environment, we are constantly looking for tactical opportunities to capitalize on dislocations that may produce asymmetric risk-return profiles.

Sources

¹ Addepar

² U.S. Department of Labor, Bureau of Labor Statistics: Consumer Price Index Summary January 2023 released February 14, 2023 – https://www.bls.gov/news.release/cpi.nr0.htm

³ Bloomberg U.S. Economic Forecasts as of February 1, 2023

⁴ U.S. Department of Labor, Bureau of Labor Statistics: Employment Situation Summary January 2023 released February 3, 2023 – https://www.bls.gov/news.release/empsit.nr0.htm

⁵ U.S. Department of Labor, Bureau of Labor Statistics: Job Openings and Labor Turnover Summary December 2022 released February 1, 2023 – https://www.bls.gov/news.release/jolts.nr0.htm

⁶ Wall Street Journal online version: Mass Layoffs or Hiring Boom? What’s Actually Happening in the Jobs Market by Sarah Chaney Cambon and Ray A. Smith on February 9, 2023 – https://www.wsj.com/articles/jobs-hiring-boom-layoffs-employment-11675947399?mod=hp_lead_pos7

⁷ Wall Street Journal online version: Powell Doesn’t See Fed Cutting Rates This Year by Harriet Torry on February 1, 2023 – https://www.wsj.com/livecoverage/federalreserve-meeting-interest-rate-hike-february-2023/card/powell-doesn-t-see-fed-cutting-rates-this-year-2AGm7XzpAgayhyMVKxH; and Fed’s Jerome Powell Braces for Longer Inflation Fight Amid Hiring Surge by Nick Timiraos on February 7, 2023 – https://www.wsj.com/articles/feds-jerome-powell-to-address-economic-outlook-withhiring-surge-in-spotlight-11675781503

⁸ Bank for International Settlements, BIS Working Papers No. 482, Secular stagnation, debt overhang and other rationales for sluggish growth, six years on by Stephanie Lo and Kenneth Rogoff, January 2015 – https://www.bis.org/publ/work482.htm

9 Office of Management and Budget and Federal Reserve Bank of St. Louis via Federal Reserve Economic Data (FRED). “Gross Federal Debt as Percent of Gross Domestic Product.” https://fred.stlouisfed.org/series/GFDGDPA188S. U.S. Department of the Treasury. “The Debt to the Penny.” https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

10 US Census Bureau. “Median Age of The Resident Population of The United States from 1960 to 2021.” Statista, Statista Inc., 17 Dec 2021, https://www.statista.com/statistics/241494/median-age-of-the-us-population/

11 United Nations – World Population Prospects 2022. <a href=’https://www.macrotrends.net/countries/USA/united-states/fertility-rate’>U.S. Fertility Rate 1950-2023</a>. www.macrotrends.net. Retrieved 2023-02-13.

DISCLAIMER

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated in the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward-looking statements as a result of factors beyond our control. Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.