On August 22nd, 2018, the current bull market in the U.S. became the longest in modern history. With unemployment now below 4%, consumer confidence at historically high levels, and U.S. stock indices continuing to hit new records, it is easy to view today’s market through rose-colored glasses. Although economic and market data continue to be positive, we believe now is the time for investors to be more skeptical of current conditions and look for those pockets of risk which may portend a reversal of the good fortune experienced over the past decade.

AARON WEALTH ADVISORS’ INVESTMENT PHILOSOPHY

As this is the inaugural paper of a thought leadership series we intend to share with our clients, we thought it beneficial to begin with a brief description of the Aaron Wealth Investment Philosophy. Our sole focus at every stage of the investment process – from ideation to implementation – is aiding our clients in the successful execution of their goals and legacy.

As investors, we look to be compensated for the risks we take; as such, each plan is built to balance the dual objectives of risk management and after-tax growth. Our investment decisions are grounded around client goals, their risk tolerances, our expectations for macroeconomic and market environments, tactical opportunities, and areas of attractive relative value. Opportunities to capture asymmetric risk/return profiles – where we believe the downside risk is cheap relative to the upside potential – are always of great interest to us, so long as they can be acted upon in an efficient manner.

At the end of the day, we are asset allocators, given our wholehearted concurrence that this is the primary driver of portfolio returns. As found in the landmark paper “Determinants of Portfolio Performance”, asset allocation policy explains approximately 94% of return variation, on average.1

We believe our clients should be as well informed as we are, if they so desire. There is no “black box” here. For this reason, we have built a strong investment culture that we wish to share with our clients through thought leadership papers, such as this one, and educational opportunities. We are in the business of wealth management – your wealth, that is – and it is incumbent upon us to provide you with the tools required to understanding your financial life.

THE GOOD: U.S. ECONOMIC AND MARKET PERFORMANCE CONTINUE TO SURPASS EXPECTATIONS

While surveying the current global economic landscape, we can’t help but draw comparisons to the 1966 epic Western, “The Good, the Bad and the Ugly”, starring Clint Eastwood. The film’s three main characters – “Blondie” (played by Clint Eastwood, The Good), “Angel Eyes” (The Bad), and “Tuco” (The Ugly) – epitomize the economic situations playing out across the world, in our view. The plot centers around the formation of a hesitant alliance between Blondie and Tuco – first, to perpetuate a bounty scheme, and then later, to out-run Angel Eyes in finding a wealth of gold coins buried in the grave of a cemetery.

We begin with “The Good”, Clint Eastwood’s confident and reserved bounty hunter whose character, in many ways, is quite representative of the current U.S. market. Now in the ninth year of a recovery and expansion, the U.S. economy continues to grow with an acceleration of that growth since early 2017. New expansionary fiscal policies, such as tax cuts and deregulation, have provided a much-needed boost to business sentiment and investment. In addition, the reduction in the corporate tax rate has improved the global competitiveness of American companies. As a result of this momentum, the latest reading of Q2 GDP came in at 4.2%, unemployment stands at 3.9%, consumer confidence has reached an 18-year high as of August, and inflation remains moderate at 2.2%.2 At the same time, the bull market in U.S. equities has continued, as the S&P 500 persistently tests all-time highs and the growth in earnings picks up.

We remain structurally positive on the U.S. economy for several reasons.

First, as the unemployment rate has persistently fallen below pre-recession levels (now at 3.9%), we have not seen meaningful upward pressure on inflation driven by wage growth. Not only has there not been a spike, but the level of inflation has recently hovered around the Fed’s preferred rate of 2%. Economically speaking, such a low level of unemployment would be expected to spur increases in unanticipated inflation, as many economists have estimated the Non-Accelerating Inflation Rate of Unemployment (NAIRU) to be 4% – 4.2%. NAIRU is the unemployment rate below which the economy should begin to see the inflation rate accelerate. We believe one explanation for this may be the steady decline in the Labor Force Participation Rate, which fell from a near all-time high of 66% in 2008 to around 62% in 2014, a level around which it has remained since.3 This suggests that there still may be some slack in the labor market and the economy has yet to reach its potential output. As a result, we do not think the Fed will be forced to more aggressively increase rates than current policy suggests in order to combat an overheating economy.

Second, fiscal and monetary policy remains accommodative and supportive of growth. In our view, changes to the tax code – especially the permanent reduction in the corporate rate – and a policy focus on deregulation have set potential economic growth on a path towards higher absolute levels. When coupled with historically low rates and clear communication of Fed interest rate policy, we believe the U.S. economy is on a strong fundamental footing.

Much speculation and apprehension has surrounded the topic of an inverted yield curve – considered by some as a predictor of a coming recession. It occurs when short term interest rates (say the 2-Yr Treasury rate) exceed longer term rates (like the 10-year Treasury rate). However, in our opinion, an inverted yield curve in and of itself is not a cause for alarm. But rather, when large and unexpected jumps in short term rates occur to invert the yield curve – because of a deterioration in economic conditions – one should become concerned. In essence, it is the movement of rates that really matter and not the absolute level, per se. The short end of the yield curve is most strongly affected by monetary policy in normal markets. Because rates have been low or near-zero for so long, we believe that interest rate normalization is driving the flattening of the yield curve, not market concerns of a recession. As we do not anticipate a sudden need for the Fed to rapidly increase rates or a breakdown of economic fundamentals, we are currently less concerned with a potential inversion of the yield curve.

Ordinarily, this data would stoke ebullient optimism in the minds of most investors and inspire a feeling that there is little risk to obtaining the buried gold treasure of our movie. However, the past decade in the U.S. is not what we would call ordinary. Since the Great Recession of 2008, risky-asset markets have been buoyed by cheap capital and the accommodative monetary policy of central banks around the world. These policies have forced investors to allocate greater shares of their portfolios to riskier assets in order to produce a meaningful return. For an expansion of this length, benchmark interest rates are incredibly low on a relative basis, when compared to past cycles.

Thus, despite our positive outlook for the economy in general, we anticipate that the environment for U.S. equities will be more similar to Blondie’s epic quest for buried gold than the low volatility environment experienced over the past several years. That is, we expect a return of higher volatility and greater risk.

From a philosophical standpoint, we believe it is a dangerous prospect to continue overweighting equities when investor and consumer sentiment are historically high. The well-known Warren Buffet quote, “Be fearful when others are greedy and greedy when others are fearful”, is the fundamental underpinning of this approach. We would much prefer to increase equity exposure when these metrics are at their lowest and reduce our risk profile when the market is willing to pay a higher premium. Historically speaking, this attitude towards investing appears to have merit. According to research conducted by James Mackintosh of the Wall Street Journal, equity performance has a 48% positive correlation with changes in 12-month consumer sentiment levels – generally used as a proxy for economic growth – since 1974. This is intuitive, as stocks tend to do well when the economy is doing well. However, he finds a moderately negative correlation of 20% between changes in consumer sentiment and future returns, implying that historically high levels of consumer sentiment are, on balance, followed by periods of negative equity performance. Since the 1960’s, when consumer confidence has reached such heightened levels, stocks have returned only 3% in the following 12 months, on average.4 To us, this implies very little upside when exuberant buying is already taking place, paired with significant downside risk. This is akin to stepping in front of a bulldozer to pick up a few extra nickels.

Because the bull market has extended for nearly a decade, client portfolios may be significantly overweight equities. Whether intentional or not, improper rebalancing or a desire to not “miss out” on continued equity returns could result in a portfolio significantly overweight risk, without investors even being aware. This aggressive stance could lead to asset allocations subject to considerable downside risk and an inappropriate risk profile. With consumer sentiment now at an 18-year high as of August, we would advocate increasing allocations to less-volatile asset classes such as bonds for those portfolios that are currently overweight equities. If today’s exuberant environment is followed by a reversal and subsequent flight to quality, bonds may provide the same return potential, or greater, without the significant downside risk of equities. While this may lead to temporary underperformance in the short-run, we believe in the intermediate-to-long term it will be additive for client portfolios.

For those portfolios not currently overweight equities, a structural rotation from a growth-tilt to a value-tilt is warranted, in our opinion. Should volatility increase, as we expect it will, we would prefer to hold value stocks – such as dividend payers and those in defensive sectors – which are less sensitive to changes in momentum and market sentiment.

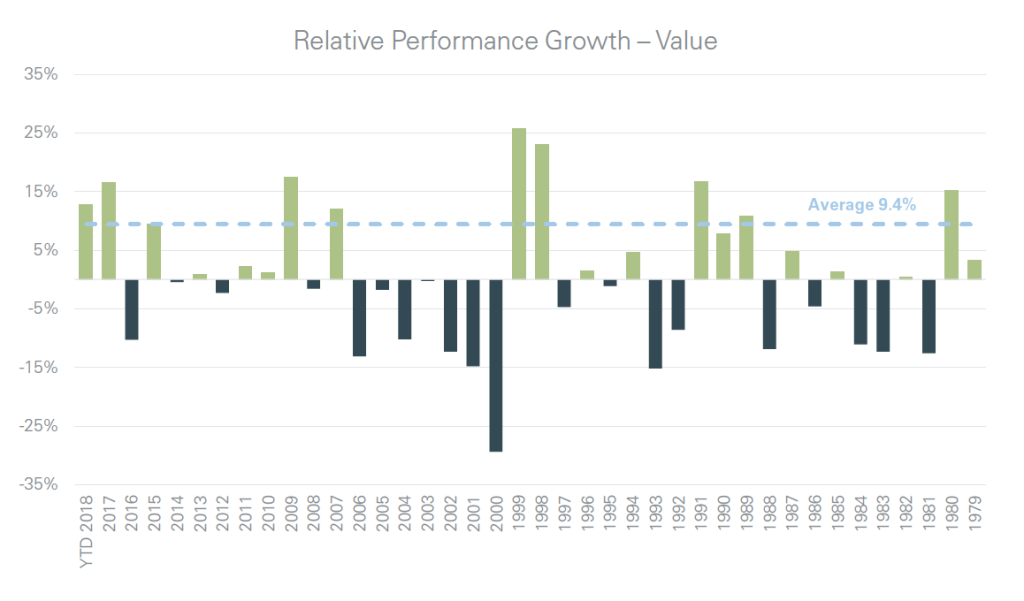

In calendar years since 1979, growth and value equities have split outperformance periods, with growth outperforming in 19 years (including YTD 2018) and value outperforming in 20 years. However, from 2009 through August 2018, growth has outperformed in 7 out of 10 calendar year periods by an average annualized rate of 9%. This is approximately equal to the historical average rate of 9.4% when growth outperforms value (see chart below).5 As the relative outperformance between the two styles tends to be cyclical and the most recent periods have seen growth favored well-above historical averages, we would expect this trend to revert and value to rebound on a relative basis.

Another area of focus for us is international developed market equities, as measured by the MSCI EAFE Index. For clarity, the MSCI EAFE Index contains majority exposure to Europe, the U.K., New Zealand, Australia, Singapore, and Japan. After the Great Recession of 2008, the central banks of these countries reacted more slowly than did the U.S. Fed to cut interest rates. As such, their economic and market recovery trailed that of the U.S. For the past several years, many asset managers have been bullish on and overweight these equity markets due to an expectation that they would eventually catch up to the strong growth seen here in America. However, international markets have been hampered by the U.S. dollar bull cycle and higher U.S. rates, which has attracted capital flows elsewhere. Most recently, concerns of European bank exposure to Turkish debt and increased trade tensions globally have sparked heightened volatility. Given the significant contribution of export activity to economic growth, these international markets are much more sensitive to tariffs and trade restrictions. However, while volatility may increase over the near-term, we have a bullish outlook for international developed equities over the medium-to-long term horizon. From a valuation perspective, EAFE markets are attractive relative to U.S. equities. Central bank policy remains quite accommodative, with interest rates near-zero and real rates negative in some instances. In our opinion, international developed markets will eventually catch up to the U.S. cycle. For investors willing and able to tolerate some near-term volatility, we are positive on the space and see value in a tactical overweight.

For U.S. investors, currency plays an important part of international investing. Strong returns in foreign currency investments can be eroded by an appreciating U.S. dollar when those returns are repatriated. As we expect the U.S. dollar to continue its bullish cycle through 2018 and into 2019, we would recommend currency hedging a portion of any international allocation. To put this in perspective, when investing internationally on an unhedged basis, one is essentially taking the explicit view that the U.S. dollar will depreciate relative to foreign currencies (a depreciating USD increases the real return of international investments, all else equal). On the other hand, a fully currency hedged portfolio is taking the explicit view that the U.S. dollar will appreciate (currency hedged portfolios outperform unhedged portfolios when the USD is appreciating, all else equal). While we do anticipate the U.S. dollar to appreciate further, currency cycles are notoriously volatile and difficult to predict. For this reason, we would advocate for a 50% / 50% split between currency hedged and unhedged portfolios. This is a neutral stance that does not take an explicit view on currency movements.

THE BAD: CRISES IN EMERGING MARKETS CONTINUE THEIR DOWNWARD SPIRAL

We now turn to “The Bad”, a.k.a. Angel Eyes, the ruthless and sociopathic mercenary hellbent on finding the gold before the duo of Blondie and Tuco. Throughout the film, Angel stalks, tortures, and kills anyone that stands between him and the gold. Although he is ultimately unsuccessful in his quest, Angel Eyes leaves a wake of violence in his path. We see this character as an apt representation of the economic and humanitarian crises unfolding in several Emerging Market countries – most notably Argentina, Turkey, and Venezuela. Despite the severity of many of these situations, it is hard for us to ignore the attractive relative valuation levels of these markets. Aside from the short-term volatility taking hold, we see Emerging Markets as an attractive opportunity for more aggressive investors.

Emerging market economies have been embattled this year largely because of rising U.S. interest rates, the resurgence of the U.S. dollar, and investors’ concerns about their heavy reliance on borrowing in U.S. dollars. During the near-zero global interest rate environment post-2008, emerging market countries significantly benefitted from yield-chasing. While investors scoured the globe for higher yielding opportunities, these markets began increasing debt issuance in U.S. dollars to attract capital inflows. As a result, reliance on external financing increased substantially. In some instances, large portions of this debt need to be rolled over in the near term, at a time when emerging markets are much less attractive to global investors. As U.S. interest rates have moved higher, capital has been reallocated away from risky emerging market debt, which typically provide a higher yield relative to developed market debt. Compounding this problem, a strengthening U.S. dollar (relative to emerging market currencies) makes the repayment of dollar-denominated debt more expensive.

Nowhere is this more apparent than Argentina and Turkey. In Argentina, external debt has climbed to over $250 billion as the government sought to inject capital into the economy rather than implement politically-difficult austerity measures. Foreign exchange reserves have fallen to $60 billion, leaving less room for open-market defense of the peso – which has fallen nearly 58% over the past year. In a positive step, the central bank has raised interest rates to 60% in order to stem capital flight and inflation, which recently jumped to 30% annually. Investors are clamoring for a cohesive, sustainable economic plan that goes further than reliance on the IMF for help, and sound policy measures will be needed to stall the downward spiral.6

The story is very similar in Turkey, which saw its currency – the lira – plummet 45% over the past year. Almost 20% of financing for Turkey’s largest banks are due between the end of 2018 and 2019, two thirds of which is in U.S. dollars. The 20% sell-off in the Lira relative to the dollar over July and August will assuredly make the rolling of this debt more precarious. Next year alone, Turkish banks and companies will need to roll over $187B in external financing. While an independent central bank could dramatically improve the situation, it appears the political influence of President Erdogan may be to powerful. Until recently, the central bank had refused to increase rates – which would go a long way to attracting capital inflows – most likely bowing to public demands from the president. In mid-September, interest rates were finally increased over 6%. For the first time in a decade, interest rates are now above the inflation rate (which jumped to 18% in September). Meanwhile, Erdogan has made it known he will not tolerate these high rates for very long – leaving market participants concerned that this positive step may be short-lived.7

Elsewhere, a full-blown economic and humanitarian crisis continues to unfold in Venezuela. Once one of the fastest growing and richest countries in the world (based on per capita income), the oil-rich nation has collapsed. And what began as a steady march towards socialism has now become a violent usurpation of political power and the economy by the authoritarian government of Nicolas Maduro. The freefall accelerated as Maduro sought to consolidate political power by removing the last vestiges of democracy, which included: re-writing the constitution, creating a new legislative assembly packed with regime cronies, jailing or killing political opponents, violently squashing civilian protest, and seizing private businesses. This, along with Maduro’s economic policies, have extracted the last remaining productive capacity in the economy. Inflation is estimated by the IMF to reach 1,000,000% and the currency is essentially worthless. With less production coming out of the country’s nationalized oil company coupled with global sanctions, the government has little funding to facilitate the importation of food and medicine needed for the population. Widespread food and medical supply shortages have led to a humanitarian crisis of epic proportions. As citizens of Venezuela have fled, neighboring countries have been forced to deal with the fallout of taking in these refugees – which has stoked its own violent and economic consequences.

While global markets seem to have taken these situations in stride, it is not out of the realm of possibility that the contagion could spread. Should defaults start piling up around emerging markets, the pain could begin to affect those investors and banks in developed markets that have lent to these countries. In addition, capital flight could accelerate if interest rates in the U.S. and Europe increase substantially. Lastly, which we discuss more later, a dramatic increase in tariffs imposed by the U.S. could produce a bleaker outlook for these economies given their reliance on exports to the U.S. market.

Historically, Emerging Market economies have significantly benefited from accelerating global growth. Given our positive outlooks for the U.S. and international developed economies, we anticipate global growth to continue its upward trajectory. This, coupled with attractive valuation levels and rebounding commodity prices, paints a more optimistic picture for this part of the world. If these crises are contained and global growth continues on its current path, we see Emerging Markets as an interesting investment opportunity, albeit with higher risk.

THE UGLY: 2 STEPS FORWARD, 1 STEP BACK

Our last piece of the puzzle is Tuco, portrayed as an oafish but persistent outlaw. Despite giving up valuable information about the location of the buried gold and facing death multiple times, Tuco makes off with half of the loot – largely due to the benevolence of Clint Eastwood’s character. The often-contradictory fiscal policy impulses of the current U.S. administration are represented well by this character.

On the one hand, as we detailed earlier, the overhaul of the tax code and consistent deregulatory effort have jumpstarted the U.S. economy out of a slow-growth environment. These policy measures have laid the groundwork for a resilient and strong economic environment. On the other hand, persistent anti-trade rhetoric targeted at the U.S.’s largest trading partners, the imposition of tariffs, and the potential abandonment of major trade agreements threatens the success of pro-growth policies. The Republican Party has long stood for free trade and open markets. However, because Congress has gradually ceded more and more trade policy discretion to the Executive Branch, markets now find themselves subject to the worst impulses of protectionist ideals.

Those involved would benefit from the lessons learned after the passage of the Smoot-Hawley Tariff Act of 1930. The tariffs enacted with this law were the second highest in 100 years and led to a significant reduction of both American imports and exports. As a result, economists generally agree that this protectionist law exacerbated the Great Depression, rather than saving jobs and the economy. The overwhelmingly negative effects of tariffs and protectionist trading practices are settled economic science, in our opinion, and should be avoided.

The current situation seems to be less dire than originally anticipated, at least for the moment. Mexico, Canada, and the U.S. have made significant progress in the renegotiation of NAFTA. European countries and the EU seem willing to work with the administration to find mutually-beneficial agreements. And we are optimistic that the U.S. can solidify trading agreements with its biggest allies over the coming years. The biggest risk we see is the escalating trade dispute with China.

After tit-for-tat tariff retaliations in the spring and early summer, China and the U.S. began serious talks to end the dispute and come to an understanding. Several important issues needed to be resolved, such as the dumping of excess Chinese steel capacity on global markets, intellectual property theft, and protection of American companies doing business in China. It appeared that the Chinese understood the importance of the U.S. consumer as an export market. However, as of mid-September, those talks have broken down. President Xi Jinping – despite facing a slowing economy – has dug in his heels, preferring instead to flex the economic weight of China. As a result, the U.S. imposed additional tariffs on $200 billion worth of Chinese exports, and China retaliated with additional tariffs on $60 Billion worth of U.S. exports.

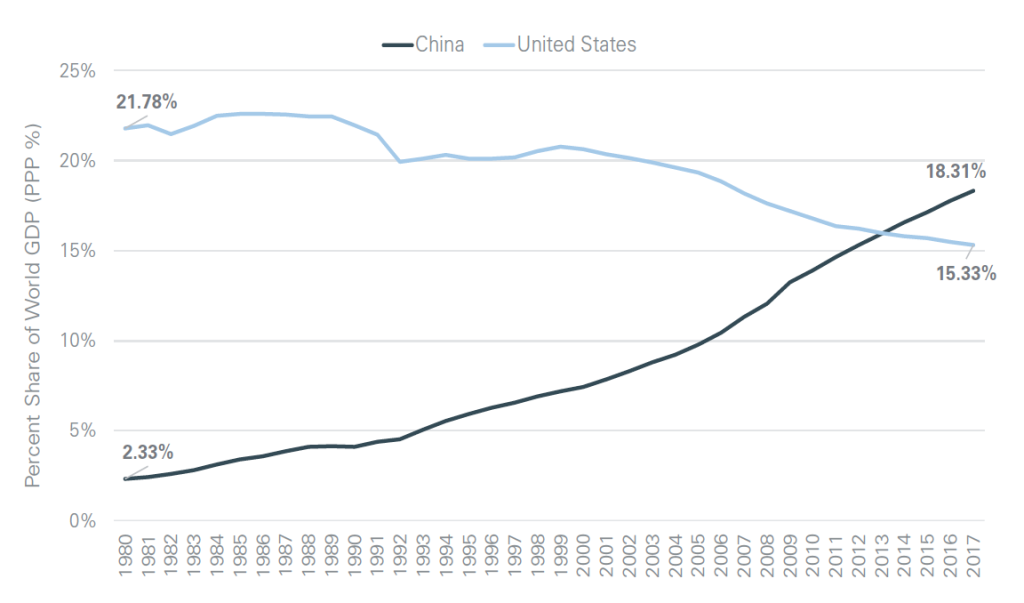

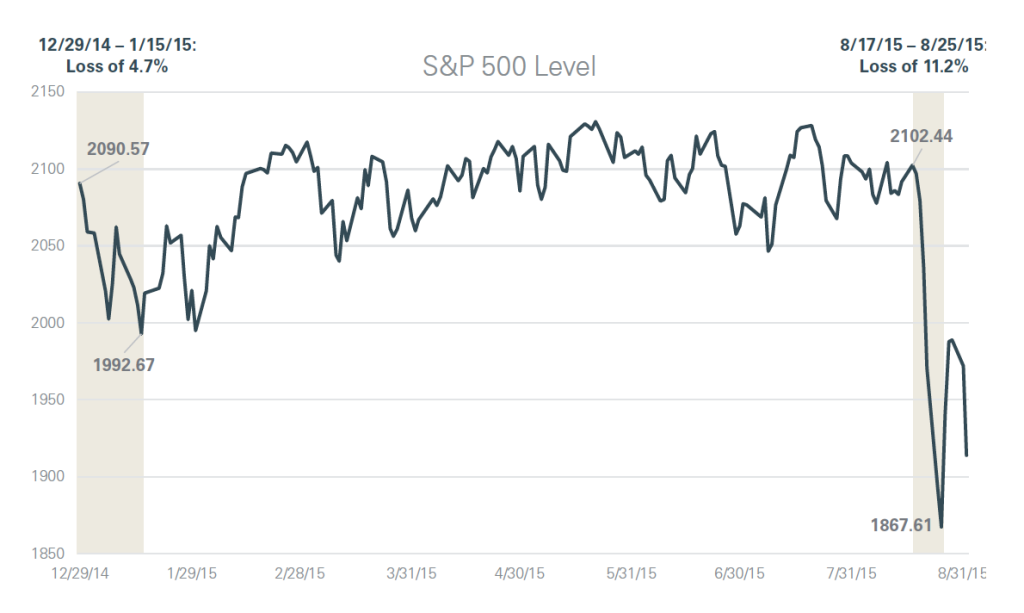

An economic axiom often repeated goes, “When America coughs, the world catches a cold.” It illustrates the dramatic impact the U.S. economy has on global growth. However, since 1980, the U.S. share of global GDP has fallen from 22% to 15%.8 Over this same period, China’s share of global GDP has risen from 2% to 18% (see below for historical US & China GDP growth).9 One only needs to remember January and August of 2015 to understand the importance of the Chinese economy to global markets. As concerns of slowing economic growth in China intensified in January 2015, the

S&P 500 sold off 4.7% during a two-week period. Similarly, later the same year in August, the U.S. market tanked 11.2% over the span of one week because China devalued its currency by 3% (see below S&P 500 Level chart).10 For this reason, an escalating trade war between the two largest economies in the world is a potential risk that must be monitored closely. While tariffs themselves might not rout U.S. markets right away, their negative effects on an important Chinese economy – that appears to be slowing – could have a dramatic impact on the U.S. economy through a significant reduction in global growth.

We would be remiss if we did not briefly mention another risk parallel to this theme. Across the globe, the rise of nationalism and anti-establishment sentiment has continued to gain momentum. From the National Front in France to the Five Star Movement and League in Italy to the Swedish Democrats, nationalist parties have garnered a significant following and power as they rail against globalism. With views and policies antithetical to those that have helped ignite global growth over the past decades – such as free movement of capital, trade, and labor – these shifts toward isolationism could threaten a world economy that is more interconnected than ever. While most of these parties represent a minority in their respective governments (apart from the ruling coalition of Five Star and the League in Italy), their significance cannot be overlooked. As such, we remain focused on elections and policies of foreign governments across the world in order to evaluate potential geopolitical risks that could negatively impact portfolios.

CONCLUSION

To conclude, we are structurally positive on U.S. markets and expect the strength of the economy and growth-oriented policy measures to overcome the short-sighted impulses that could threaten progress. However, given the exuberance of investor and consumer sentiment, we find it imperative to remain cautious. By positioning ourselves in a more defensive stance, we can potentially limit our downside risk exposure while we wait for the inevitable pull-back and buying opportunity. It is our opinion that now is the time to begin tilting portfolios towards more value-oriented and low-volatility equities. Once signs of market risk become evident, it is already too late to advantageously rotate portfolios – the premium for protection becomes too high. As is often the case, investors looking to weather the storm when it’s already pouring are left without a protective shelter. In addition, we believe the worst of the emerging market crises are behind us. Several positive steps are currently being undertaken to stem the bleeding, so to speak. While the economic and humanitarian suffering is extreme in certain cases, we ultimately do not foresee a contagion event. It is our hope that world powers can come to the aid of those citizens trapped in desperation by reigning in “The Bad” actors which have caused such terrible destruction.

Disclaimer

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered, or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This report is a publication of Aaron Wealth Advisors LLC. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change.

*Information contained herein does not involve the rendering of personalized investment advice, but is limited to the dissemination of general information. A professional adviser should be consulted before implementing any of the strategies or options presented.

*Information is not an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*All investment strategies have the potential for profit or loss. The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

- “Determinants of portfolio performance”: Brinson, Gary P; Hood, L Randolph; Beebower, Gilbert L Financial Analysts Journal; Jan/Feb 1995; 51, 1; ABI/INFORM Global pg. 133.

- Source: YCharts. Bureau of Economic Analysis; U.S. Real GDP Growth 8/29/2018. Bureau of Labor Statistics; US Unemployment Rate 9/7/2018 and US Core Inflation Rate 9/13/2018. University of Michigan; University of Michigan US Consumer Sentiment Summary 9/14/18.

- Source: YCharts. Bureau of Labor Statistics; US Labor Force Participation Rate 9/7/2018.

- Research paraphrased. Source: James Mackintosh, Wall Street Journal “Economic Confidence is Really High. Perhaps It’s Time to Sell.” 9/10/2018.

- Source: Y Charts. Data range: 1/1/1979 – 8/31/2018. Growth and value equities represented by the Russell 1000 Growth Index and Russell 1000 Value Index. Performance is shown gross of all fees. It is not possible to invest directly in any index.

- Source: “How Argentina’s Economic Crises Unfolded”; Julie Wernau and Ryan Dube; Wall Street Journal; 9/4/2018.

- Source: “What Turkey Can Do If Market Troubles Return”; Jon Sindreu and Christopher Whittall; Wall Street Journal; 8/27/2018

- Source: IMF Cross Country Macroeconomic Statistics. Expressed in percent of world GDP in Purchasing Power Parity dollars. 1980 – 2017.

- Ibid

- Source: Y Charts. Data range: S&P 500 performance during January of 2015 and August of 2015. Performance is shown gross of all fees. It is not possible to invest directly in any index.