Divorce can often be an emotional whirlwind, leaving you feeling overwhelmed and drained, with little energy to address potentially significant financial upheaval. Building an iron-clad support team is critical in facing these challenges, made up not only by your trusted friends and family, but also by adept legal counsel and an experienced financial advisor. This team can help you regain your financial footing with confidence.

Understanding the Pillars of Your Divorce Team

Legal Guidance: Family Attorney

Your attorney plays a crucial role in dealing with the legal aspects of your divorce. From handling all the paperwork to negotiating a fair divorce settlement, their expertise becomes the cornerstone of your decision-making process.

Financial Counsel: Financial Advisor

Your financial advisor becomes a beacon of rational decision-making by ensuring you understand the financial consequences of various settlement scenarios. An objective view and focused approach can keep you anchored, helping make decisions that favor your long-term financial stability.

Selecting the right financial advisor is a critical step in this journey. It’s important to choose an advisor who is a fiduciary, legally binding them to act in your best interest. Your advisorshould be able to provide impartial advice without any bias.

Once the divorce proceedings conclude, your financial advisor can help you navigate life changes and manage your financial health. This involves understanding new tax implications and recalibrating your financial plans as your life evolves.

Considerations for Financial Stability Post-Divorce

Reevaluating your financial status after a divorce is crucial for long-term stability and growth. Here are some additional steps to consider:

Update Your Estate Plan

After a divorce, it’s essential to update your estate plan. This includes revising your will, powers of attorney, updating beneficiaries on life insurance policies and retirement accounts, and modifying any trust agreements. Ensure that your estate plan reflects your new marital status and financial priorities.

Reassess Retirement Plans

Divorce can have significant implications on your retirement plan. Review your retirement accounts and contributions and ensure that your retirement goals are still achievable. Consider consulting a financial advisor to make any necessary adjustments.

Evaluate Insurance Coverage

It’s important to reexamine your insurance needs, including health, home, auto, and life insurance. Ensure that you have adequate coverage for yourself and any dependents. Updating your insurance policies can provide peace of mind and financial security.

Work with Your Financial Advisor

Continuing to work with a qualified financial advisor can help you navigate the complexities of your new financial landscape. A financial advisor can offer tailored advice, helping you make informed decisions that support your long-term goals.

Final Thoughts

Divorce marks the beginning of a new chapter in your personal and financial lives. By taking proactive steps and leveraging the expertise of a team, including a financial advisor, you can secure your financial future and embark on this new journey with confidence. Aaron Wealth Advisors would be honored to support you every step of the way. Contact us today to learn how we can help you achieve financial independence and peace of mind.

DISCLAIMER *Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated in the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward-looking statements as a result of factors beyond our control. Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.

Bill Andrakakos, CFA, FRM President & Chief Investment Officer

As you navigate the complexities of managing your estate, an important consideration is how to protect assets from excessive taxation. Estate taxes have the potential to significantly reduce the inheritance intended for your loved ones. With thoughtful planning and the right strategies, you can minimize the impact of estate taxes, ensuring that your legacy remains intact for future generations.

Trusts

Trusts are crucial instruments in estate planning. They provide control over the distribution of your assets, potentially lower estate taxes, and they can protect your estate from the probate process. By placing assets in a trust, you can reduce the taxable value of your estate. For example:

Irrevocable Trusts can remove assets from your estate entirely, thus reducing the total estate value subjected to taxes.

Charitable Trusts can reduce estate taxes by directing a portion of the estate to charitable organizations.

Qualified Personal Residence Trusts (QPRT) maintain ownership of your residence allowing you to retain the right to live in the home for a specified period while removing its value from your estate.

Grantor Retained Annuity Trusts (GRAT) can hold appreciating assets and provide an annuity payment stream for a specified term, with any remaining assets passing to beneficiaries free of gift or estate tax.

Gifting

The act of gifting is not just a means of sharing wealth but also a method of reducing taxable estate value. The IRS permits individuals to give a specific sum annually without being subject to gift tax. Regular, planned gifting can strategically lower estate value and thereby the potential estate tax liability. Take advantage of annual gift tax exclusions to transfer assets tax-free each year to beneficiaries.

Charitable Contributions

Charitable donations can also play a role in diminishing the size of a taxable estate. Contributing to charitable organizations, foundations, or trusts not only supports a cause close to heart – but also scales back estate taxes.

Life Insurance

Life insurance payouts typically do not attract income tax. However, they can add to the estate value and incur estate taxes. By assigning the policy to a trust, the benefits can be kept off your estate’s taxable value. By establishing an Irrevocable Life Insurance Trust (ILIT) to hold life insurance policies outside of your taxable estate, they can provide tax-free proceeds to beneficiaries.

Qualified Plans

Utilize retirement accounts and other qualified plans strategically. These assets may have tax advantages and can be structured to minimize estate tax exposure.

Educational Savings Accounts

Educational investments like 529 plans offer another way to reduce an estate’s size while contributing to the future of a child’s education. Contributions grow tax-free if they are used for qualified educational expenses.

Family Limited Partnerships (FLPs)

FLPs can be structured to enable the previous generation to retain control over assets while sharing the financial benefits with other family members. Unlike irrevocable trusts, the members of a family limited partnership can change the terms of the agreement. Additionally, FLPs can offer some decreased liability. Family members who have limited partnership interests can be protected from creditors.

Proactive Planning

Early and regular reevaluation of your estate plan is key to seizing the benefits of a shifting financial landscape and changes in tax laws. Minimizing estate taxes and preserving wealth for beneficiaries requires a thoughtful approach and proactive planning. By working together with financial advisors, estate planning attorneys, and tax professionals you can develop a comprehensive strategy tailored to your specific goals and financial situation. Reach out to find out how Aaron Wealth Advisors can help create a legacy for generations to come.

DISCLAIMER *Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated in the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward-looking statements as a result of factors beyond our control. Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.

Introduction

Since the dawn of mankind, humans have been afflicted with an insatiable appetite for attempting to divine what the future holds. Proof of this innate obsession is embedded throughout history with examples stretching back to antiquity. The Babylonians (approx. 2000 BC – 1600 BC) would closely examine a sheep’s liver, attributing insights about the future to specific anatomical surface features.1 Roman general Claudius Pulcher famously consulted and relied heavily on “sacred chickens” when seeking wisdom for upcoming battles, bringing a coup to every ground.2 And given how vast the Roman Empire stood in its prime, one could easily conclude that these were some well-traveled chickens! As humanity advanced and industrialized, this hunger grew more voracious – catapulting supposed prophets and seers, like the Renaissance’s Nostradamus, to generational fame. However, as capital markets began to form and modernize, a new wave of fortune telling gained traction and legitimacy from the investing public. In his book titled, “Fortune Tellers: The Story of America’s First Economic Forecasters”, Walter Friedman writes how pioneers in the world of economic forecasting thrived during the period leading up to the Great Depression…but then ultimately failed to predict the crippling crash of 1929.

Today, with computing power capable of meticulously processing, analyzing, and torturing the vast world of data, economic and market forecasting – from GDP growth to interest rates to stock prices – is generally viewed as a noble pursuit of science and empirical research. All that stands in the way of predicting the market’s next move is the discovery of a “perfect” model that can dissect and explain the intricacies of our modern financial universe. Through our modern lens, it is easy to look back on the forecasting methods of the ancient Babylonians and Romans as foolish and crude. But we should ask ourselves – how much more accurate are we than they? While it is difficult to exactly quantify the precision of our primeval counterparts (despite knowing General Pulcher’s forces went on to suffer complete defeat by the Carthaginians in direct contradiction to the prophesy of “the sacred chickens”), forecasts today can be tested for accuracy.

In this edition of Aaron Wealth Advisors’ “The View from Here” we try to navigate the turbulent waters of predicting future interest rate movements, specifically how the Federal Reserve’s Dot Plot and the market’s implied path of interest rates can lead investors to make poor decisions based on false confidence.

However, prior to jumping into our analysis and conclusion, we set the stage by addressing the following: 1. How interest rates drove capital markets in 2023. 2. The purpose behind the Dot Plot and how its popularity has grown. 3. How wildly inaccurate interest rate forecasts devasted markets in 2022. 4. The historical reliability of the Dot Plot. 5. What to make of it all and investment implications. For those interested in only the result, punchline, or interpretation, let’s just say “those that live by the crystal ball…tend to eat shattered glass.” – Ray Dalio.

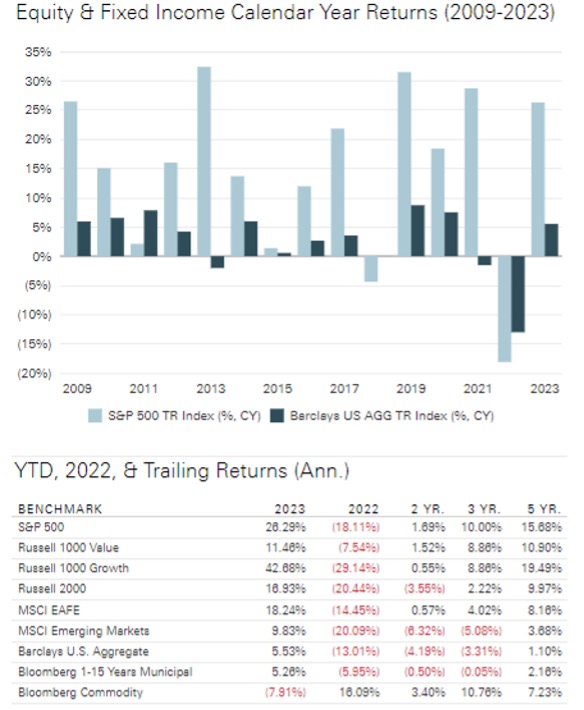

Last year marked a clear departure from 2022, with most asset classes outperforming their prior year returns and surpassing consensus expectations. At the beginning of 2023, investors anticipated a slowdown in corporate earnings as elevated borrowing costs would likely pull the U.S. economy into a recession. However, financial markets avoided the recession many believed was inevitable and marched higher, with the S&P 500 posting a monstrous gain of more than 24% and the Dow finishing near a record high. The AI craze fueled the “Magnificent Seven” (Apple, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia and Tesla) to account for roughly 60% of the S&P 500’s returns in 2023. Heading into the 4th quarter, the Bloomberg U.S. Aggregate Bond Index was on track to record its 3rd consecutive negative year and worst performance streak since its inception in 1986. But this ignominious result was sidestepped with the help of unprecedented interest rate fluctuations – wherein the 10-Year Treasury yield, after soaring to 5% in October, plummeted over the final seven weeks of the year and settled at 3.9%, identical to where it was 12 months ago.

Figure 1: Calendar Year & Trailing Market Returns (12/31/2022 -12/31/2023)3

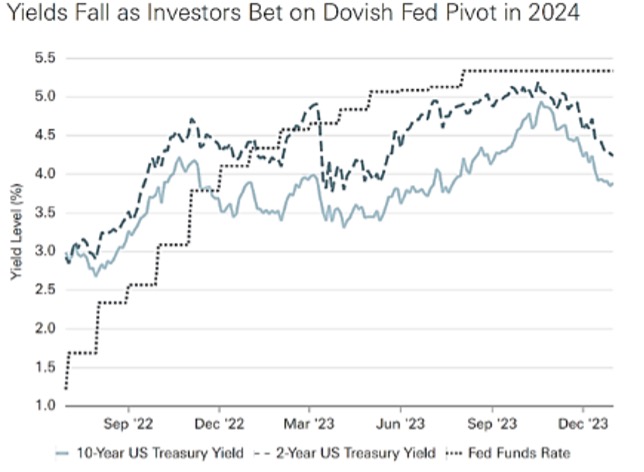

Amid one of the strongest “everything rallies” cycles in decades, financial markets seasoned an unexpected regional banking crisis, a U.S. government debt downgrade, and rising geopolitical tensions around the world. Last year will be remembered as a period where substantial shifts in the market’s narrative for monetary policy overshadowed notable developments in the fundamentals which ordinally drive investor sentiment. At the beginning of the year, most experts predicted an impending recession, but by summer, the consensus course corrected to the expectation of “higher for longer” inflation and interest rates. In the 4th quarter, the narrative whipsawed once again, this time focusing on subsiding inflation, speculation about a “soft landing” for the economy, and an increasing anticipation of rate cuts in 2024.

Figure 2: Fed Funds Rate vs 2- & 10-Year U.S. Treasury Yields3

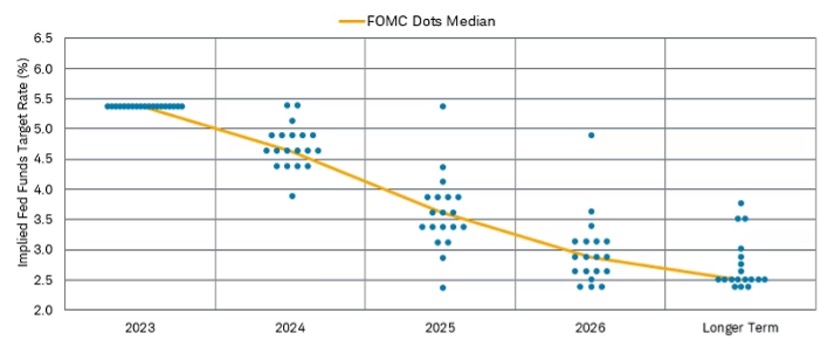

Encouraged by a decline in inflation, the December 13th Federal Reserve’s Open Market Committee (FOMC) Dot Plot signaled a significant drop in the Fed Funds rate over the next few years, returning to 2.5% over the long run. The Summary of Economic Projections (SEP) that accompanied the Dot Plot revealed that the median expectation of Fed officials forecasted three rate cuts of 0.25% each in 2024, aiming to bring the Fed Funds rate to 4.6%, compared to an estimate of 5.1% as recently as last September.

Figure 3: Federal Reserve, Summary of Economic Projections, December 13, 20234

These developments prompted a decline in bond yields while sparking celebration in the stock market that a “soft landing” or “no landing at all” scenario was within reach. Surely with the Federal Reserve’s tremendous resources, PhD-level expertise, unrestricted access to every morsel of relevant economic data, and wealth of experience, a soft landing should be a forgone conclusion, right? Well, empirical evidence suggests otherwise. And in some cases, investors would be better off doing the exact opposite of what the Fed Dot Plot depicts. This finding should prompt any rational market participant to question the validity of the Federal Reserve’s crystal ball.

Exploring the Dot Plot: Unraveling its Purpose & Growth in Popularity

The Federal Open Market Committee (FOMC) has published economic forecasts from meeting participants in its quarterly Summary of Economic Projections (SEP) since 2007. With the sole purpose of offering more transparency following the 2008 Global Financial Crisis, the Federal Reserve introduced the FOMC Dot Plot in 2012. At that time, the Federal Reserve aimed to offer the public early insight into the policies that Fed officials were contemplating for both the short- and long-term. According to Ryan Sweet, Chief Economist at Oxford Economics, it was their version of “aggressive forward guidance”. 5

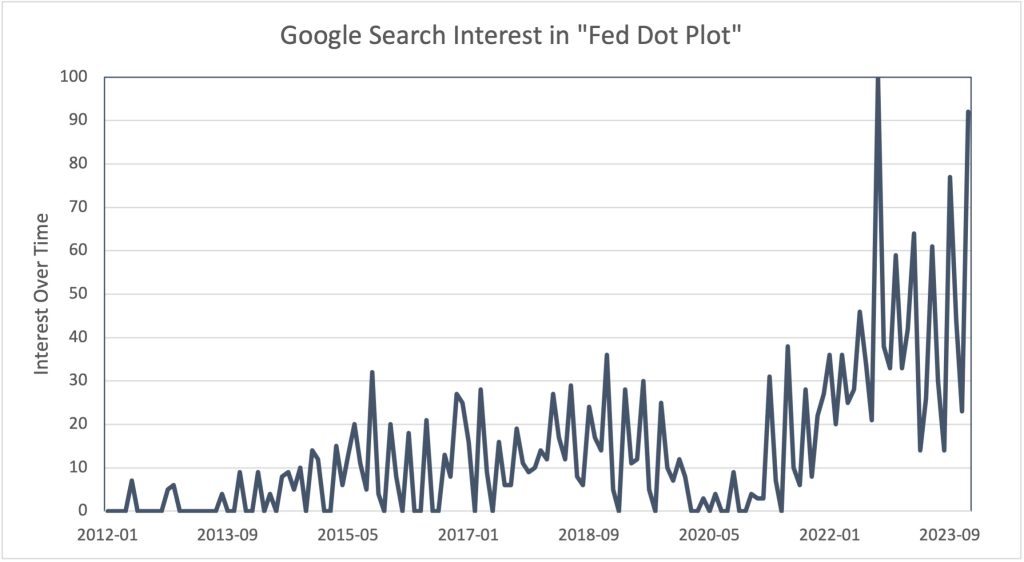

Just as then, investors now analyze and compare iterations of the Dot Plot to gauge the direction (whether hawkish or dovish) of monetary policy. However, unlike then, the popularity of the Dot Plot and the media’s coverage of this once considered “non-event” have seemingly skyrocketed, as evidenced by the Google Search Interest below.

Figure 4: Google Search Interest & Trend for “Fed Dot Plot” 6

Interest Over Time Numbers represent search interest relative to the highest point on the chart for the given region and time. A value of 100 is the peak popularity for the term. A value of 50 means that the term is half as popular. A score of 0 means there was not enough data for this term.

The market’s interpretation of these forecasts has also reflected this new level of “aggression”. Investors don’t have to look far into the rearview mirror to find examples of how the Dot Plot and Fed Funds Futures—a market-derived expectation for the path of interest rates— differ. And as we’ll discover, do at times, differ significantly. To keep consistent with the metaphor, consider the Federal Reserve as a GPS and the market as the driver determining the pace toward the destination. Akin to instances where the GPS leads us to a dead end or nudges us towards violating the speed limit, both the Fed and the market can do the same. And, as has happened frequently, the ramifications can be significant – i.e., when 2022’s “drive” took a more ominous turn, resulting in a “crash”. That year, both the S&P 500 and the Bloomberg U.S Aggregate Bond Index delivered returns deep in the red, down 18% and 13%, respectively, and cemented the bond market benchmark’s worst finish in its 37-year history.

Green Horizons or Optimistic Overshoot?

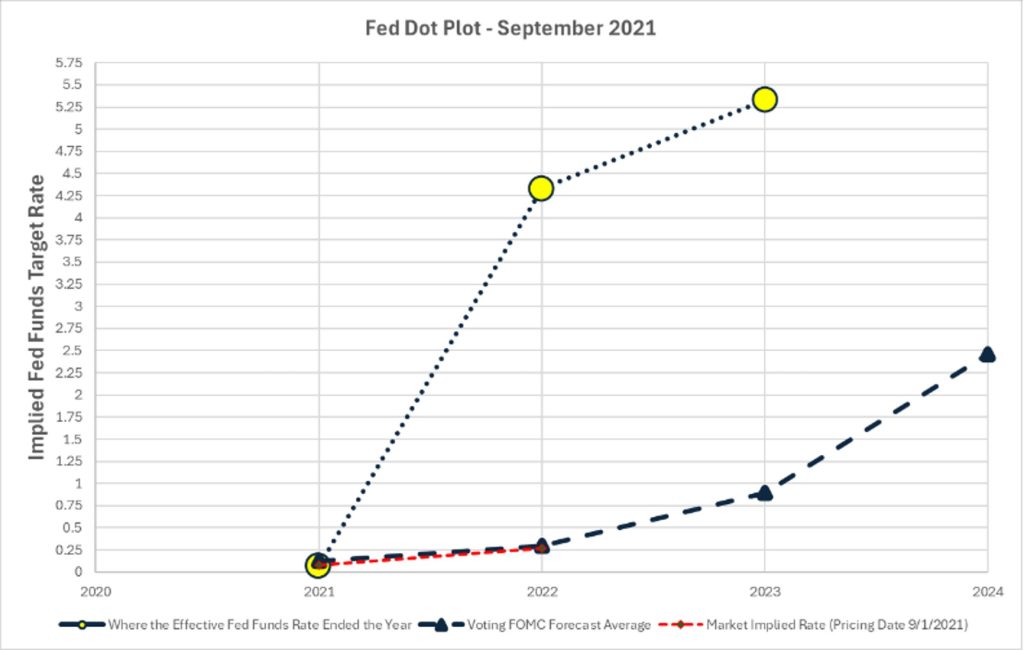

Just a short 23 months ago, interest rates were at historic lows and the Fed Funds target rate range was holding steady at 0% – 0.25%. It isn’t difficult for investors to recall what that environment looked and felt like in 2021. Covid-19 vaccines were being distributed, consumers were flush with cash, and the economy was experiencing robust growth as the “Great Re-Opening” unfolded. Inflation was surpassing the Fed’s target range. Yet, at that juncture, Chair Jerome Powell stated it was transitory and assured the country that rate hikes wouldn’t be required to tame it. His statement echoed the September 2021 Fed Dot Plot, which revealed the FOMC’s average projection for the policy rate at 0.292% by year-end 2022. This equates to just a single 0.25% hike, pushing their target range to 0.25% – 0.50%. Markets seemingly bought this transitory narrative, pricing rates to finish 2022 at 0.273%.

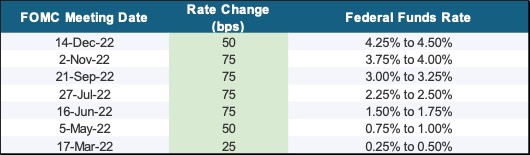

However, by March of 2022, inflation had eclipsed its highest rate in over 40 years. The Fed was forced to act and began increasing rates for the first time since before the pandemic. And, once the Fed decided it was necessary to slay the inflationary dragon, it took decisive action by hiking rates 4.25% over the coming 12 months.

Figure 5: Fed Rate Hikes 2022: Taming Inflation7

This led to one of the widest disconnects in financial market history, as both the Federal Reserve and the market vastly underpriced the economic reality and unpredictability of inflation heading into 2022. The September 2021 Dot Plot, September 2021 Fed Funds Futures Markets, and the realized Effective Fed Funds Rate illustrate this miscalculation (see Figure 6).

Figure 6: Disconnect between Fed Dot Plot, Fed Funds Futures (as of September 2021) and where rates finished7

By the end of 2022, the cumulative effects of restrictive monetary policy required to combat record setting inflation readings resulted in equities delivering its worst year since 2008. Value stocks served as a loan bright spot, outperforming their growth counterparts by the widest margin since the Dot-Com Bubble Burst of the late 1990s. Since its inception, the Barclay’s U.S. Aggregate Bond Index has had only 5 negative years, and 2022 proved to be its worst in history – down 13%. Figure 7 illustrates the performance of the 2-asset classes from September of 2021 (coinciding with the Fed Dot Plot forecast) to the year end 2022 (coinciding with where rates finished).

Figure 7: Performance of US Stocks & Bonds (09/01/2021 – 12/31/2022) 8

The impacts of inaccurate forecasts had potential to outlive 2022, as reputable economists and firms had now forecasted a 100% certainty of a U.S. recession within one year. Bloomberg’s “recession probability model” forecasted “a higher recession probability across all timeframes, with the 12-month estimate of a downturn by October 2023 hitting 100%, up from 65% for the comparable period in the previous update.” 9 However, as described in 2023’s recap, financial markets went on to finish near all-time highs, completely reversing 2022’s trend and ignoring not only Bloomberg’s model, but all models calling for recession in 2023.

Noticeably, the Dot Plot published in December 2023 (See Figure 3) has much greater dispersion in expectations relative to years prior. As of this publishing, their projections call for three rate cuts in 2024, with the FOMC sitting an average rate of 4.704%. 7 Although probabilities have slightly moderated now, at one point Fed Funds Futures (which represent market implied rates) had priced in six rate cuts over the course of the next 12 months. With the unemployment rate still below 4%, GDP growth running at 3% annually, U.S. Core Inflation at 3.93%, real wage growth increasing, and retail sales indicating consumer strength, have investors become disconnected from reality again?7 By historical standards, cutting rates when inflation is around 4% would be considered absurd. The upside of a narrative is that they’re almost always right. But the disadvantage is that they are already reflected in market prices. With risk assets priced to perfection and reaching new all-time highs, the market’s divergence between its interpretation of the Fed’s policy path and the Fed’s stated intentions should come with even greater caution.

“I don’t let people do projections for me because I don’t like throwing up on the desk.”

Charlie Munger

Charlie Munger, the legendary American businessman, investor, and philanthropist (who unfortunately passed late last year), had little time for market forecasters and their prognostications – politely put in comparison to his quote above. 10 Although he was unlikely referring directly to the Fed’s Dot Plot, let’s see if his logic applies!

Four times a year (March/June/September/December), the Fed publishes the predictions of its 19 participants. By examining past dot plots and comparing those rates to where rates actually finished, we can assess whether the Fed’s projections are historically predictive. We can measure the strength and direction between the 2 variables (FOMC’s Forecasts and the Effective Fed Funds Rate at year-end) by running a correlation analysis. Correlation is a statistical measure that describes the extent to which two variables change together. Correlation is often represented by a number called the correlation coefficient, which ranges from -1 to 1. A positive correlation means the variables move in the same direction (both increase or both decrease), while a negative correlation means they move in opposite directions. The closer the correlation coefficient is to 1 or -1, the stronger the correlation. And if it’s closer to 0, there’s a weak or no correlation. In simpler terms, it helps us understand whether there is a relationship between two things and how strong that relationship is. Although the computation comes with inherent limitations (implying causation, sensitivity to outliers, assuming homoscedasticity, limited sample size etc.), its application in this context provides valuable insight. And with (or without) surprise – forecasting interest rates gets cloudy.

Using September and December Dot Plot reports since 2012 11, the FOMC’s short-term projections, covering approximately a 3-month to 2-week period until year-end, have consistently aligned closely with the year-end effective funds rate. The correlations between the projection and the actual rate stand at an impressive 0.997896 and 0.9994548, respectively.

Using March and June Dot Plot reports since 2012 11, although lesser in strength (i.e. lower correlation coefficient), their forecasts are also in harmony. Correlations stand at 0.897486 and 0.979232, respectively.

This high correlation should not come as a surprise. By September and December, the FOMC has presumably thoroughly discussed its policy outlook for the remainder of the year and is unlikely to make significant deviations from its projected course. However, the FOMC’s accuracy suffers materially when we extend their gaze beyond the short-term and into the following year’s end.

Using September and December Dot Plot reports since 2012 11, the FOMC’s projections covering approximately a 15- to 12-month period, stand at 0.559553 and 0.690898, respectively.

Using March and June Dot Plot reports since 2012 11, the FOMC’s projections covering approximately a 24 to 18-month period, stand at 0.165848 and 0.454774, respectively.

Furthermore, the FOMC’s forecasts for interest rates 2 years out by the end of that year are particularly surprising.

Using September and December Dot Plot reports since 2012 11, the FOMC’s projections covering approximately a 27- to 24-month period, stand at -0.529200 and -0.306760, respectively.

Using March and June Dot Plot reports since 2012 11, the FOMC’s projections covering approximately a 33- to 30-month period, stand at -0.420148 and -0.576766, respectively.

As the data suggests, the picture changes drastically when forecasting rates past the very short term (approx. 3-12 months). In fact, history shows investors would arguably have been better off positioning their portfolios for the exact opposite of the Fed’s two-year dot plot average prediction. The lesson to be learned is that we ought to derive insights from fundamentals instead of solely concentrating on momentum from swings in the Federal Reserve’s preferences, expectations, or (put directly) guesses regarding the long-term behavior of interest rates.

Summit Snapshot: Navigating the Essence of it All.

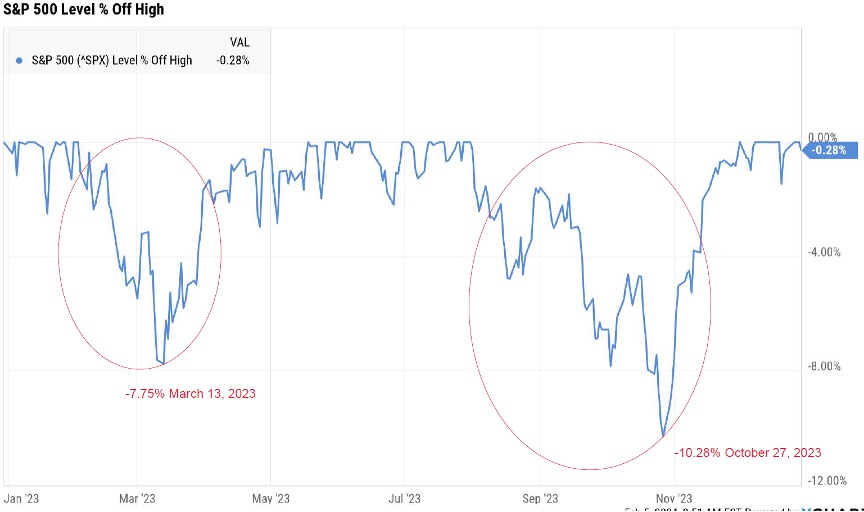

While it is tempting to seek the Holy Grail of accurate forecasting, the reality is that both equity and fixed income returns are inherently difficult to predict. We emphasize the shortcomings of the Fed Dot Plot not as a form of criticism – as we acknowledge the Fed is doing the best it can – but as a fair warning that attempting to predict rates tends to produce poor results. And as we see in the illustration below, episodes of volatility arise when financial markets grow concerned when consensus expectations significantly deviate from Fed Policy.

Figure 8: Bumpy Road when the Fed Fails to Meet Market Expectations (12/31/2022 – 01/31/2024) )8

The economy, particularly inflation and maximum employment, is the driving force behind the Fed’s interest rate decisions. Staying true to a data dependent process, acknowledging the limitations of forecasting, and focusing on managing risk can help investors navigate the labyrinth of the markets with greater confidence.

As we look ahead, we anticipate economic tailwinds diminishing and headwinds intensifying, especially in the context of tighter monetary policy, decelerating growth, and a reduction in fiscal stimulus that helped boost employment and spending. Given these factors, we believe that investors should proceed with caution. While we maintain our long-term investment perspective and manage portfolios accordingly, we remain vigilant in this rapidly evolving environment, actively seeking tactical opportunities to capitalize on market dislocations to mitigate risk and enhance returns. We look forward to sharing these perspectives, allocation shifts, and new investment opportunities in more detail with our valued clients during upcoming conversations. In the meantime, please do not hesitate to reach out to the Aaron Wealth team with any questions.

DISCLAIMER *Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated in the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward-looking statements as a result of factors beyond our control. Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.

Introduction

In the 1990s, an instructional reference book series soared to fame as non-intimidating guides for readers new to various topics. As its popularity grew worldwide – to the point of attracting a cult following of “collectors” proudly displaying each edition on their bookshelf – the series expanded rapidly to around 2,500 titles available in numerous languages. Like so many other nascent businesses, an industrious mind identified a burgeoning trend and capitalized on the untapped market demand with a product geared towards evolving consumer preferences. In this case, the creators of the For Dummies franchise catapulted to instant success because they accurately presaged a world that was becoming increasingly information-rich but time-poor and then introduced a clever solution. Sadly though, its once-promising prospects would soon be thwarted by the advent of the Internet – which could offer the consumer vastly more content, instantly and free of charge. However, we argue that there is at least one use case where a comeback would be both highly impactful and enthusiastically received across the globe: Public Policy. Unlike earlier titles, the intended audience wouldn’t be the everyday novice seeking basic proficiency or a broadened skillset. Instead, Public Policy for Dummies would be targeted to the “expert class” as required reading for all current and future policymakers prior to assuming their post. We presume taxpayers would gleefully pick up the tab for funding this new program, as its relatively low cost would be more than outweighed by its overwhelming benefits. To ensure compliance and guarantee ease of comprehension, we recommend that this edition be only one page in length consisting of three easy steps:

Step 1: Recognize, accept, and acknowledge the reality of major policy issues smacking you in the face. Fight the instinct to deny their existence, downplay their risks, or silence those sounding the alarm – even if politically unpalatable.

Step 2: Do something to address the most concerning issues first, without making matters worse. If your policy ideas would exacerbate the problem, do nothing at all.

Step 3: Repeat Steps 1 & 2 (in that order).

Obviously, this proposal – a hyperbolic and overly simplistic solution to a complex problem – is intended solely as satire. It is merely our attempt at humorously underscoring the serious, real-world consequences of recent public policy action (or inaction). In our January 2022 market commentary, The Inflation Spiral Everyone Could See Coming, we discussed in detail how the current inflation cycle was easily foreseeable and not at all transitory. Had policymakers implemented any number of responsible measures at their disposal to address the looming crisis – or at least avoided aggravating an already precarious situation – the severity of inflation’s painful repercussions on consumers, workers, asset prices, and the economy could have been mitigated or potentially avoided altogether. However, after appearing to have peaked in June 2022, inflation’s significance as the primary determinant of growth prospects and in policymaking calculus should steadily subside over the next 12 months. For this reason, it is imperative that we now recalibrate our priorities from solely focusing on the short-term battle being fought to preparing for what may lie ahead. In our view, the potential fallout from the accumulation of misguided policy decisions since the COVID-19 pandemic will shape the economic landscape investors must reckon with in the coming years. And, as we discuss in more detail later, limiting the damage from this fallout and repairing structural issues that continue to deteriorate will require a coherent set of proactive policy solutions.

Where We Are Now: A Recap of 2022

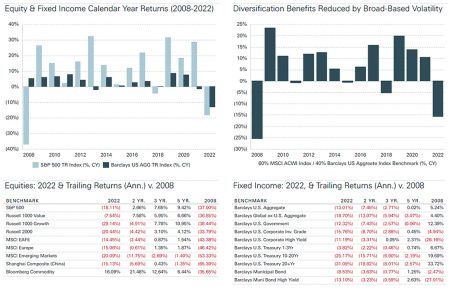

Markets closed out 2022 with the worst calendar year performance since 2008 as inflation, monetary policy tightening, slowing growth, the Russia-Ukraine war, China’s “Zero-Covid” measures, and other geopolitical events tore through the global economy and upended the optimism of the post-pandemic boom. This confluence of factors led to most major asset classes moving increasingly in tandem, and the ensuing volatility wreaked havoc across the investment universe. Both equities and fixed income markets suffered their largest annual declines in 15 years with the S&P 500 Index down more than -18% and the Barclays U.S. Aggregate Bond Index losing -13%. Unlike in 2008, fixed income provided little benefit to downside risk mitigation or volatility dampening as rapidly rising rates inflicted double-digit declines upon wide swaths of the universe. As a result, the frequently referenced model for a diversified portfolio – a 60% Global Equity and 40% Investment Grade Fixed Income allocation – struggled mightily on its way to finishing the year down almost -16% (see Figure 1). Financial assets with higher correlations to inflation (e.g., commodities, infrastructure), an appreciating U.S. dollar, or rising interest rates significantly outperformed during this period. Illustrative of the latter, the effect of rate volatility on disparate equity styles was stark. Value and Dividend stocks – companies with stronger current cash flows and lower valuation multiples – materially outpaced Growth stocks, which have higher future earnings potential and frothy valuations more sensitive to changes in interest rates (as measured by Russell 1000 Value Index, -7.54% and Russell 1000 Growth Index, -29.14%).

Figure 1: Calendar Year Trailing Market Returns (12/31/2007 to 12/31/2022)1

Capital markets were plagued by large swings in momentum and elevated uncertainty as investors oscillated in their collective outlook for inflation, interest rates, and the economy. All in all, 2022 proved to be a landscape in which bottom-up fundamentals played almost no part in the setting of price levels. And it is likely that this pattern will continue throughout 2023 given the persistent divergence between the market’s expectations for future monetary policy and the Fed’s planned course of action. The more these forecasts deviate from one another, the greater the turbulence that will be injected into trading when investors are ultimately forced to reconcile their opinions with reality.

Where We Go from Here: Reckoning with the Pandemic & Inflation Fallout

Understanding that prudent preparation now will be pivotal to successfully navigate the post-inflation world, we have bifurcated our outlook to address two distinct environments we anticipate encountering going forward. The first encompasses the near-term period – approximately the next 12 months – where inflation will remain a material factor in prevailing conditions. Then, looking further out on the horizon, the second period seeks to evaluate the fallout from policy choices made over the past several years and their potential for aggravating longer-term structural issues that have been building for some time. For clarity, we outline each separately in the following two sections.

Part I – Fighting the Fed is a Fool’s Game

As we embark on a new year with inflation marching steadily lower (U.S. CPI came in at 6.4% for January from 9.1% in June 2022; U.S. CPI ex-Food & Energy was 5.6% in January down from 6.6% in September 2022),² the consensus has grown increasingly convinced that the Fed has done enough to slay the inflation dragon and is quickly approaching the end of this monetary tightening cycle. This view is reflected by current market data that has priced in two final 0.25% rate hikes (one of which came in February), rate cuts in the second half of the year, and headline inflation falling to 3.7% by year-end.³ With conviction around this view solidifying further since December, interest rates began a retracement, positive sentiment gathered momentum, and both equities and fixed income experienced a significant relief rally. However, our confidence that this is anything more than a short-lived trend is close to zero.

Our outlook for 2023 remains consistent and little changed from the past 12-24 months. We believe that inflation and interest rates will prove to be sticky for some time, lingering at higher levels for longer than current forecasts suggest. Despite recently announced layoffs across certain sectors and a slight slowing of wage growth, the U.S. labor market’s resilience in the face of tightening financial conditions has defied expectations of late and might even be picking up steam. January’s surprising employment report saw an acceleration of job growth as employers added 517,000 jobs (nearly three times more than expected), previous month’s figures were revised materially higher, and the unemployment rate fell to a 53-year low of 3.4%.4 Job openings ticked up as well. With about two open positions for each person currently seeking a job, demand for labor continues to significantly outstrip available supply.5 While large cuts by companies like Amazon and Microsoft may make headlines, the tech-heavy information sector makes up only 2% of all private sector jobs. In contrast, service industries – such as healthcare, education, leisure and hospitality – account for 36% of private payrolls and 63% of all job growth over the past six months.6 These latest monthly reports have not only reversed five months of slowing growth, but they portend a scenario where employment and wage growth are likely to resume putting upward pressure on inflation.

Economic data of this ilk is backward-looking and notoriously difficult to forecast. Thus, the extrapolation of a singular month’s data into the future would be highly susceptible to error and provide negligible predictive value. So, for argument’s sake, we set it aside to assess the substance of other factors which may influence how 2023 unfolds.

Dating back to 1970, a cardinal rule of sound portfolio management has long been “Don’t Fight the Fed.” Its invocation is so ubiquitous – such that even amateur investors grasp the concept – because of its perfect record against those who fail to heed the warning. Yet today, for some inexplicable reason, market participants have assured themselves that their elusive first win is finally within reach; this time things will be different. For more than a year now, Fed Chairman Jerome Powell has been transparent and clear in his communications outlining the policy steps the central bank would take to break inflation while consistently emphasizing their commitment to achieving this goal. Here are a few recent examples:

Given the outlook, I don’t see us cutting rates this year.

We’re going to be cautious about declaring victory and sending signals that the game is won.We’re in the early stages of disinflation [and it’s] going to take time.

We think we’re going to have to do further [rate] increases, and we think we’ll have to hold policy at a restrictive level for some time.

We’re going to react to the data. So if we continue to get, for example, strong labor market reports or higher inflation reports, it may well be the case that we have to do more and raise rates more than has been priced in.7

In our opinion, this is indisputable evidence of the Fed’s planned course of action. How anyone could interpret such explicit, unambiguous language and arrive at a contradictory conclusion strains credulity. Has the investment community lost faith in the central bank or Jerome Powell? Is he not credible? Do investors really want to bet that the Fed lacks the fortitude to follow through on their plans? Trying to surmise why the Fed’s intentions are becoming so distorted as each statement is released, digested, and then translated into market pricing leaves us scratching our heads. Maybe it’s simply a case of mass-scale wishful thinking.

Consequently, we again find ourselves playing the role of contrarian. Going along with the “wisdom of the crowd” is often comforting because evolutionary conditioning has taught us there is safety in numbers, but just as often, it is a false sense of security luring us into a dangerous trap. Given a dearth of evidence to the contrary, we are satisfied that any clear-eyed, unbiased assessment of currently available information, especially those detailed above, would align with the major contours of our thesis. We therefore remain steadfast in our outlook that inflation and interest rates will hold at higher levels for longer than currently anticipated. While there is always a possibility that market dynamics can exhibit irrational characteristics for extended periods, the past year has demonstrated the market’s tendency towards forecasting errors, both in frequency and magnitude. And though this places us back in direct conflict with consensus expectations, the evidence is too compelling to ignore – prudent management requires responsible action to mitigate foreseeable pitfalls. In our estimation, the way portfolios are positioned in relation to inflation and interest rate risk will be a key point of differentiation in realized performance.

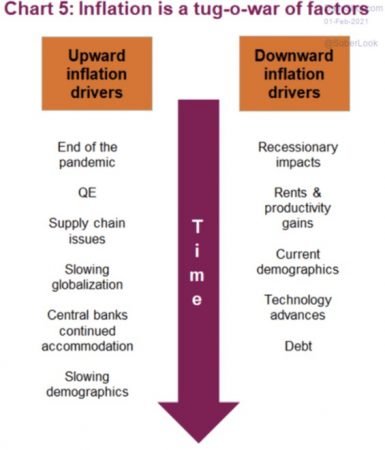

Part II – A Return to Secular Stagnation

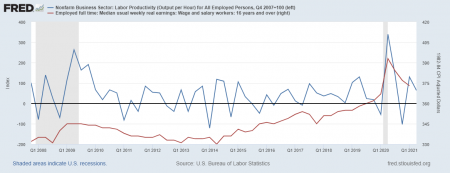

A theory first introduced by the economist Alvin Hansen during the Great Depression, secular stagnation refers to an economy suffering from meager or no long-term growth and structurally low private demand, requiring very low interest rates to boost demand and reach potential output. During the historically sluggish recovery from the 2008 financial crisis, this concept was resurrected in public discourse. For years its validity as a theory as well as its accuracy in describing economic conditions at the time were contentiously debated. While the causes of secular stagnation have yet to be proven empirically, a Bank of International Settlements 2015 paper cites the following potential explanations: “secular deficiency in aggregate demand, slowing innovation, adverse demographics, lingering policy uncertainty, post-crisis political fractionalization, debt overhang, insufficient fiscal stimulus, excessive financial regulation, and some mix of all of the above.”8 Assuming that these hold true, even the casual observer would recognize the tell-tale signs of stagflation’s prevalence in today’s global economy. We highlight a few such conditions in the nearby charts (Figure 2) but, for brevity’s sake, will leave further examination to future dispatches.

Figure 2: Stagflationary Indicators

Conclusion: Portfolio Allocation Update

We conclude with an update on portfolio positioning. Asset classes with strong cash flows, contracted and predictable revenues, and lower sensitivity to elevated interest rates are likely to outperform on a relative basis over the coming period. As such, we remain comfortable with our tactical underweight to Emerging Market equities, U.S. Growth equities, and longer-duration bonds in favor of Value/Dividend equities and short-duration bond sectors. And finally, our strongest short-to-medium term conviction continues to be a shifting of portfolio risk budgets from public to private market exposure (where appropriate). Given that we anticipate muted returns in public markets over the near term, this tactic possesses multiple potential benefits today in our opinion – not only can private assets serve as a risk dampener during volatile markets but, in the current regime, may also increase long-term return potential. As always, we are long-term investors and manage portfolios accordingly. However, in a rapidly evolving environment, we are constantly looking for tactical opportunities to capitalize on dislocations that may produce asymmetric risk-return profiles.

Sources

¹ Addepar

² U.S. Department of Labor, Bureau of Labor Statistics: Consumer Price Index Summary January 2023 released February 14, 2023 – https://www.bls.gov/news.release/cpi.nr0.htm

³ Bloomberg U.S. Economic Forecasts as of February 1, 2023

⁴ U.S. Department of Labor, Bureau of Labor Statistics: Employment Situation Summary January 2023 released February 3, 2023 – https://www.bls.gov/news.release/empsit.nr0.htm

⁵ U.S. Department of Labor, Bureau of Labor Statistics: Job Openings and Labor Turnover Summary December 2022 released February 1, 2023 – https://www.bls.gov/news.release/jolts.nr0.htm

⁶ Wall Street Journal online version: Mass Layoffs or Hiring Boom? What’s Actually Happening in the Jobs Market by Sarah Chaney Cambon and Ray A. Smith on February 9, 2023 – https://www.wsj.com/articles/jobs-hiring-boom-layoffs-employment-11675947399?mod=hp_lead_pos7

⁷ Wall Street Journal online version: Powell Doesn’t See Fed Cutting Rates This Year by Harriet Torry on February 1, 2023 – https://www.wsj.com/livecoverage/federalreserve-meeting-interest-rate-hike-february-2023/card/powell-doesn-t-see-fed-cutting-rates-this-year-2AGm7XzpAgayhyMVKxH; and Fed’s Jerome Powell Braces for Longer Inflation Fight Amid Hiring Surge by Nick Timiraos on February 7, 2023 – https://www.wsj.com/articles/feds-jerome-powell-to-address-economic-outlook-withhiring-surge-in-spotlight-11675781503

⁸ Bank for International Settlements, BIS Working Papers No. 482, Secular stagnation, debt overhang and other rationales for sluggish growth, six years on by Stephanie Lo and Kenneth Rogoff, January 2015 – https://www.bis.org/publ/work482.htm

9 Office of Management and Budget and Federal Reserve Bank of St. Louis via Federal Reserve Economic Data (FRED). “Gross Federal Debt as Percent of Gross Domestic Product.” https://fred.stlouisfed.org/series/GFDGDPA188S. U.S. Department of the Treasury. “The Debt to the Penny.” https://fiscaldata.treasury.gov/datasets/debt-to-the-penny/debt-to-the-penny

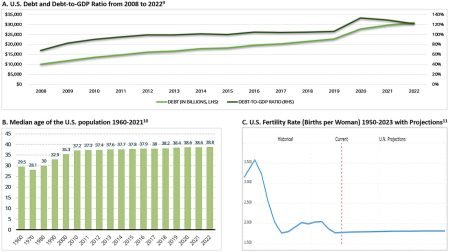

10 US Census Bureau. “Median Age of The Resident Population of The United States from 1960 to 2021.” Statista, Statista Inc., 17 Dec 2021, https://www.statista.com/statistics/241494/median-age-of-the-us-population/

11 United Nations – World Population Prospects 2022. <a href=’https://www.macrotrends.net/countries/USA/united-states/fertility-rate’>U.S. Fertility Rate 1950-2023</a>. www.macrotrends.net. Retrieved 2023-02-13.

DISCLAIMER *Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated in the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward-looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward-looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward-looking statements as a result of factors beyond our control. Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward-looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.

Toby Stannard was featured in Financial Advisor IQ this week. He weighed in on how Aaron Wealth Advisors works with clients to create customized value-based indexes. Read more about it Here.

Afteryearsofbingingonfiscal and monetary excess, markets feel the pain of withdrawals

INTRODUCTION: THE MAKING OF A MONETARY JUNKIE

Back in 2008 the Federal Reserve, along with many major central banks across the world, embarked on an unprecedented and coordinated response to the Great Recession. With standard techniques – such as slashing interest rates to zero – proving ineffective, they argued that a more unconventional monetary policy was required to jumpstart the global economy. Their idea: central banks should buy predetermined amounts of securities (e.g., Treasuries, corporate bonds, mortgage-backed securities) to inject capital into the economy and hold down longer- term rates thereby incentivizing appetites for risk assets and spurring economic activity. In November of 2008, the first round of quantitative easing (QE1) began in the United States. Given its novelty, this program was generally understood to be a short-term policy of last resort reserved for only the greatest of financial crises. Yet, in 2010, the Fed continued with a second round, nicknamed QE2. And in 2012, a third round was launched with an important modification – it would be open-ended, earning the moniker “QE-Infinity.” When Covid-19 shutdown the world in 2020, a turbocharged version of quantitative easing was rolled out. As a result of such sustained monetary policy accommodation, and in combination with historic bouts of fiscal stimulus, global markets have been able to binge on a glut of liquidity, cheap money, and federal backstops for nearly 15 years. Is it possible that we’ve become addicted?

At the beginning, there was ample discussion and concern about how this type of program could be unwound. QE, by design, creates massive distortions in price signals across markets, hence the original intention to be a short-lived, emergency program. With each round of larger and larger stimulus, the potential fallout from withdrawing this support increasingly faded from the conversation. We got a glimpse into our future in the summer of 2013 when the Fed announced it would begin tapering asset purchases. However, this was by no means a turn to monetary tightening. Interest rates would be held steady, but asset purchases would be reduced each month (still historically accommodative by any measure). What followed has come to be known as the “Taper Tantrum” – equities plummeted 4% in the three trading sessions following the announcement and bond yields spiked. Following this, the Fed quickly decided to hold off on scaling back its asset purchases in September.

Such an event reminds one of an important lesson: swiftly cutting off the supply of an addictive substance can be quite dangerous.

WHERE WE ARE NOW: SUFFERING THE EFFECTS OF BINGING & THE PAIN OF WITHDRAWALS

After a punishing first four months of the year, investors experienced some reprieve in May from the battering volatility as most major equity and fixed income indices stabilized to post a positive return for the month. However, the respite was short-lived, proving itself only to be the eye of the storm. Thus far in June, markets continued their downward slide – across asset classes – and increased in intensity. To illustrate the market dynamics at play, imagine a balloon. As stimulus flooded the economy and rates fell, the balloon inflated more and more (valuations expanded, momentum was strongly positive). Then this year, as policy began to tighten and rates jumped, the balloon started to deflate – the more quickly rates spike, the more quickly the balloon deflates (valuations compressed, momentum swung strongly negative). In addition to the withdrawal of stimulus, the current landscape has been broadsided by exogenous shocks and deteriorating economic conditions, including:

Inflation Data: The May reading of S. CPI (released in mid-June) showed no indication that inflation was moderating, coming in at 8.6%.1 This has now become a major concern across the globe. For the same month, Eurozone inflation reached a record-high, hitting 8.1%.2

Energy, Commodities, & Russia’s War in Ukraine: U.S Retail Gas Prices soared to all-time highs averaging $5.10/gallon in June.3 Russia declined a humanitarian-relief proposal for safe shipping routes of crucial commodity supplies through Ukraine. Moscow also cut off the majority of natural gas flows to Europe through the Nordstream Pipeline, raising concerns about insufficient heating for this winter and sending market prices about eight times higher than seasonal averages.4

Monetary Policy: Contrary to previous guidance, the Federal Reserve hiked its policy rate 0.75% at its June meeting and left open the potential for the same in July. Concurrently, central banks across the world began to accelerate or signal tighter-than- expected monetary policies to combat inflation.

Profit Warnings by Businesses: some companies, especially in the retail sector, issued warnings for earnings guidance as they reported needing to “right-size” large accumulations of inventory.

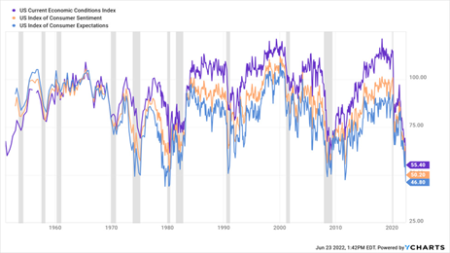

While lagging U.S. economic and employment data remain strong, forward-looking indicators have begun to show how pervasive and pessimistic the collective outlook has become. Indices of U.S. Surveys for Current Economic Conditions, Consumer Sentiment, and Consumer Expectations all recently plummeted to record or near-record lows (see Figure 1 nearby). In a marked reversal from the first quarter, the majority of CEO’s surveyed over the past month now believe the U.S. economy will be in a recession in the next 12-18 months. Typically, in similar periods of heightened volatility, broad-based selloffs, and market gloom, we would be chomping at the bit to deploy long-term capital and scoop up assets at attractive discounts. However, as will be discussed in more detail in the next section, today’s environment has a small, albeit material, probability for negative snowballing, with downside risks accumulating as conditions worsen.

Figure 1: US Consumer Survey Indices (Inception – June 2022; gray shading denotes recession)5

WHERE WE GO FROM HERE: RECESSION APPEARS UNAVOIDABLE

We find no solace in the fact that markets, central banks, and policymakers are finally waking up to the reality of today’s inflation problem that we, and others, have been warning about since late 2020. In fact, their tardiness further exacerbates our concerns that those currently responsible for setting policy are ill-equipped to competently navigate through this period of instability. The June Fed meeting and Chairman Powell’s subsequent conference demonstrated that monetary policy is and may remain behind the curve to tame inflation. On the fiscal policy front, we do not believe that any of the proposed solutions recently posited by Congress or the current administration will alleviate the inflation problem. Furthermore, some of these proposals that increase stimulus (prepaid gas cards, student loan forgiveness, etc.) and supply-side disincentives (price controls, increased corporate/personal income tax, heightened regulations, etc.) may actually exacerbate price increases. Monetary policy can only intervene via the demand side of the economy, which means to tame inflation it must dampen aggregate demand. Since we see no realistic scenario on the horizon where fiscal policy steps in to address the imbalance on the supply side (i.e., through reduced tax/regulatory burdens, incentives for energy production and business investment), we anticipate that higher inflation will persist longer and rates will increase further than currently anticipated by markets – despite some cushion between today’s current Fed Funds rate and the short end of yield curves. As such, absent some positive exogenous shock, our base case is that the U.S. and global economy will be in a recession in the next 12 months, with the next 3-6 months proving critical to the duration and severity of any slowdown.

At this point, it is important to remember that economic data is backward-looking while markets are forward-looking. To that end, should inflation be quelled without crushing demand, then any ensuing recession would likely be mild, and the worst of the market pain could potentially be behind us. To clarify, our base case scenario is in no way an advocation for the elimination of certain asset classes, like fixed income. We remain long-term investors and manage portfolios accordingly. However, we are quickly working through various new strategy options to protect against what could be a relatively tumultuous 12-24 months, in addition to what has already been implemented. A few, but certainly not an exhaustive list, of the potential arrows in our quiver for downside risk mitigation include:

Tactical Tilt Towards High-Quality and Value: High-quality, attractively valued companies with wide moats and stable and consistent cash flows have historically outperformed in recessionary environments. This would accomplish a two-pronged objective of tilting towards an outperforming style while simultaneously reducing exposure to (what should be) an underperforming style – growth. Growth equities, which have a greater share of earnings expected in the future, are relatively harder hit in a rising rate environment as future cash flows are discounted to be less valuable.

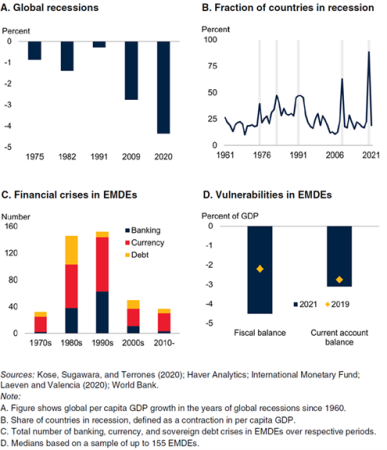

Tactical Underweight to Emerging Markets: Emerging Markets, while highly idiosyncratic, have historically struggled during risk-off and monetary tightening cycles. Developing economies with high levels of indebtedness relative to GDP and/or large shares of foreign currency denominated debt frequently experience the greatest amount of pain. This was evident during the Great Inflation period of the late- 1970’s to early-1980’s, which saw a slew of financial and currency crises arise in Emerging Market (EMDE) economies following the global recession triggered by policy tightening to fight inflation in Advanced Market (AM) economies. As EMDE currencies depreciate relative to AM currencies, AM interest rates rise, and/or AM economies enter recession, EMDE foreign currency denominated debt becomes increasingly expensive to service and AM capital flees to perceived safe haven assets. As a result, EMDE economies frequently spiral into crises (see Figure 2 nearby).

Shift Towards Short-Term, Quality Corporate Credit: Since late 2020, we have been diligently focused on reducing our exposure to interest rate risk within the fixed income sleeve. One solution to this was increasing allocations to securitized sectors of the fixed income universe. With this came greater exposure to the health of S. consumers via credit card debt, auto loans, residential mortgages, etc. In a recession, downside risk could be mitigated and relative performance enhanced by shifting towards short-term, high quality corporate debt and credit.

Intelligently Designed Structured Notes: We have recently designed various structured notes for analysis that possess attractive asymmetric risk-return profiles and For instance, with a high degree of principal protection, we could earn higher-than-market yields relative to fixed income while further reducing interest rate risk and retaining levered-upside equity participation should markets rebound over the next several years.

Figure 2: End of Stagflation of the 1970s & Vulnerabilities in EMDEs6

These decisions have become our top due diligence priority as implementation-timing is critical to successful outcomes. We will communicate these changes to each client, as pertinent and appropriate. Our intent with this communication is not to sow fear or concern. Rather, we believe our clients deserve timely and transparent insight into our outlook, the reasoning that underpins it, and the steps we are taking to address the potential risks we see on the horizon. In addition, all investors should be clear-eyed in their expectations when prevailing circumstances signal choppy waters ahead. As always, please feel free to reach out to our team with any questions, comments, or concerns.

Sources

1.YCharts; U.S. Bureau of Labor Statistics; Consumer Price Index Report for May 2022; https://www.bls.gov/news.release/cpi.nr0.htm

2.Eurostat; Euro Area Inflation for May 2022; https://ec.europa.eu/eurostat/documents/2995521/14644605/2-17062022-AP-EN.pdf/1491c8b5-35e4-cdec-b02a- 101a14a912ad

3.YCharts; U.S. Energy Information Administration; Weekly Retail Gasoline and On-Highway Diesel Prices Report for June 13th, 2022

4.Bloomberg online edition; European Gas Extends Gains as Specter of Russian Cuts Persists by Anna Shiryaevskaya; June 21, 2022; https://www.bloomberg.com/ news/articles/2022-06-21/european-gas-rises-again-as-supply-crisis-spreads-across-region

5.YCharts; University of Michigan; University of Michigan Surveys of Consumers Report for June 2022

6.World Bank. 2022. Global Economic Prospects, June 2022. Washington, DC: World Bank. doi: 10.1596/978-1-4648-1843-1. License: Creative Commons Attribution CC BY 3.0 IGO

Disclosures

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated on the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward looking statements as a result of factors beyond our control.

Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.

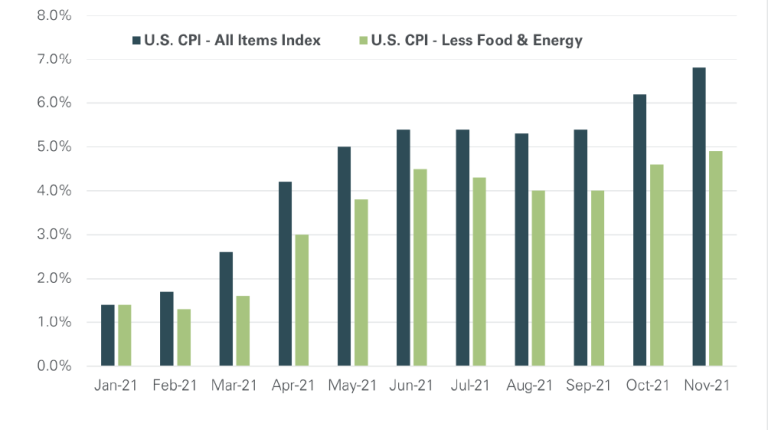

On December 10th, the U.S. Bureau of Labor Statistics released its monthly Consumer Price Index (CPI) report for November. For most, the data quantified the day-to-day financial changes they had been experiencing for months now. The all-items CPI index jumped 6.8% over the previous 12 months, the largest increase since June 1982.¹ Interestingly, markets responded positively with the S&P 500 closing up nearly 1% that day,² likely because the number was in-line, rather than above, expectations. The Federal Reserve’s preferred gauge of inflation, the CPI Index excluding the often-volatile categories of food and energy, rose 4.9% over the same period. We have now experienced an 8-month surge of increasing inflation from 4.2% in April to November’s reading of 6.8%.¹

The frequently touted fallacy that price increases would be transitory – based on the argument that supply chain distortions would naturally resolve themselves as the global economy emerged from the pandemic and year-over-year inflation readings would soon end their measurement against the depressed levels of the 2020 recession – never held up to even casual scrutiny. Finally realizing the absurdity of the claim, Jerome Powell officially ditched the “transitory” tag from the Fed’s language and outlook regarding inflation during Congressional testimony at the end of November. After its December meeting, the Fed also announced that it would hasten its tapering of asset purchases – known as quantitative easing – and penciled in a potential for three rate increases in 2022 (previously, policy rate increases weren’t expected until 2023). While this is a step in the right direction, it may be too little too late to contain the problem without inflicting material economic harm. Moreover, monetary policy is only one component in the morass of government functions which contribute to the overall success or failure of economic management.

Perhaps the most frustrating aspect of this reality, as investors and individuals, is the lack of recourse available to quickly right the ship when mismanagement becomes so readily apparent and pervasive. Evidence of inflationary pressures have been mounting for some time now and warning signs pointing to the increasing risk were glaringly obvious to almost anyone paying attention. To wit, we have consistently sounded the alarm – along with a multitude of others possessing far greater public prominence – about the growing probability of runaway inflation since the late summer of 2020. Yet, instead of pivoting when their prior assumptions proved inaccurate, those tasked with managing and crafting public policy routinely exacerbate conditions by implementing counterproductive or ineffectual programs that further stoke the inflationary flames. But more on that later…

Part I: How We Got Here First, some background and context are required to better understand the current landscape. In lieu of a lengthy recitation of technical minutiae, the four main drivers of inflation in an economy can be summarized as follows: i. an increase in the money supply ii. a decrease in the demand for money iii. a reduction in the aggregate supply of goods/services due to higher production costs (e.g., raw materials, wages, tariffs, taxes, and other inputs) iv. an excess in aggregate demand from consumers, businesses, government, or foreign buyers