WHERE WE ARE

Investors with a sense of history may recall that the month of August has on occasion featured meaningful developments creating significant impact on financial asset prices. August 1991 saw the breakup of the Soviet Union; August 1998 witnessed the Russian debt default and ruble devaluation; August 2011 brought the Standard & Poor’s debt downgrade of U.S. Treasury securities; and August 2015 contained the surprise Chinese currency devaluation, which led to the first-ever 1,000 point drop in the Dow Jones Industrial Average. Over the period from 1980 through 2019, the average monthly S&P 500 stock market return for August (-0.15%) is the second lowest of all twelve months (behind September, -0.70%).

The late June to August 21st portion of this historic restoration of equity price levels has been achieved amongst numerous important background developments, including, among others:

i. Persistent erosion of the U.S. dollar, with seven out of eight weekly declines in the DXY index, from 97.50 on June 26th to 93.20 on August 21st;

ii. Range-bound U.S. Treasury interest rates throughout June, July, and mid-August, with 10-year yields fluctuating between 0.52% and 0.71%, and 30-year yields fluctuating between 1.18% and 1.43%;

iii. A gradually declining trend in the VIX volatility index, as featured by successive weekly closes of 34.73, 27.68, 27.29, 25.68, 25.84, 22.21, 22.46, 22.05, and 22.54;

iv. Modest firmness in West Texas Intermediate crude oil prices, rising in six out of eight weeks, from $38.49 per barrel on June 26th to $42.34 per barrel (+10.0%) on August 21st;

v. Generally rising gold prices, up six of eight weeks, from $1,772.50 per troy ounce on June 26th to $1,934.60 (+9.1%) on August 21st;

vi. A +27.2% increase in bitcoin pricing, from $9,162.92 on June 26th to $11,659.01 on August 21st;

vii. In contrast to the year-over-year 2Q20 increase in China’s real GDP of +3.2% (after a -6.8% year-over-year contraction in 1Q20), deep quarter over quarter real GDP declines were experienced in 2Q20 for Japan -7.8% (-27.8% annualized), the U.S. -9.5% (-32.9% annualized) and Europe -12.1% (-40.3% annualized);

viii. Despite local limitations/prohibitions on mass gatherings, lockdowns, mask requirements, mandatory quarantines, and social distancing, as of Monday morning, August 24th, the U.S. had reported more than 177,000 deaths due to COVID-19 and more than 5.72 million confirmed infections, representing 24.4% of the world’s more than 23.4 million cases and 21.9% of the world’s more than 809,000 deaths; and

ix. Continuing investor focus on, and demand for, an increasingly limited number of specific stocks in the technology sector (for example, Apple, which rose +40.6%, from $353.83 on June 26th to $497.48 on August 21st) as well as certain “concept stocks” (for example, Tesla, which increased +113.6%, from $959.74 on June 26th to $2,049.98 on August 21st).

The following sections contain our evaluation of what we consider to be important positive and negative influences on financial asset prices in the period ahead, followed by our recommended portfolio positioning.

BULLISH/CONSTRUCTIVE FACTORS AND INFLUENCES

1. Assumption of Continued Monetary Stimulus: While financial market participants have expected recent statements by Federal Reserve governors to reflect growing confidence in the outlook, bolstered by some signs of a recovering economy and rising stock prices, instead, with a sobering assessment of the economic backdrop, the Fed’s monetary policy message has cited an increasing spread of the coronavirus since mid-June, together with the slowing of many states’ reopening of businesses, the need for more fiscal assistance, and a preference for policy interest rates to be kept close to zero through the end of 2022. In its updated June economic projections, the Federal Reserve expects year-end 2022 unemployment to be at 5.5%, with consumer price inflation at 1.7%, still below the Fed’s 2% target level. As a result, expectations are in place for: (i) the maintenance of low interest rates, primarily in the shorter-maturity portion of the U.S. Treasury yield curve; (ii) continuation of the Federal Reserve’s extensive array of credit and lending support programs; (iii) further expansion of the Fed’s multitrillion-dollar balance sheet; (iv) Quantitative Easing (“money printing”) to purchase various types of governmental, mortgage-backed, and corporate fixed income securities; and (v) “debt monetization,” commonly perceived to be money creation by the central bank to finance a significant part of large budget deficits by the federal government. Minutes from the July 27th-28th Federal Open Market Committee meeting indicate that voting members expressed little enthusiasm for “yield curve control,” (generally interpreted to encompass targeting intermediate- and longer-term interest rates and pledging to buy long-term U.S. Treasury bonds). In the near future, the Federal Reserve is expected to announce revisions to its policy framework and the guiding principles it intends to follow when setting interest rates and other monetary policies.

2. Expectations of a 2021 Pickup in GDP and Corporate Profits: In the June 10th economic projections of Federal Reserve Board members and Federal Reserve Bank presidents, after an expected decline of -6.5% in U.S. GDP in 2020, U.S. GDP is forecast to grow +5.0% in 2021 (and +3.5% in 2022). According to FactSet and Refinitiv, as of early August, “bottom-up” projections by security analysts were calling for: (i) in 3Q20, a year-over-year S&P 500 earnings decline of -22.9% and a revenue decline of -4.4%; (ii) in 4Q20, an earnings decline of -12.8% and a revenue decline of -1.4%; (iii) in calendar year 2020, an earnings decline of -19.0% and a revenue decline of -3.2%; (iv) in 1Q21, earnings growth of +12.9% and revenue growth of +3.1%; and (v) in calendar year 2021, earnings growth of +26.5% and revenue growth of +8.4%.

3. More Constructive Economic Picture: Improvement has been registered in:

i. Employment conditions, with (after -20.7 million lost jobs in April, +2.7 million jobs added in May, and +4.8 million jobs added in June) +1.8 million jobs added in July, a 10.2% unemployment rate, (down from 11.1% in June) and weekly state unemployment benefit claims falling below 1.0 million for the first time since March (even though they rose again to 1.1 million the following week);

ii. The Housing Sector, with July Housing Starts up +22.6%, the largest monthly gain since October 2016, and July Building Permits (a more forward-looking metric) up +18.8%, as the National Association of Home Builders Confidence Index reached 78 in August, matching the all-time high set more than 20 years earlier; July Existing Home Sales rose +24.7% month-over-month, the largest percentage gain since the data began being released in 1968;

iii. Retail Sales, which have managed to claw their way back to +1.7%, or $8.7 billion, above February 2020 levels (month-over-month, they were -8.3% in March, -14.7% in April, +17.7% in May, +8.4% in June, and +1.2% in July);

iv. Institute for Supply Management surveys of Purchasing Managers (with readings above 50 indicating expansion), where July’s ISM Manufacturing index reached 54.2 vs. 52.6% in June, and July’s ISM Services index hit 58.1, versus 57.1 in June;

v. Durable Goods Orders, up +7.3% in June month-over-month, following a gain of +15.1% in May; and

vi. Industrial Production, positive +3.3% month-over-month in July, after rising 5.7% in June.

4. Meaningful Cash Levels on the Sidelines: Considerable potential buying power for risk assets resides in the sizeable aggregate balances in taxable and tax-free money market funds, which have grown from $3.6 trillion at the beginning of 2020 to $4.6 trillion in mid-June.

5. News of Vaccine Progress: Global asset prices have shown a proclivity to rally, or fade, when substantive coronavirus vaccine advances, or disappointments, are announced in dosing, toxicity, safety, efficacy, immune response, side effects, and manufacturing. Trials are being conducted along several scientific pathways, among them: messenger RNA-based approaches; DNA-based approaches; non-replicating viral vector approaches; replicating viral vector approaches; and protein-based approaches. If a vaccine can be found that induces sufficient levels of neutralizing antibodies to protect people safely from the disease, financial assets would likely experience a short-term price increase, possibly a meaningful one. The sustainability and magnitude of such a move (even if numerous companies launch a vaccine at the same time) will be largely determined by the length of time necessary before humanity achieves sufficient immunity to the disease.

BEARISH/CAUTIONARY FACTORS AND INFLUENCES

1. Continuing Unknowns Associated with the COVID-19 Pandemic: With the path of the economy highly dependent on the course of the coronavirus and the private and public sectors’ response to it, significant unanswered questions include:

i. The likely course, extent, and severity of the disease as the weather changes and the influenza season approaches;

ii. The extent of lingering symptoms and duration and degree of potential immunity associated with having tested positive for and/or having recovered from the coronavirus;

iii. Whether, how, and when cities, regions, the United States, and other countries can reach “herd immunity” (defined by the Centers for Disease Control and Prevention as “when a sufficient proportion of a population is immune to an infectious disease to make it unlikely to spread among people”);

iv. The efficacy of and compliance with various restrictions enacted in different states, countries, and regions to stop the virus from spreading;

v. The effects on students, families, teachers, and staff of differing approaches to in-person versus remote learning and to divergent protocols for opening various levels of the education sector; and

vi. With more than 180 coronavirus vaccine candidates being developed by researchers around the world (138 in the pre-clinical stage, 25 in Phase I trials, 15 in Phase II trials, and 7 in Phase III trials), details as to the speed, safety, and degree of success in the development, manufacturing, distribution, and public acceptance of preventative vaccines and/or therapeutic treatments for the coronavirus.

2. Anxiety as to the Timing, Size, and Forms of Additional Funds from Congress: With some stimulus provisions expiring and others scheduled to expire against the backdrop of a still-weak labor market, and as the White House-ordered enhanced unemployment insurance offers some degree of relief for less-advantaged households, struggling businesses, and vulnerable economic sectors, Washington’s lawmakers have remained stuck at an impasse. Financial asset prices may be adversely affected by the more than $2 trillion chasm separating the proposals of the two political parties, not to mention lingering sharp intraparty divisions over some elements of further economic aid.

3. Stretched Valuations: As of mid-August, the forward price-earnings ratio of the S&P 500 index was 22.3, considerably above its five-year average (17.0), as well as its 10-year average (15.3). Among other valuation indicators that appear extended are: (i) the so-called “Buffett Ratio,” which Warren Buffett calls “probably the best single measure of where valuations stand at any given moment.” Representing the percentage of U.S. equities’ total market capitalization relative to aggregate U.S. GDP, at 178%, this indicator is considered to be significantly overvalued; and

(ii) the Cyclically Adjusted Price Earnings ratio (also known as the CAPE ratio, or the Shiller ratio, named after its creator, Yale Professor and 2013 Nobel Economics Laureate Robert Shiller), representing prices divided by cyclically-adjusted 10-year average earnings after inflation; at a recent level of 31.0, this indicator is considered to be 20.6% overvalued versus its recent 20-year average of 25.7 (and 85.6% overvalued versus its 1870-2020 average reading). It is worth remembering that while overly high (or overly low) valuations in and of themselves are rarely a trigger for

initiating major asset price moves, they nevertheless can be a valuable barometer of prevailing investor euphoria or despondency.

4. Narrow, Highly-Concentrated Equity Market Leadership: Benefiting from widespread investor admiration and appreciation of the fact that lockdown measures and the stay-at-home economy have accelerated the adoption of networking, communications, and online shopping, a major part of the 2020 gains in major stock market indices has been attributable to the surging share prices of just a handful of large technology companies (Facebook, Alphabet, Amazon, Apple, and Microsoft) which together represent 25% of the total equity market capitalization of the S&P 500 index. Year-to-date through the close of trading on August 21st, Amazon was up +77.8%, Apple had gained +69.4%, and Microsoft had risen +35.1%; without these three companies, the total YTD return through July 31 (including dividends) from owning the S&P 500 index would have been -4.1%, whereas with Amazon, Apple, and Microsoft included, the total return from owning the S&P 500 index would have been +2.4%.

5. Broadening Indications of Investor Exuberance: Often useful as a cautionary signal to manage or reduce portfolio risk, a number of commonplace late-cycle investment behaviors have recently begun to manifest themselves, including:

i. Securities trading apps, message boards, social media outlets, and Internet sites have attracted daytraders into the equities and options markets to a degree not seen since the height of the 1999-2000 dotcom investing boom;

ii. Special Purpose Acquisition Companies (“SPACs”) raise equity funds in Initial Public Offerings (“IPOs”) from the capital markets with no specified details as to the use of the proceeds; they tend to be popular in ebullient market environments. Such eras may feature a wide spread between first-quartile and third-quartile managers’ prior track records, operating skill, and respect of shareholders’ interests;

iii. High-priced stocks suddenly vaulting further upward upon the announcement of a stock split may reflect irrational investor ardor, since it is deemed more likely that mainstream investors may be attracted to such shares at their new lower prices; and

iv. With zero commission rates on stock trades, the suspension of sports betting, a homebound, digitally-savvy and electronic games-experienced generation has embraced fractional investing, allowing the purchase of partial shares “by the slice,” which may be transforming some significant portion of neophyte investors into day-trading speculators.

6. Risks of Further Deterioration in U.S.-China Relations: The course of 2020 thus far has witnessed a widening ideological divide, visa bans, mutual sanctions on senior officials, forced consulate closures, and hawkish policies on the part of the U.S. and Chinese governments over trade, technology, Hong Kong, and superpower rivalry (in the South China Sea, in the Taiwan Strait, in the Middle East, in cyberspace, and in orbit). These issues have set off a significant downgrading of the two nations’ relations that is increasingly characterized by recriminations, acrimony, and the risk of more serious confrontations. Even as U.S. and Chinese trade negotiators plan to confer by video in late August over: (i) progress in fulfilling terms of the “Phase One” trade deal; and (ii) U.S. actions against Chinese technology firms, the charged state of overall relations between America and China argues for allocations to high-quality assets with value-holding power, as well as some appropriate degree of liquidity that can be put to work should asset prices come under pressure owing to more elevated bilateral antagonism.

7. Pre- and Post-Election Uncertainty: With increased mail-in balloting amidst pandemic fears, the potential for foreign interference in the electoral process, and legal resources already being marshaled in the event of disputed election outcomes, financial asset prices could experience significant volatility in the time leading up to and after the U.S. national elections on Tuesday, November 3rd. Voting results for the White House, the Senate, and the House of Representatives could have important implications for corporate and individual taxes, federal spending priorities, the conduct of policymaking, regulatory activity, geopolitical positioning, and not least, stock, bond, and currency prices.

PORTFOLIO POSITIONING

1. Themes to Consider Over the Next Few Years: Expressed below are a number of potential themes that may be taken into consideration in selecting asset categories, asset managers, asset classes, sectors, companies, and security types:

i. The rising aspirations and spending power of the massively expanding global middle class, especially in Asia;

ii. “All-weather” sectors and companies that can thrive regardless of uncertain and shifting social, public health, and political trends and conditions;

iii. Taking advantage of (rather than being taken advantage of by) the likelihood of money printing, internal and external currency debasement, and ‘Modern Monetary Theory’ being pursued by the Authorities to service massive explicit government and corporate indebtedness and the enormous implicit obligations of pension and healthcare promises;

iv. Companies and sectors with demonstrated successful track records in: capital allocation; balance sheet strength; risk management; sustainably defendable business models; and robust multi-year return on equity (generated through revenue growth and favorable margin preservation, rather than through excessive leverage) meaningfully above the firm’s weighted average cost of capital; and

v. Technology enablers and dominators in artificial intelligence, machine learning, 5G cellular network technology, the Internet of Things, biotechnology, battery and energy inventions, robotics, quantum computing, and electric vehicles.

2. Keeping Things in Perspective: Many of the overarching themes and conditions that influence our intermediate- and long-term asset allocation and investment strategy emphasize the need to recognize that the concepts and implementation methods intended to achieve safety, balance, diversification, and liquidity are likely to face meaningfully evolving social priorities, geopolitical power relationships, price level changes, demographic trends, indebtedness levels, technological pervasiveness, and not least, the definition, role, embodiment, and value of money itself. For the current environment and conditions expected in the period ahead, we have set forth some thoughts in the following sections.

3. Enhancing and Preserving: We admit to some continuing degree of unease over the apparent disconnect between, on the one hand, the growing mainstream popularity of stocks during the rapid recovery in U.S. equity prices, and on the other hand, the continued uncertain economic and post-election outlook. Our short-term inclination at this point in time is to take note of the Federal Reserve’s ongoing support of financial asset prices while taking advantage of such strength to upgrade the quality of portfolio holdings —(i) jettisoning lower-quality, higher-risk assets; (ii) selectively carrying some cash-like liquidity; and (iii) with timing restraint and price discipline, adding to attractively-priced, higher quality assets on equity market pullbacks.

4. Equity Emphasis and De-emphasis: Particularly in the current conditions of very low U.S. Treasury interest rates, it appears likely that cash generating, financially-stable companies with robust growth prospects, which are able to operate and thrive in the digital sphere as they continue to enhance their business models, should retain a valuation premium. Within equities one may consider: (i) judiciously beginning to shift some emphasis from growth sectors, companies, and managers towards the moderate inclusion of some value sectors, companies, and managers; (ii) modestly adding small- and mid-cap companies (or investment managers specializing and with good track records in this space) to our primary emphasis on large-capitalization enterprises; and (iii) for the time being, continuing to prefer a tactical overweighting to U.S. domestic equities over international developed and emerging market stocks.

5. Focus on Strength and Quality: One may consider to emphasize asset managers, sectors, and specific companies that can benefit from the major sustained trends of the 2020 decade, including: (i) incremental growth in a wide range of economic circumstances; (ii) a focus on economic repair, digitalization, ecommerce, personal wellness, safety, domesticity, home improvement, infrastructure spending, and where possible, the release of pent-up consumer demand; and (iii) advantageous capture of benefits from onshoring, supply chain redesign, and deglobalization as important drivers of capital spending and disruptive innovation. At the company level in equities, we reiterate our emphasis in point #1 above on identifying and building long-term exposure to firms possessing fortress-like, cash-rich balance sheets, limited debt, positive free cash flow generation, dividend strength, and competitive business models that over a long time frame can generate high returns on equity (through revenue growth and tenable profit margins, rather than through excessive levels of leverage).

6. Balancing Growth and Value Sectors: On a year-to-date basis through Thursday, August 20th, the iShares Russell 1000 Growth ETF (symbol IWF, and including companies in sectors such as technology, healthcare, and communication services) had returned +15.58%, while the iShares Russell 1000 Value ETF (symbol IWD, and including companies in sectors such as financial, real estate, energy, utility, and industrial companies) had returned -15.83%; this 31.41 percentage point Growth minus Value returns differential has widened by a further 2.53 percentage points from mid-July’s already historically wide divergence over more than three decades, and to us appears to argue for considering some piecemeal, prudent reallocation from selected Growth sectors, companies, and managers into selected Value sectors, companies, and managers.

7. U.S. Dollar Outlook: After declining -7.4% In 2017, appreciating +4.3% in 2018, and marginally slipping -0.2% in 2019, the DXY U.S. dollar index (measured versus a basket of six major currencies — the euro, Japanese yen, Swedish kroner, British pound, Canadian dollar, and Swiss franc) had as of the market close on August 21st, declined -3.3% year-to-date. Following the U.S. dollar’s strength in 1Q20 as a safe-haven,

“flight-to-quality” asset during the pandemic- and lockdown-induced global financial market turbulence earlier this year (the DXY index had gained +6.7% year to date as of March 20th), we believe the U.S. dollar may continue on its gradual path of weakness as, due primarily to the Federal Reserve’s stated preference for lower yields in the United States, the U.S. dollar’s income-generating advantage is likely to be considerably vitiated versus other major currencies.

8. Fixed Income Securities: We affirm our affinity for issuers at the high-quality end of the rating spectrum, both in investment grade and in high-yield bonds. In taxable and tax-exempt bonds (where we see some pockets of value on a taxable equivalent basis), we prefer maturities and durations along the short-to-intermediate portion of the yield curve spectrum.

9. Alternative Investments and Real Assets: In alternative investments, our focus for some time has emphasized: some degree of exposure to gold and/or gold mining shares/ETFs, and we continue this preference; high-quality master limited partnerships with strong business models and sustainable dividend-paying capacity; and select investments in private credit, private real estate, and opportunistic strategies that are positioned to selectively derive meaningful value from the numerous dislocations created by the coronavirus pandemic.

THE PATH OF THE 2020 ELECTIONS

For a good part of this calendar year, we have counseled that we consider it prudent to give advance thought to the range of potential economic, regulatory, taxation, spending, budget deficit, societal, and financial market implications of the national election results, depending on whether Republicans or Democrats win one or more of the White House, the House of Representatives, and the Senate.

After Labor Day, the campaign, especially as the election approaches, is likely to reflect increased amounts of political vociferousness, perhaps some degree of vehemence, and even apportionments of vitriol (we hope and pray not too much) with the potential to cause meaningful shifts in financial asset prices. That is why we recommend forming beforehand and sticking to a well-reasoned asset allocation plan and investment strategy tailored to the investor’s own circumstances, time horizon, objectives, and temperament.

November 2016: The 58th Quadrennial Presidential Election

The Outcome: On Tuesday, November 8th, 2016, a total of 138 million Americans (58.1% of the nation’s voting-eligible population; 100 million voting-eligible Americans did not cast a ballot) voted in the 58th quadrennial presidential election. With 270 electoral votes needed to win the White House (since the early 1800s, more than 900 constitutional amendments have been introduced in Congress to alter or abolish the electoral college, all of which have failed thus far), the Donald John Trump/Michael Richard Pence ticket (carrying 30 states, 2,626 counties, and garnering 62.984 million votes, 46.1% of the total votes cast) collected 304 electoral votes and the Hillary Rodham Clinton/Timothy Michael Kaine ticket (carrying 20 states, plus the District of Columbia, 487 counties, and garnering 65.853 million votes) collected 227 electoral votes, as 7 “faithless electors” (2 pledged to Donald Trump, and 5 pledged to Hillary Clinton) instead voted for other candidates. On Inauguration Day, January 20th, 2017, Donald Trump took office as America’s 45th President and Mike Pence took office as its 48th Vice President.

The County-by-County Count: The 2016 election represents the fifth presidential contest in which the winning candidate won the electoral college but lost the popular tally, in this case by 2.869 million votes. And whereas some social media-based sources have pegged (what they deem to be) the total number of 3,141 nationwide counties’ results at 3,084 for Donald Trump to 57 for Hillary Clinton, it is worth keeping in mind that vote tallies by county differ depending on the standards used. For example, the Associated Press considers parishes in Louisiana as counties in election results, the State of Alaska has 40 state districts grouped into 20 “boroughs,” and the Commonwealth of Virginia includes 95 counties and 38 independent cities. The Associated Press, assessing what it considers to be 3,113 counties, reports the 2016 outcome to have been 2,626 counties for Donald Trump to 487 counties for Hillary Clinton, and Time magazine, analyzing the totals for its definition of 3,152 counties, reports 2,649 counties to have been won by Donald Trump and 503 counties to have been won by Hillary Clinton.

November 2020: The 59th Quadrennial Presidential Election

September, October, and Then, the Election: With the VIX volatility index having risen an average of four points ahead of each of the last seven presidential elections since this measure was created, important issues to consider in the weeks ahead include:

i. The post-conventions Clarity of Message by each political party as delivered to, perceived by, and ability to energize their respective loyal voter bases;

ii. The nation’s reactions to the three presidential debates and one vice presidential debate (all to last 90 minutes with no commercial breaks, to begin at 9:00 PM Eastern time, and with moderators to be announced) – Tuesday, September 29, at Case Western University in Cleveland, Ohio; Wednesday, October 7 (between Vice President Pence and Senator Harris), at the University of Utah in Salt Lake City, Utah; Thursday, October 15, at the Adrienne Arsht Center for the Performing Arts in Miami, Florida; and Thursday, October 22, at Belmont University in Nashville, Tennessee;

iii. Assessments of the strength of party identification among various segments of the voting population, as well as in the composition of the overall electorate, at the same time, taking into account the ability of each ticket to generate serious backing from less-supportive voter populations;

iv. Which candidate voters (considering demographic attributes, where they live, how they classify themselves on the political spectrum, and other characteristics) think can better confront America’s broad challenges, including the coronavirus pandemic, the economy, social issues, and pressing global concerns;

v. The effectiveness of voting procedures, trust in mail-in balloting, the degree of putative social media and foreign-based election interference, actual voter participation, and the perceived veracity and legitimacy of the results; and

vi. The potential consequences of prolonged uncertainty associated with a contested election (should it occur) for social order and the financial markets.

Some Implications of Potential Scenarios

Fully 20% of the pre-pandemic workforce is currently receiving jobless benefits, and early expectations of a V-shaped recovery have been hindered by renewed coronavirus outbreaks. Regardless of who wins the 2020 election and in what manner, financial asset valuations appear to be reflecting expectations that whenever the coronavirus pandemic ends, some degree of economic acceleration is likely to take place in the U.S.

As we have counseled for some time, it is important to devote thought and attention to the taxation, regulatory, economic, asset allocation, and investment strategy implications of the three leading potential electoral outcomes outlined below (while noting that both political parties have expressed interest in promoting the development of generic drugs, lowering drug prices, and containing healthcare costs; and the two parties have also been focusing on antitrust, platform liability, and privacy issues relating to many of America’s biggest technology enterprises):

i. If President Trump is re-elected and wins the White House, Democrats keep control of the House of Representatives, and Republicans keep control of the Senate, such an outcome would likely favor securities in the following sectors: technology, defense, finance, healthcare, and energy, while potentially putting pressure on sectors and companies that could be harmed by further deterioration in U.S-China relations;

ii. if Vice President Biden wins the White House, Democrats keep control of the House of Representatives, and Republicans keep control of the Senate, such an outcome would likely favor companies and sectors that would be deemed to have thereby avoided increased taxes and a heavier regulatory burden;

iii. If Vice President Biden wins the White House, Democrats keep control of the House of Representatives, and Democrats take control of the Senate (sometimes referred to in the media as a “blue wave”), such results would substantially raise the odds of higher taxes. Offsets to the latter outcome could come in the form of substantial additional spending on infrastructure, education, and healthcare. Securities in the following sectors, among others, are perceived to be disadvantaged by a “blue wave” Democratic sweep: defense, healthcare, financials (via increased regulation) and energy (with expectations of restricting fracking and limiting drilling on federal lands in Texas/New Mexico’s Delaware Basin and Southeast Montana/Northeast Wyoming’s Powder River Basin), while giving a lift to sectors and companies that could be helped by improving U.S-China relations.

The 2016 Pre- and Post-Election Tax and Spending Outlook

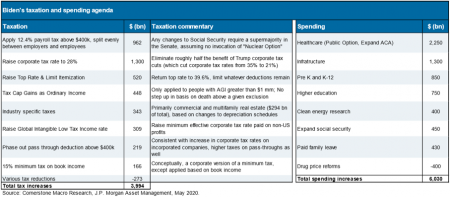

As shown in the panel below, the current taxation and spending policy positions of Vice President Biden contain numerous base-broadening elements that increase taxes by approximately $4 trillion, while increasing spending to the tune of approximately $6 trillion in areas including healthcare, infrastructure, education, energy research, and other initiatives.

Released on Wednesday, July 9th, the 110-page report of the Unity Task Force (created and staffed by individuals designated by Vice President Joe Biden and Senator Bernie Sanders) contains a detailed set of policy recommendations in six domestic policy areas:

i. Health care (while not supporting Medicare for All, the report proposes a public option, a government-administered plan “like Medicare” that would be available to all Americans; on drug pricing, the report recommends appointing a government board to set prices that Medicare would pay for new drugs);

ii. The economy (with $400 billion pledged for procurement of domestically made goods and $300 billion to support high-tech research);

iii. Climate change (here, a total of $2.0 trillion over four years is earmarked to shift millions of jobs into clean energy, with the goal of cutting emissions from power generation to zero by 2030, having net zero emissions by 2050, and introducing new fuel-economy standards);

iv. Criminal justice (proposing reforms to law enforcement and policing practices);

v. Education (including universal preschool for three- and four-year-olds, at a cost of $775 billion over a decade), and

vi. Immigration (proposing to end travel restrictions against 13 countries, and to maintain protections from deportation for approximately 700,000 young immigrants known as “Dreamers”).

Should Vice President Biden win the White House, financial asset prices in general, as well as specific industries and companies, are likely to be affected by the speed and degree to which the new Administration and Congress (whose degree of support depends on which party controls the House of Representatives and which party controls the Senate) might be able to implement priorities in these and other areas.

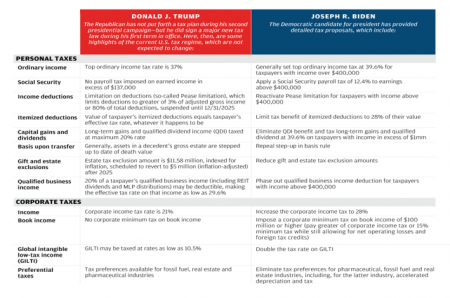

For further granularity, the following panel sets forth eight elements of personal taxes and four elements of corporate taxes: (i) under the current U.S. tax regime, which would not currently be expected to change much under President Trump (although the President has endorsed the idea of payroll tax reductions; tweeted about a potential capital gains cut; and vowed to extend the Tax Cuts and Jobs Act of 2017, which capped the so-called SALT (State and Local Tax) deduction at $10,000); and (ii) as currently outlined as taxation policy under a Biden administration.

Given that the process of turning taxation proposals into law takes time, it is likely to be at least June 2021 for new tax legislation to be enacted. On several aspects of tax planning (including the timing and forms of income and expenditures; tax gain-loss harvesting; and retirement, estate, and gifting strategies) it may be sensible to postpone any major moves until a judicious assessment can be made of the makeup of the post-election government and its specifically-expressed legislative agenda.

DISCLOSURES

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This report is a publication of Aaron Wealth Advisors LLC. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication, are subject to change, and may not be the opinion of Aaron Wealth Advisors.

*Information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional adviser should be consulted before implementing any of the strategies or options presented.

*Information is not an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*All investment strategies have the potential for profit or loss. The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.