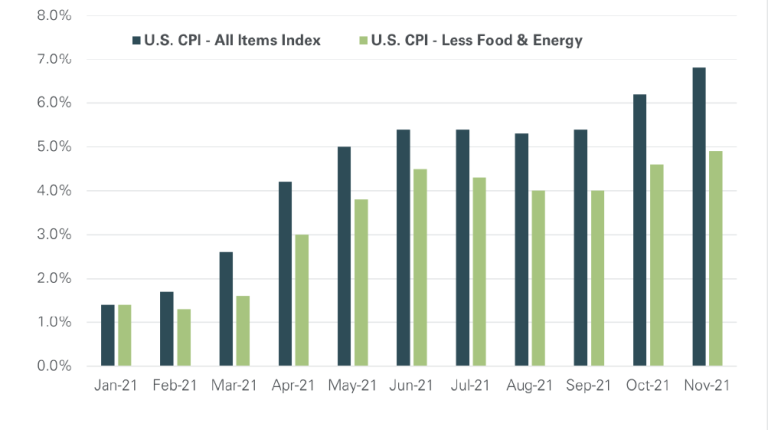

On December 10th, the U.S. Bureau of Labor Statistics released its monthly Consumer Price Index (CPI) report for November. For most, the data quantified the day-to-day financial changes they had been experiencing for months now. The all-items CPI index jumped 6.8% over the previous 12 months, the largest increase since June 1982.¹ Interestingly, markets responded positively with the S&P 500 closing up nearly 1% that day,² likely because the number was in-line, rather than above, expectations. The Federal Reserve’s preferred gauge of inflation, the CPI Index excluding the often-volatile categories of food and energy, rose 4.9% over the same period. We have now experienced an 8-month surge of increasing inflation from 4.2% in April to November’s reading of 6.8%.¹

The frequently touted fallacy that price increases would be transitory – based on the argument that supply chain distortions would naturally resolve themselves as the global economy emerged from the pandemic and year-over-year inflation readings would soon end their measurement against the depressed levels of the 2020 recession – never held up to even casual scrutiny. Finally realizing the absurdity of the claim, Jerome Powell officially ditched the “transitory” tag from the Fed’s language and outlook regarding inflation during Congressional testimony at the end of November. After its December meeting, the Fed also announced that it would hasten its tapering of asset purchases – known as quantitative easing – and penciled in a potential for three rate increases in 2022 (previously, policy rate increases weren’t expected until 2023). While this is a step in the right direction, it may be too little too late to contain the problem without inflicting material economic harm. Moreover, monetary policy is only one component in the morass of government functions which contribute to the overall success or failure of economic management.

Perhaps the most frustrating aspect of this reality, as investors and individuals, is the lack of recourse available to quickly right the ship when mismanagement becomes so readily apparent and pervasive. Evidence of inflationary pressures have been mounting for some time now and warning signs pointing to the increasing risk were glaringly obvious to almost anyone paying attention. To wit, we have consistently sounded the alarm – along with a multitude of others possessing far greater public prominence – about the growing probability of runaway inflation since the late summer of 2020. Yet, instead of pivoting when their prior assumptions proved inaccurate, those tasked with managing and crafting public policy routinely exacerbate conditions by implementing counterproductive or ineffectual programs that further stoke the inflationary flames. But more on that later…

Part I: How We Got Here

First, some background and context are required to better understand the current landscape. In lieu of a lengthy recitation of technical minutiae, the four main drivers of inflation in an economy can be summarized as follows:

i. an increase in the money supply

ii. a decrease in the demand for money

iii. a reduction in the aggregate supply of goods/services due to higher production costs (e.g., raw materials, wages, tariffs, taxes, and

other inputs)

iv. an excess in aggregate demand from consumers, businesses, government, or foreign buyers

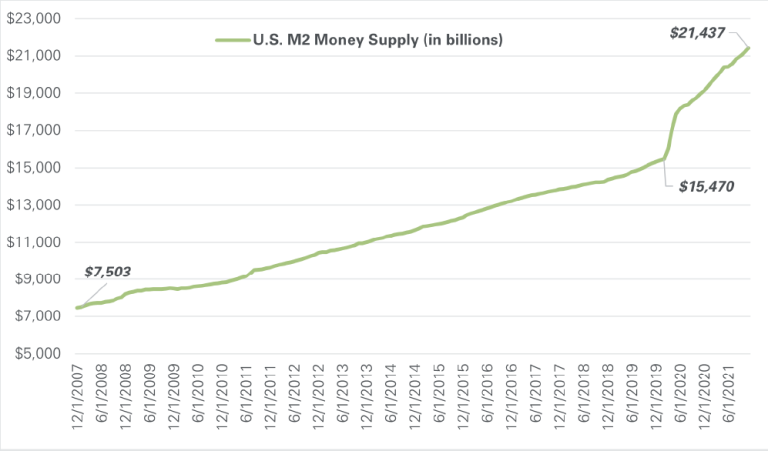

It would be inaccurate to assume that the genesis of today’s inflationary pressures can be attributed solely to the fiscal and monetary policy responses of the Covid pandemic. While they certainly doused the fire with an unwarranted accelerant, the dry kindling and embers have been building to a blaze since the Great Recession of 2008-2009, without appropriate concern. It was then that central banks around the world began the unprecedented and coordinated implementation of a non-traditional policy – quantitative easing. Through mass purchases of long-term securities on the open market and zero (or negative) policy rates, the goal of this program was to flood the economy with liquidity, spur the demand for risky assets, encourage lending, and suppress interest rates. Originally intended to be a robust, short-lived stimulus program that would jumpstart the economy after a devastating recession, it continued with no end in sight as the ensuing recovery was characterized by years of tepid growth and low inflation. As a result, U.S. money supply has increased 184% since 2008, with a 37% flood coming since the beginning of the global pandemic alone.4 For an understanding of the magnitude of the Fed’s asset purchases, its balance sheet has skyrocketed to $8.8 trillion, or roughly 38% of U.S. GDP, from $922 billion at the end of 2007 and $4.2 trillion in February 2020.5 We mentioned in the opening section that the Fed’s December decision – to taper asset purchases more quickly and schedule three rate hikes in 2022 – was a step in the right direction. However, even with these changes, monetary policy is still massively expansionary. With the U.S 10 Year Treasury rate hovering around 1.5% and inflation running at 6.8%, real rates (i.e., nominal rates adjusted for inflation) are currently -5.3%. What then is the justification for extending quantitative easing through March 2022? The answer eludes us, but we suspect some degree of cognitive dissonance might be at play here.

Concurrently, albeit with some exceptions, fiscal policy has added to the malaise with mounting regulatory burdens, higher taxes, escalating protectionist trade barriers (e.g., quotas and tariffs), and growing centralized control over large swaths of the private market by government. On this front, the most egregious errors of judgement – but likely better described as political opportunism – have come during the Covid response.

To highlight a few of the most baffling decisions:

i. March 2021 Covid Relief package: Despite the $4 trillion of relief already allocated, a burgeoning economic recovery that began in the summer of 2020, rapidly declining rates of unemployment, a soaring stock market, and state/local governments flush with budgetary surpluses from high tax revenues and federal outlays, the newly installed administration thought an additional $1.9 trillion of fiscal stimulus was sorely needed in early 2021. Roughly one-third of the package was allocated for direct cash payments to individuals and state/local governments, disbursed indiscriminately without the appropriate means-testing to determine actual need. Even more perplexing, trumpeted as legislation critical to stimulating a rebound in the economy and labor market, it implemented enhanced unemployment benefits along with the expansion of other cash benefits that created significant disincentives to work – at a time when labor force participation was sagging and businesses struggled to fill open jobs, despite surging demand. Certain segments of the labor force often earned a higher income from government payments than from employment. As job openings consistently outnumbered unemployed workers, businesses have reported record levels of jobs that are unable to be filled and high percentages of positions with zero or few qualified applicants.6 To attract workers, companies have increased compensation and even gone so far as offering financial incentives just to interview. We do not want to imply that this policy was the sole driver of recent inflation. However, given the incentives it created, one could draw the reasonable conclusion that it had a meaningful impact via contributions to wage hikes, worker shortages, reduced production capacity of supply, and excess consumer demand.

ii. Management of the Energy Sector: From its first days, the Biden administration has waged a full-fledged attack on the domestic energy sector. Their intent is clear and unapologetic: stifle the industry’s growth, or bankrupt it altogether, in order to achieve the climate goals outlined in the party’s “Green New Deal.” Sweeping executive orders and intense political pressure for broad divestment from fossil fuels have cudgeled business with crippling regulatory burdens and mounting operational costs. Immediately after taking office, President Biden paused all oil and gas leasing on federal lands. Shortly after, he killed the previously approved Keystone XL pipeline, along with the thousands of U.S. jobs it would provide. Following this in May, the administration approved the Nord Stream 2 pipeline – which will deliver gas from Russia to Europe – handing Vladimir Putin a massive financial and energy victory. Even as consumers began to feel the pain of soaring gasoline, heating, and electricity prices this year, no consideration was given to rethinking this strategy. Instead, he went hat in hand to OPEC, pleading for them to boost production (which they didn’t) – as if there wasn’t a domestic solution readily available to curb the inflation spiral. By choosing not to leverage America’s abundant, low-cost energy resources, this approach has needlessly increased domestic prices, forced a return to reliance on foreign competitors for U.S. energy needs, and shipped jobs and economic returns overseas that could have been retained here. All of this stands in direct opposition to the “Buy American” priorities that Biden routinely boasts and makes no progress whatsoever towards his climate goals.

iii. Lumber Tariffs: In May, Biden’s Commerce Department issued a preliminary proposal to more than double the tariffs on Canadian softwood lumber imported to the U.S. After further administrative review the new policy was finalized in November, ultimately increasing average softwood lumber tariffs to 17.9% from 8.99%. As reported by the Wall Street Journal, “Softwoods like spruce and pine are the backbone of light construction, and a steady supply is key to restraining the rising cost of home building. For decades U.S. sawmills haven’t been able to meet domestic demand, but they’ve leaned on government to protect their market share…According to Working Forest, a trade publication, U.S. production has topped out at some 70% of domestic demand since the 1990s. Foreign producers fill the gap, led by Canada with a roughly 26% share.”7 Back in a 2019 edition of our I.D.E.A. Series (Tariffs: What They Are, What They Aren’t, and Who Pays8), we outlined in detail how tariffs are antithetical to economic growth, both domestically and globally. In short, they act as an added tax on consumers by creating a “net welfare loss” of higher prices and reduced domestic supply. By October, the month prior to the Commerce department’s final decision, U.S. indexes for Softwood Lumber Producer Prices and House Prices had already increased 28% and 26%, respectively, over February 2020 levels.9 Thus, this decision was perplexing for multiple reasons. First, tariffs could lead to higher costs and reduced supply in a market where U.S production capacity is chronically incapable of fulfilling domestic demand. And, secondly, it contradicts the administration’s purported objectives of alleviating inflationary pressures and normalizing relationships with global trading partners. Under President Biden’s direction, we expected the U.S. would tilt away from the destructive protectionist instincts that were characteristic of the Trump

administration, but so far this assumption has been proven wrong. Our evaluations of this administration’s policies should not be interpreted, in any way, as a commentary on President Biden’s motivations. That is to say, we believe their intentions are coming from a good place. Running a country is an impossibly difficult job, especially during a global pandemic and these hyper-partisan times. Instead, our goal is to highlight differences in approach and a potential better path forward. Inflation is the most regressive tax that exists. And because of its disproportionate impact on the most financially disadvantaged and vulnerable of our society, there should be no delay in relieving this burden. We believe that the Biden administration would share this goal though we disagree on the best way to achieve it, which reasonable people in a democratic society often do.

Part 2: Solutions – Ones That Can Work; Others That Definitely Will Not Duke University professor of political science and economics, Michael Munger, recently described prices as “signals wrapped in incentives.”10 It follows then that price increases reflecting a scarcity of goods, services, and labor might be eased by incentivizing the growth of supply. On the other hand, policies which goose excess demand further or create greater disincentives to growing supply would have the opposite effect, that is to spur inflation. Alas, the latter approach has been consistently applied throughout much of 2021 as too much focus has been placed on generating more demand. Is it any wonder then that we have seen price levels jump nearly 7% recently with no sign of subsiding? As we alluded to earlier in this section, our proposed solution is simple: “It’s the supply side, stupid.” A policy mix of deregulation, lower taxes, and pared back government entitlements/benefits could address the inflation problem by incentivizing and eliminating barriers to supply growth, essentially allowing it to catch up to aggregate demand. While this may seem antithetical to the sensibilities of today’s Democratic party, any short-term political backlash would likely lead to far greater confidence in the president’s ability to manage the economy – which, according to recent polls, is quite underwater. At the same time, if successful, this strategy may aide him in wresting back control of the party from his more progressive flank in order to pursue the moderate agenda on which he campaigned. Furthermore, it has the added benefit of not forcing policymakers to suppress demand. Demand side interventions – such as large, swift interest rate hikes and significant fiscal policy tightening –should be viewed as a last resort to curbing lingering inflation given their historical propensity to cause recessions (like in the 1970’s). Though, obviously, a prudent and measured reduction in stimulative monetary policies is necessary. To be sure, other mechanisms recently proposed –government price control boards, corporate investigations, increased supply chain regulations – will not only be ineffective, but likely harmful to the economy.

Conclusion

We have learned time and again throughout history that governments cannot wish away inflation through the ham-fisted regulation of its symptoms. Rather, the underlying structural issues must be attenuated. While we will continue advocating for such an approach, as investors we must still prepare for the scenario that no such resolution will come about. Thus, out of prudence and realism, we will remain active and vigilant in protecting client portfolios from the potential negative impacts of further inflation.

Sources

¹U.S. Department of Labor, Bureau of Labor Statistics 12/10/2021: https://www.bls.gov/news.release/pdf/cpi.pdf

²Investing.com data for 12/10/2021: https://www.investing.com/indices/us-spx-500-historical-data

³Board of Governors of the Federal Reserve System (US), Households and Nonprofit Organizations; Net Worth, Level, Federal Reserve Bank of St. Louis; https://

fred.stlouisfed.org/series/TNWBSHNO. U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items in U.S. City Average [CPIAUCSL],

Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/CPIAUCSL, Index Dec 1972 = 100 (1972 Dollars)

4Board of Governors of the Federal Reserve System (US), M2 [M2SL], Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/M2SL, Data period 12/2007

to 10/2021.

5Board of Governors of the Federal Reserve System (US), Total Assets of the Federal Reserve, https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm,

Data period 12/31/2007 to 12/27/2021. U.S. Bureau of Economic Analysis, Gross Domestic Product [GDP], Federal Reserve Bank of St. Louis; https://fred.stlouisfed.

org/series/GDP, Data as of Q3 2021.

6National Federation of Independent Business (NFIB) Research Foundation, Small Business Optimism Index, November 2021 Report, https://www.nfib.com/surveys/

small-business-economic-trends/

7Wall Street Journal 11/30/2021 print edition, Editorial Board, “Biden Joins the Lumber Tariff Wars”, https://www.wsj.com/articles/biden-joins-the-lumber-warscommerce-

department-tariffs-canada-11638226400

8Aaron Wealth Advisors, May 2019, I.D.E.A. Series, “Tariffs: What They Are, What They Aren’t, and Who Pays”, https://aaronwealth.com/tariffs-what-they-are-what-theyarent-

and-who-pays/

9Source: YCharts, Data period February 2020 to October 2021; US Bureau of Labor Statistics, US Producer Price Index: Lumber and Wood Products: Softwood; US

Federal Housing Finance Agency, FHFA House Price Index.

10Wall Street Journal 12/15/2021 print edition, Michael Munger, “A Biden Plan for Prices? No Thanks.” https://www.wsj.com/articles/no-biden-price-plan-wagestagnation-

inflation-money-supply-price-regulation-control-federal-reserve-11639517901?mod=opinion_lead_pos5

Disclosures

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts

business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of

the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a

fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific

course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The

information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this

material reflect Aaron Wealth’s views as of the date(s) indicated on the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific

investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or

indirectly, will be profitable or equal to past performance levels.

*This document contains forward looking statements, including observations about markets and industry and regulatory trends as of the original date of this

document. Forward looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the

negatives of these terms, and similar express results could differ materially from those in the forward looking statements as a result of factors beyond our control.

Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward looking or

other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of

loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional

regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth

Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the

information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without

warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of

securities offered for sale or private placement offerings available to any investor.