As the daily life of the modern-day person becomes ever busier and spare time becomes a luxury of increasingly greater value, it’s only human nature that complacency can creep into areas that don’t demand one’s day-to-day attention. Our bandwidth for focus is constrained and limited, unfortunately. So, it is not unusual that important topics – like our financial well-being – often get put on the back burner for another day, especially when a relationship with a financial advisor exists. After all, this is what they are paid to do – to manage assets on behalf of their clients who may not have the time or confidence to do so on their own.

Despite this, in order to give oneself the best chance of success in reaching financial goals, it is vitally important for every investor to be aware of several pitfalls to which all portfolios are susceptible. Armed with the right information and targeted questions, anyone can become their own best advocate in charting the course of their financial future. This is akin to the better health outcomes experienced by patients who manage their exercise, diet, and regular doctor visits based on the critical knowledge of family medical history and diseases for which they are at higher risk due to genetic predisposition. At Aaron Wealth, we firmly believe obtaining an independent opinion on your portfolio can be a helpful and illuminating exercise. However, there is no substitute for understanding the implications of the below investment considerations and the value this knowledge can provide to your financial life.

1) Understanding Investment Fees & Building Cost-Efficient Portfolios

One of the most controllable – but often most overlooked – areas of wealth management is fees, which includes fees for services and fees for investment products. Improving a portfolio’s cost-efficiency, all else being equal, can be the easiest way to have a materially positive impact on financial outcomes. Put simply, fees are the only portion of future investment returns that are known in advance. It should go without saying then that a clear understanding of the amount of fees you are currently paying, the services or products for which you are paying fees, to whom you are paying fees, and the competitive market rate for each is of paramount importance. In order to facilitate an accurate view of how you are being charged and the amount of fees you are paying, we should consider some basic definitions:

“It should go without saying then that a clear understanding of the amount of fees you are currently paying, the services or products for which you are paying fees, to whom you are paying fees, and the competitive market rate for each is of paramount importance”

Advisory Fees: This fee is charged by financial advisors for their advice and services, typically based on the amount of assets under management and periodically assessed. If your wealth manager acts in a fiduciary capacity, this should be the primary avenue by which he or she is compensated from the relationship. However, if your advisor is held to the less-stringent suitability standard, this is not likely to be their only revenue stream.

Management Fees: This fee is associated with the investment products you buy and sell. A mutual fund or ETF will charge a percentage-based fee, often called an expense ratio, to cover the costs and various expenses associated with managing the fund. You will never see these fees show up on your statements. Instead, they are deducted from the Net Asset Value (or share price) of your fund shares, essentially reducing your return by an equivalent amount. This is the reason many investors can often overlook this cost and be sold expensive, underperforming products. As such, determining whether a product “earns its fee” is a critical component of evaluating the cost-efficiency of a portfolio. Similarly, one should always ask their advisor if he or she: (1) is financially incentivized to place clients in certain products, or (2) receives payouts – often called revenue sharing – from the fund company for selling a particular product

Commissions and Transaction Fees: Commissions are fees incurred when an advisor sells an investment product and earns a commission based on the value of your initial investment. Such products can include ETFs, mutual funds, stocks, bonds, annuities, and structured notes, sometimes carrying large commissions ranging from 1-4%. It is worthwhile to note that advisors who act as fiduciaries almost never charge these fees because of the inherent conflict of interest. If they do, they are required to disclose this to you prior to any trade.

2) Is Your Advisor Considering Your Total Financial Picture or Just an Isolated Silo?

Let’s assume a middle-aged man shows up to an emergency room with nausea and severe pain in his chest and arm. The doctor then prescribes him Tums for the nausea and extra-strength Tylenol for the pain. Obviously, this man is presenting with all the tell-tale signs of a heart attack. But the doctor’s treatment of his symptoms in isolation would inevitably lead to some tragic results. While investment management decisions don’t deal in life or death decisions like a heart attack, the analogy remains an illustrative one. Viewing just a portion of one’s financial life in isolation, rather than in context of the total picture, may lead to a concentration of unintended risks and negative outcomes that are avoidable. For this reason, any wealth advisor should consider your entire financial profile and not just a siloed view of the assets they manage. Incorporating and considering things like real estate holdings, private equity, employment situation, life insurance, and any other outside investments you may have allows for the execution of a more holistic, cohesive, and well-defined strategy. At Aaron Wealth, we work with our clients to build out comprehensive net worth statements so you can clearly understand your entire financial profile. By leveraging our technology partners, we are able to provide consolidated reporting on private investments, real estate holdings, outside investments, and other specialty assets – that are often omitted due to complexity or lack of robust capabilities – in a comprehensive manner. This gives both advisor and client a common, universal resource for the totality of their financial life from which to plan and strategize.

Viewing just a portion of one’s financial life in insolation, rather than in context of the total picture, may lead to a concentration of unintended risks and negative outcomes that are avoidable

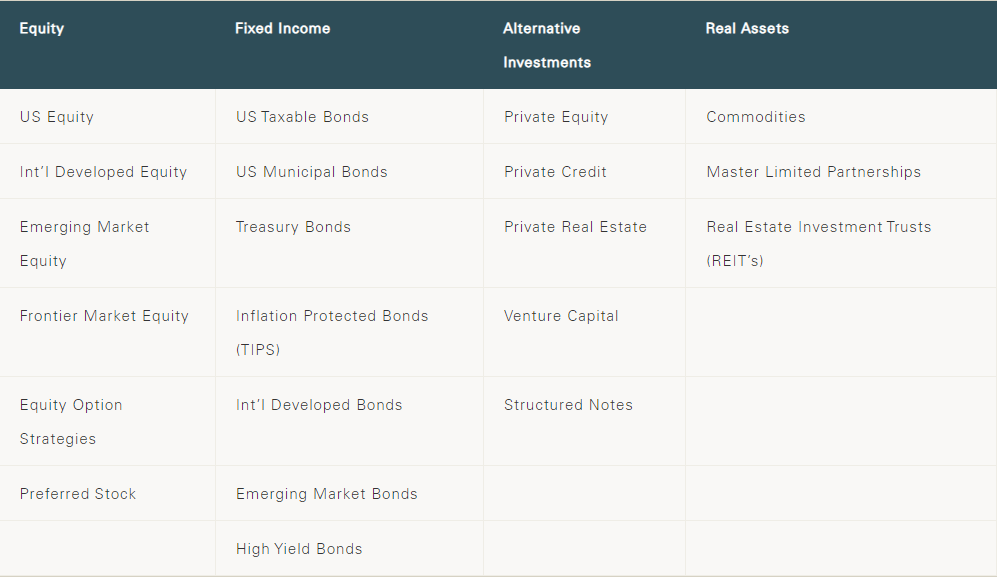

3) Does Your Asset Allocation Fit Your Goals, Objectives, and Risk Tolerance?

Building a customized, strategic asset allocation that is designed to meet the goals and objectives of your portfolio is a fundamental pillar of successful wealth management. A strategic asset allocation is the long-term mix of assets that is expected to meet the investor’s objectives. Ensuring that this allocation is consistent with both your ability and willingness to take risk is of equal importance. An investor’s willingness to take risk is often determined by the psychological makeup of the individual and their overall attitude towards risk. In contrast, an investor’s ability to take risk is a quantitative measurement based on their financial situation. Taking too little or too much risk can result in falling short of your goals or adding undue anxiety to your life; it is a delicate balancing act that requires discussion, education, and personal evaluation. A well-designed allocation diversifies your portfolio across several distinct asset classes with the goal of efficiently generating a sufficient long-term return while assuming the minimal amount of risk required. Some asset classes that should be considered for investors include:

We often find investors have limited exposure to several of the above asset classes. Unfortunately, not all advisors possess the acumen required to implement more sophisticated strategies that can be quite beneficial in creating a diversified portfolio. As we have discussed in a previous paper, evidence shows that remaining invested in a well-diversified portfolio over the long term, rather than trying to time the market, has proven to be a superior strategy.

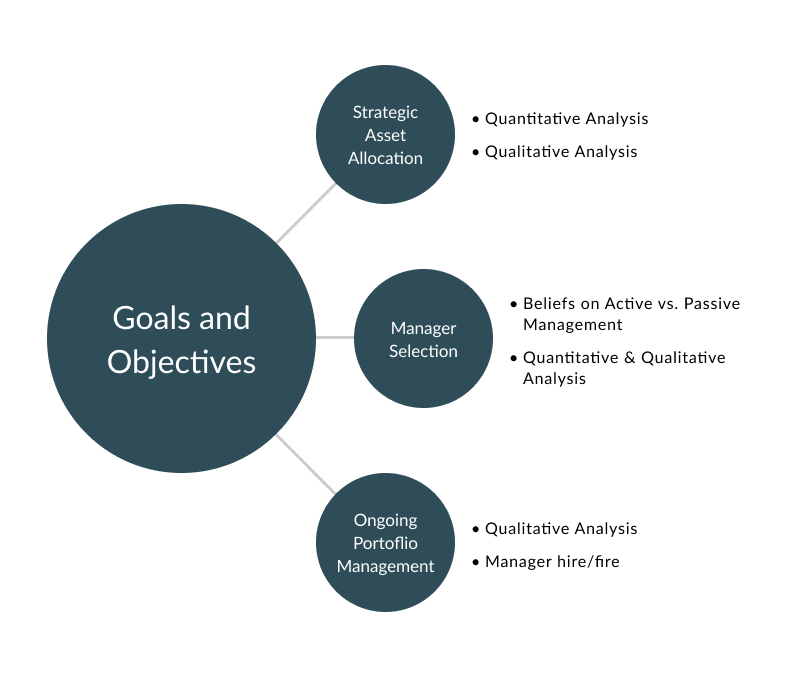

4) Is Your Portfolio Properly Constructed?

Designing the correct mix of asset classes within your portfolio is just one step on the road to success. The process of portfolio construction is how a sound strategy gets implemented into real world action. This process begins with selecting the types of investment vehicles that will maximize the potential for achieving your long-term goals and objectives. After your investment advisor has conducted thorough due diligence on the universe of products, he or she will help you select the optimal investments. One of the most fundamental decisions an investment advisor makes is the choice between an active vs. passive strategy. Active investing takes a hands-on approach that involves hiring an outside manager to conduct research and select the investments that he or she believes will outperform the market. The fundamental goal of active management is to “beat the market” or outperform a stated benchmark. In contrast, passive investing is the process of selecting a benchmark in which to invest and replicating the performance. Because active investing is generally more expensive, it has been shown that many active managers fail to outperform their benchmarks, especially accounting for taxes and fees. At Aaron Wealth, we believe that many equity markets tend to be better suited for passive management, whereas certain fixed income markets are better for an active approach. However, there is no one-size fits all strategy, and each portfolio should be tailored and fully customized to your specific situation.

Another vital consideration is the decision to invest in growth vs. value style disciplines. A value approach will invest in companies that are perceived to be underpriced based on research. In contrast, growth style investing will buy companies that the manager believes will outperform the broad market based upon future earnings potential. A strategy that incorporates both disciplines is prudent from a diversification perspective. However, history has shown that growth style investing has the potential to perform better when interest rates are low and the economy is performing well. Alternatively, value tends to outperform when the economy is weak and there is a “flight to safety” among investors. Once the portfolio has been implemented based upon these decisions, ongoing monitoring of the investments is paramount to successfully achieving your goals.

5) Evaluating Investment Performance and Tax Implications

Performance evaluation is a crucial component of the investment process and serves as a key feedback step. By regularly evaluating the portfolio, investors can identify the strengths and weaknesses of the various investment strategies and take the opportunity to make any necessary changes. However, it is essential to monitor your investment performance with accurate measures. We commonly find individuals who aren’t properly gauging their portfolio performance with the right statistics and benchmarks. It is vital to choose an appropriate benchmark in order to appraise the investment performance of your portfolio, with accurate and interrelated characteristics. Frequently this is accomplished by creating a custom benchmark. For example, it is helpful to combine several different world indices and asset classes in order to accurately match the characteristics of your customized portfolio

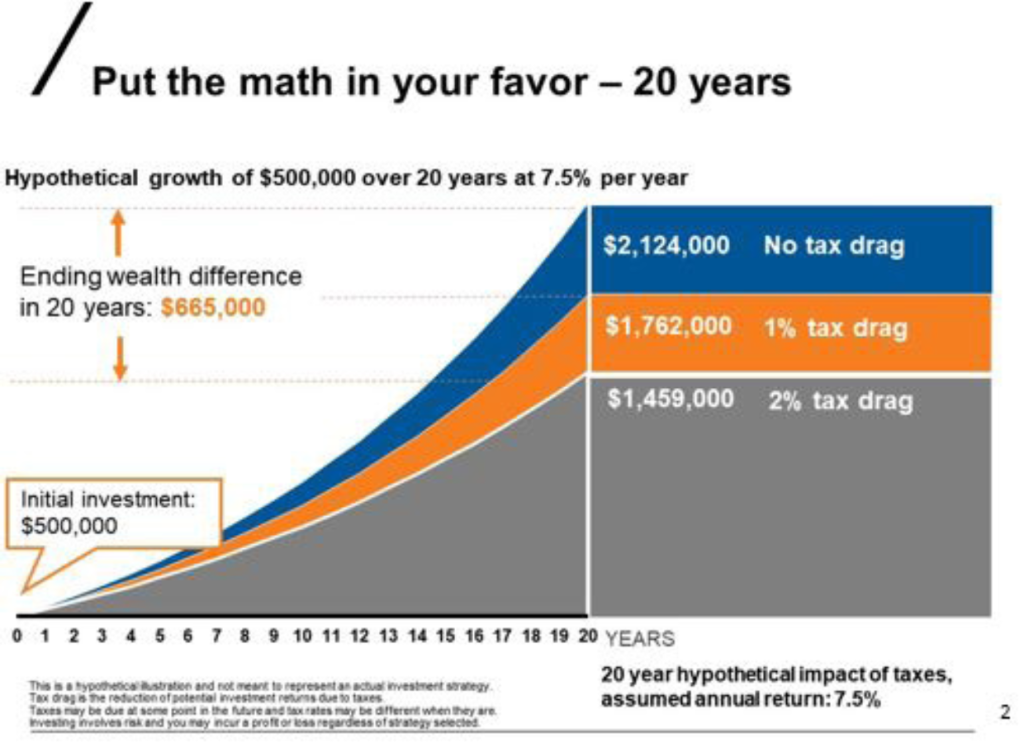

Another overlooked aspect of investor portfolios is the lack of focus placed on pre-tax and post-tax return. A critical term to understand is tax drag, which is the loss in return due to tax obligations. As you can see from the chart below, just a 2% tax drag has the potential to drastically reduce wealth creation over a 20-year time horizon.

There are certain investment strategies that can help reduce the tax implications of your investments. Among them include tax-loss harvesting, tax-managed accounts, and utilizing investment vehicles that are more tax-efficient. One clear example is the avoidance of mutual funds that typically pay large capital gain distributions. As an alternative, Exchange Traded Funds (ETF’s) do not pay any capital gains until the position is sold. Working with the correct advisor will allow you to carefully consider the effects of taxes on your investments and address them accordingly.

Conclusion

Overall, we believe there are several key factors that should be considered when reviewing your investment portfolio. Working with the correct advisor can help you unlock potential within your portfolio if these considerations are addressed in the proper manner. At Aaron Wealth, we encourage investors to seek an independent consultation as it can be an efficient way to identify and remedy avoidable pitfalls that hinder a portfolio’s long-term success.

DISCLOSURES

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated on the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward looking statements as a result of factors beyond our control. Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.