After years of binging on fiscal and monetary excess, markets feel the pain of withdrawals

INTRODUCTION: THE MAKING OF A MONETARY JUNKIE

Back in 2008 the Federal Reserve, along with many major central banks across the world, embarked on an unprecedented and coordinated response to the Great Recession. With standard techniques – such as slashing interest rates to zero – proving ineffective, they argued that a more unconventional monetary policy was required to jumpstart the global economy. Their idea: central banks should buy predetermined amounts of securities (e.g., Treasuries, corporate bonds, mortgage-backed securities) to inject capital into the economy and hold down longer- term rates thereby incentivizing appetites for risk assets and spurring economic activity. In November of 2008, the first round of quantitative easing (QE1) began in the United States. Given its novelty, this program was generally understood to be a short-term policy of last resort reserved for only the greatest of financial crises. Yet, in 2010, the Fed continued with a second round, nicknamed QE2. And in 2012, a third round was launched with an important modification – it would be open-ended, earning the moniker “QE-Infinity.” When Covid-19 shutdown the world in 2020, a turbocharged version of quantitative easing was rolled out. As a result of such sustained monetary policy accommodation, and in combination with historic bouts of fiscal stimulus, global markets have been able to binge on a glut of liquidity, cheap money, and federal backstops for nearly 15 years. Is it possible that we’ve become addicted?

At the beginning, there was ample discussion and concern about how this type of program could be unwound. QE, by design, creates massive distortions in price signals across markets, hence the original intention to be a short-lived, emergency program. With each round of larger and larger stimulus, the potential fallout from withdrawing this support increasingly faded from the conversation. We got a glimpse into our future in the summer of 2013 when the Fed announced it would begin tapering asset purchases. However, this was by no means a turn to monetary tightening. Interest rates would be held steady, but asset purchases would be reduced each month (still historically accommodative by any measure). What followed has come to be known as the “Taper Tantrum” – equities plummeted 4% in the three trading sessions following the announcement and bond yields spiked. Following this, the Fed quickly decided to hold off on scaling back its asset purchases in September.

Such an event reminds one of an important lesson: swiftly cutting off the supply of an addictive substance can be quite dangerous.

WHERE WE ARE NOW: SUFFERING THE EFFECTS OF BINGING & THE PAIN OF WITHDRAWALS

After a punishing first four months of the year, investors experienced some reprieve in May from the battering volatility as most major equity and fixed income indices stabilized to post a positive return for the month. However, the respite was short-lived, proving itself only to be the eye of the storm. Thus far in June, markets continued their downward slide – across asset classes – and increased in intensity. To illustrate the market dynamics at play, imagine a balloon. As stimulus flooded the economy and rates fell, the balloon inflated more and more (valuations expanded, momentum was strongly positive). Then this year, as policy began to tighten and rates jumped, the balloon started to deflate – the more quickly rates spike, the more quickly the balloon deflates (valuations compressed, momentum swung strongly negative). In addition to the withdrawal of stimulus, the current landscape has been broadsided by exogenous shocks and deteriorating economic conditions, including:

Inflation Data: The May reading of S. CPI (released in mid-June) showed no indication that inflation was moderating, coming in at 8.6%.1 This has now become a major concern across the globe. For the same month, Eurozone inflation reached a record-high, hitting 8.1%.2

Energy, Commodities, & Russia’s War in Ukraine: U.S Retail Gas Prices soared to all-time highs averaging $5.10/gallon in June.3 Russia declined a humanitarian-relief proposal for safe shipping routes of crucial commodity supplies through Ukraine. Moscow also cut off the majority of natural gas flows to Europe through the Nordstream Pipeline, raising concerns about insufficient heating for this winter and sending market prices about eight times higher than seasonal averages.4

Monetary Policy: Contrary to previous guidance, the Federal Reserve hiked its policy rate 0.75% at its June meeting and left open the potential for the same in July. Concurrently, central banks across the world began to accelerate or signal tighter-than- expected monetary policies to combat inflation.

Profit Warnings by Businesses: some companies, especially in the retail sector, issued warnings for earnings guidance as they reported needing to “right-size” large accumulations of inventory.

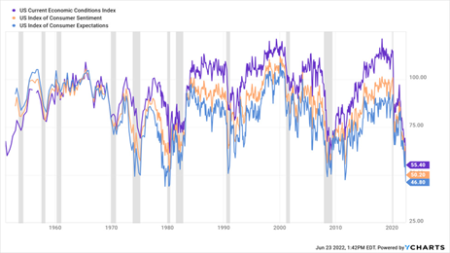

While lagging U.S. economic and employment data remain strong, forward-looking indicators have begun to show how pervasive and pessimistic the collective outlook has become. Indices of U.S. Surveys for Current Economic Conditions, Consumer Sentiment, and Consumer Expectations all recently plummeted to record or near-record lows (see Figure 1 nearby). In a marked reversal from the first quarter, the majority of CEO’s surveyed over the past month now believe the U.S. economy will be in a recession in the next 12-18 months. Typically, in similar periods of heightened volatility, broad-based selloffs, and market gloom, we would be chomping at the bit to deploy long-term capital and scoop up assets at attractive discounts. However, as will be discussed in more detail in the next section, today’s environment has a small, albeit material, probability for negative snowballing, with downside risks accumulating as conditions worsen.

Figure 1: US Consumer Survey Indices (Inception – June 2022; gray shading denotes recession)5

WHERE WE GO FROM HERE: RECESSION APPEARS UNAVOIDABLE

We find no solace in the fact that markets, central banks, and policymakers are finally waking up to the reality of today’s inflation problem that we, and others, have been warning about since late 2020. In fact, their tardiness further exacerbates our concerns that those currently responsible for setting policy are ill-equipped to competently navigate through this period of instability. The June Fed meeting and Chairman Powell’s subsequent conference demonstrated that monetary policy is and may remain behind the curve to tame inflation. On the fiscal policy front, we do not believe that any of the proposed solutions recently posited by Congress or the current administration will alleviate the inflation problem. Furthermore, some of these proposals that increase stimulus (prepaid gas cards, student loan forgiveness, etc.) and supply-side disincentives (price controls, increased corporate/personal income tax, heightened regulations, etc.) may actually exacerbate price increases. Monetary policy can only intervene via the demand side of the economy, which means to tame inflation it must dampen aggregate demand. Since we see no realistic scenario on the horizon where fiscal policy steps in to address the imbalance on the supply side (i.e., through reduced tax/regulatory burdens, incentives for energy production and business investment), we anticipate that higher inflation will persist longer and rates will increase further than currently anticipated by markets – despite some cushion between today’s current Fed Funds rate and the short end of yield curves. As such, absent some positive exogenous shock, our base case is that the U.S. and global economy will be in a recession in the next 12 months, with the next 3-6 months proving critical to the duration and severity of any slowdown.

At this point, it is important to remember that economic data is backward-looking while markets are forward-looking. To that end, should inflation be quelled without crushing demand, then any ensuing recession would likely be mild, and the worst of the market pain could potentially be behind us. To clarify, our base case scenario is in no way an advocation for the elimination of certain asset classes, like fixed income. We remain long-term investors and manage portfolios accordingly. However, we are quickly working through various new strategy options to protect against what could be a relatively tumultuous 12-24 months, in addition to what has already been implemented. A few, but certainly not an exhaustive list, of the potential arrows in our quiver for downside risk mitigation include:

Tactical Tilt Towards High-Quality and Value: High-quality, attractively valued companies with wide moats and stable and consistent cash flows have historically outperformed in recessionary environments. This would accomplish a two-pronged objective of tilting towards an outperforming style while simultaneously reducing exposure to (what should be) an underperforming style – growth. Growth equities, which have a greater share of earnings expected in the future, are relatively harder hit in a rising rate environment as future cash flows are discounted to be less valuable.

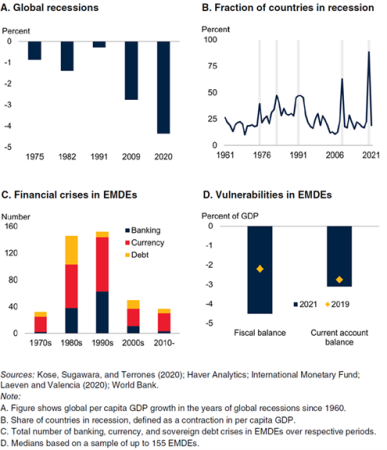

Tactical Underweight to Emerging Markets: Emerging Markets, while highly idiosyncratic, have historically struggled during risk-off and monetary tightening cycles. Developing economies with high levels of indebtedness relative to GDP and/or large shares of foreign currency denominated debt frequently experience the greatest amount of pain. This was evident during the Great Inflation period of the late- 1970’s to early-1980’s, which saw a slew of financial and currency crises arise in Emerging Market (EMDE) economies following the global recession triggered by policy tightening to fight inflation in Advanced Market (AM) economies. As EMDE currencies depreciate relative to AM currencies, AM interest rates rise, and/or AM economies enter recession, EMDE foreign currency denominated debt becomes increasingly expensive to service and AM capital flees to perceived safe haven assets. As a result, EMDE economies frequently spiral into crises (see Figure 2 nearby).

Shift Towards Short-Term, Quality Corporate Credit: Since late 2020, we have been diligently focused on reducing our exposure to interest rate risk within the fixed income sleeve. One solution to this was increasing allocations to securitized sectors of the fixed income universe. With this came greater exposure to the health of S. consumers via credit card debt, auto loans, residential mortgages, etc. In a recession, downside risk could be mitigated and relative performance enhanced by shifting towards short-term, high quality corporate debt and credit.

Intelligently Designed Structured Notes: We have recently designed various structured notes for analysis that possess attractive asymmetric risk-return profiles and For instance, with a high degree of principal protection, we could earn higher-than-market yields relative to fixed income while further reducing interest rate risk and retaining levered-upside equity participation should markets rebound over the next several years.

Figure 2: End of Stagflation of the 1970s & Vulnerabilities in EMDEs6

These decisions have become our top due diligence priority as implementation-timing is critical to successful outcomes. We will communicate these changes to each client, as pertinent and appropriate. Our intent with this communication is not to sow fear or concern. Rather, we believe our clients deserve timely and transparent insight into our outlook, the reasoning that underpins it, and the steps we are taking to address the potential risks we see on the horizon. In addition, all investors should be clear-eyed in their expectations when prevailing circumstances signal choppy waters ahead. As always, please feel free to reach out to our team with any questions, comments, or concerns.

Sources

1.YCharts; U.S. Bureau of Labor Statistics; Consumer Price Index Report for May 2022; https://www.bls.gov/news.release/cpi.nr0.htm

2.Eurostat; Euro Area Inflation for May 2022; https://ec.europa.eu/eurostat/documents/2995521/14644605/2-17062022-AP-EN.pdf/1491c8b5-35e4-cdec-b02a- 101a14a912ad

3.YCharts; U.S. Energy Information Administration; Weekly Retail Gasoline and On-Highway Diesel Prices Report for June 13th, 2022

4.Bloomberg online edition; European Gas Extends Gains as Specter of Russian Cuts Persists by Anna Shiryaevskaya; June 21, 2022; https://www.bloomberg.com/ news/articles/2022-06-21/european-gas-rises-again-as-supply-crisis-spreads-across-region

5.YCharts; University of Michigan; University of Michigan Surveys of Consumers Report for June 2022

6.World Bank. 2022. Global Economic Prospects, June 2022. Washington, DC: World Bank. doi: 10.1596/978-1-4648-1843-1. License: Creative Commons Attribution CC BY 3.0 IGO

Disclosures

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances or any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors. The information contained in this presentation represents factual information, analysis, and/or opinions regarding various investments. Any opinions expressed in this material reflect Aaron Wealth’s views as of the date(s) indicated on the Presentation and are subject to change.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*This document contains forward looking statements, including observations about markets and industry and regulatory trends as of the original date of this document. Forward looking statements may be identified by, among other things, the use of words such as ”expects,” “anticipates,” “believes,” or “estimates,” or the negatives of these terms, and similar express results could differ materially from those in the forward looking statements as a result of factors beyond our control.

Recipients of the information herein are cautioned not to place undue reliance on such statements. No party has an obligation to update any of the forward looking or other statements in this document.

*All investment strategies have the potential for profit or loss. The investment strategies illustrated in this document and listed above involve risk, including the risk of loss of principal.

*The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.