Spoiler Alert: You pay, so brace yourself for what amounts to a tax increase on business, economic activity, trade efficiencies, and consumption passed by executive fiat.

With headlines constantly dominated by news of ongoing trade wars and expanding tariffs, let’s dive head-first into a detailed evaluation of the subject. We have discussed our stringent aversion to such costly and unnecessary market manipulation at length in the View from Here series; however, a firm understanding of the history, mechanics, and impacts of tariffs will help to further contextualize the foundational underpinnings of our arguments.

Tariffs are often employed by populist leaders as an economic weapon that can be brandished against trading partners to reignite domestic growth and revive national industrial glory. However, the major implication of this failed trading policy that proponents either do not comprehend or refuse to admit: the pain inflicted by their great weapon is inevitably borne by the very populations they claim to champion. To be clear, the accelerating trend towards a liberalized, open global economy – that leverages mutually beneficial agreements and removes expensive trade barriers like tariffs – may be the single largest driver of wealth creation in the modern era. In short, tariffs are antithetical to economic growth, both domestically and globally.

A Brief Word on I.D.E.A.: Insights, Discussion, Education, and Analysis Series

As this is the inaugural edition of the I.D.E.A. series, we wanted to share with clients its intended goal and design. Our firm was founded on the belief that our clients should be as well informed as we are, if they so desire. There is no “black box” here. For this reason, we have built a strong investment culture that we wish to share with our clients through thought leadership papers and educational opportunities. We are in the business of wealth management – your wealth, that is – and it is incumbent upon us to provide you with the tools required to understanding your financial life.

At the same time, we believe that one of the biggest disservices foisted upon individual investors by the financial industry is the exploitation of asymmetrical knowledge gaps used to portray competence and justify value. In other words, the industry’s consistent use of technical jargon coupled with a failure to educate has led to an informational power imbalance between insiders and the clients who rely on them for advice. Some may abuse this imbalance to erect a façade of sophistication and foster an environment in which the client feels overly dependent on the advisor. In our opinion, this practice does not connote any real value or translate into expertise – it merely breeds distrust of the advisory relationship, in particular, and broader industry, in general.

We have sought to employ plain language when discussing economic and market concepts in our thought leadership series, The View from Here. However, even though plain language is used, our goal of making these pieces easily digestible can sometimes lead to a lack of explanatory detail that may be needed to connect the underlying interrelationships between concepts and conclusions. Essentially, in order to keep these pieces succinct and concise, we often omit a level of minutiae that – while helpful in understanding broader mechanisms – generally distorts the ability of readers to logically follow our thought process. This is where the I.D.E.A. series comes in to play. It is an open forum for more detailed Insights, Discussion, Education, and Analysis on a wide array of topics. This can range from filling in the informational gaps of a specific concept discussed in The View from Here series, to presenting analysis and opinions on current events, to writing about a client-directed area of interest.

As always, we welcome your input. If there is ever a topic or idea which you would like to learn about in more depth, we would happily include it in this series. After all, this is designed specifically with our clients’ interests in mind.

Understanding Tariffs and Their Effects on Markets

Let’s begin our discussion with a brief overview of what tariffs are and why they are implemented. Investopedia provides a helpful and succinct description:

A tariff is a tax imposed by one country on the goods and services imported from another country. Tariffs are used to restrict imports by increasing the price of goods and services purchased from another country, making them less attractive to domestic consumers. There are two types of tariffs: a specific tariff is levied as a fixed fee based on the type of item, such as a $1,000 on a car [or] an ad-valorem tariff is levied based on the item’s value, such as 10% of the value of a vehicle. Governments may impose tariffs to raise revenue or to protect domestic industries – especially nascent ones – from foreign competition. By making foreign-produced goods more expensive, tariffs can make domestically produced alternatives seem more attractive.

Tariffs – along with other trading practices such as import quotas – are most often associated with mercantilism. Mercantilism is an economic theory grounded in the idea that trade is a zero-sum game, if one country wins another must lose. For this reason, mercantilists believe government should heavily regulate trade and commercial activity to maximize profitable trading. Tariffs and quotas are a couple of regulatory tools governments will use as a means to this end. According to this system, maximizing wealth means maximizing exports and minimizing imports. Despite being largely debunked by modern economic theory, many policy makers continue to hold views similar to mercantilism. As an example, the current White House administration frequently cites U.S. trade deficits as evidence of detrimental trading relationships and to support the imposition of tariffs. However, such inaccurate notions are not consistent with economic reality and obfuscate the real costs imposed by trade barriers. What’s more, proponents of these trading policies often perpetuate the misconception that these taxes are paid by international trading partners and not domestic businesses and consumers

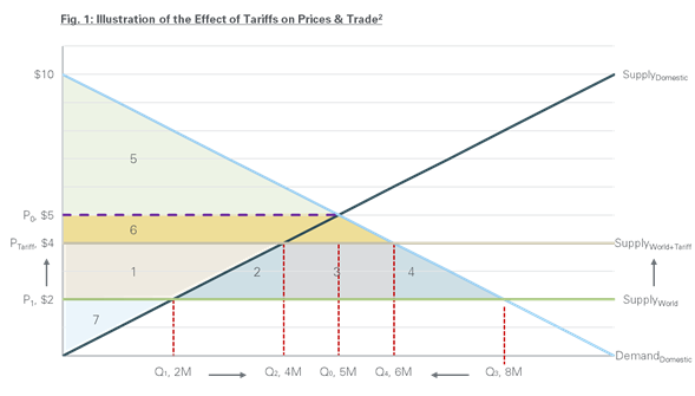

To truly understand the negative impacts of tariffs, it is imperative that one conceptualizes the ripple effects that spread across markets when artificial trade barriers are erected. For illustrative purposes, we will walk through a straightforward Supply & Demand model to demonstrate the primary effects in the market of a single good (see Figure 1).

The dark blue and light blue diagonal lines in Figure 1 represent the Supply and Demand curves, respectively, for a specific good in the domestic economy. The light green horizontal line represents the global Supply curve for the same good. Now, let’s evaluate what happens in varying circumstances.

Scenario 1: The Domestic Market is Completely Closed

A closed market means that no international trading of this good takes place with the domestic market. Thus, the market clearing price is the intersection of domestic supply (SupplyDomestic) and domestic demand (DemandDomestic). This represents the price at which the quantity supplied equals the quantity demanded. As a result, in this scenario:

- The price paid by consumers would be $5 (P0)

- The quantity supplied by producers would be 5 Million (Q0)

- The consumer surplus – defined as the amount a consumer is willing to pay relative to the price actually paid for a good – is a measure of benefit to the consumer. In this scenario, it is represented by the area of the shaded green box (5), which is equivalent to $12.5 Million.

- The producer surplus – defined as the price at which a producer is willing to sell a good relative to the price they actually receive – is a measure of benefit to producers. In this scenario, it is the mirror image of the shaded green box (5) and equivalent to $12.5 Million.

Scenario 2: The Domestic Market is Completely Open

A completely open market means that international trade is frictionless; there are no barriers or costs to trading. Thus, the market clearing price is the intersection of world supply (SupplyWorld)and domestic demand (DemandDomestic). This represents the price at which the global quantity supplied equals the domestic quantity demanded. As a result, in this scenario:

- The price paid by domestic consumers would be $2 (P)

- The total quantity supplied would be 8 Million (Q3): 6 Million (Q3– Q1) will be imported from international producers and 2 Million (Q1) will be produced domestically

- With free trade, consumers benefit greatly. The consumer surplus, now measured by boxes 5+6+1+2+3+4, equals $32 Million. A gain of $19.5 Million

- Domestic producers, however, will lose due to their lack of competitiveness. The producer surplus, now measured by box 7, is $2 Million, a loss of $10.5 Million.

- Although imports now dominate domestic production, the market is more efficient because prices are lower. The net gain in market efficiency is equivalent to the change in consumer surplus minus the change in producer surplus, $19.5 Million – $10.5 Million, or $9 Million.

Scenario 3: The Domestic Market is Open, but a $2 Tariff is Imposed on Imports

As mentioned earlier, tariffs artificially increase the price of foreign goods. This $2 tax is paid by importers and then passed on to the end consumer. Thus, the market clearing price is the intersection of world supply (SupplyWorld+Tariff) and domestic demand (DemandDomestic) plus the $2 tariff. As a result, in this scenario:

- The price paid by domestic consumers would be $4 (PTariff)

- The total quantity supplied would be 6 Million (Q4): 2 Million (Q4 – Q2) will be imported from international producers and 4 Million (Q2) will be produced domestically

- With tariffs, domestic consumers are worse off. They pay an artificially higher price relative to free trade. The consumer surplus, now measured by boxes 5+6, equals $18 Million. A loss of $14 Million.

- Domestic producers benefit relative to free trade due to protective barriers from more efficient international competition. The producer surplus, now measured by boxes 7+1, is $8 Million, a gain of $6 Million.

- Although domestic producers have experienced a gain in market share and prices, the overall domestic market is less efficient and more costly. The net effect relative to free trade, measured by the gain in producer surplus plus the loss in consumer surplus, is $6M – $14M = a net loss of -$8 Million

Evaluation: Measuring the Effects of Tariffs

With these scenarios now laid out, we can evaluate the net loss of the $2 Tariff. Boxes 2, 3, and 4 represent that net loss from the implementation of a tariff. This sum demonstrates the negative effects consumers experience through higher prices and less domestic supply. Boxes 2 and 4 are known as the “net welfare loss” to the market, while Box 3 represents the tariff revenue generated for the government. This straightforward example illustrates a hierarchy of trade: while international trading with tariffs is better than a completely closed economy, free and open trading produces greater welfare for all. We want to emphasize that this analysis only portrays the primary (or micro) implications for the market of a single good. What is often missed or not understood are the secondary and tertiary effects that can ripple through the economy because of tariffs. To show these real world, knock-on impacts, we turn to an historical example.

Case Study: The Bush Steel Tariffs of 2002-2003

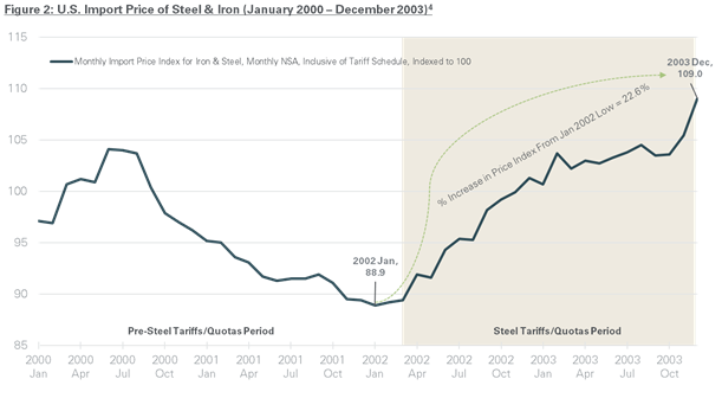

Under what is known as Safeguard Measures, members of the World Trade Organization are granted the power to temporarily restrict the import of a certain product if the domestic industry is impaired, injured, or threatened by increased imports. The Bush Administration imposed tariffs on a range of steel products using such safeguard measures in March of 2002. Tariffs ranged from 8% – 30% on international steel imports, though some countries were exempt (Canada, Mexico, among others). While the tariffs were intended to last for about three years, political pressure ultimately forced them to be lifted in December of 2003.

We do not intend to go into an in-depth analysis of what transpired, but simply provide an overview of the secondary and tertiary ripple effects caused by tariffs. The benefit of this particular case is its isolation to one industry over a relatively short period of time. Many studies have been performed that isolate the effects of U.S. steel tariffs which are easily obtainable. For the purposes of this piece however, data shown is for illustrative use only and may not isolate the impact of steel tariffs versus other external market forces.

For context, it is useful to include a brief summary on the topic from a study conducted by Trade Partnership Worldwide – an international trade and economic consulting firm. In their February 2003 study, “The Unintended Consequences of U.S. Steel Import Tariffs: A Quantification of the Impact During 2002”3, the authors state:

As a result of a Section 201 (“safeguard”) investigation brought at the behest of the U.S. steel industry, President Bush in March 2002 imposed tariffs on imports of certain steel products for three years and one day. The tariffs, combined with other challenges present in the marketplace at the time and in the months that followed, boosted steel costs to the detriment of American companies that use steel to produce goods in the United States. The resulting negative impact included job losses for thousands of American workers.

Their analysis only pertains to the first year (2002) of the tariffs and does not include 2003. Yet, results of other studies and the data to follow are largely consistent.

Since 1992, the Bureau of Labor Statistics have tracked data on U.S. import prices for steel that incorporate the effects of varying steel tariffs. In January of 2002, three months before the Bush steel tariffs took effect, the index measuring these prices hit an all-time low since 1992. After the tariffs were implemented, the price index increased 22.6% from this low (see Figure 2). This measures the primary market effect, described in the section above. Prices rise when artificial barriers, like tariffs, are imposed on trade.

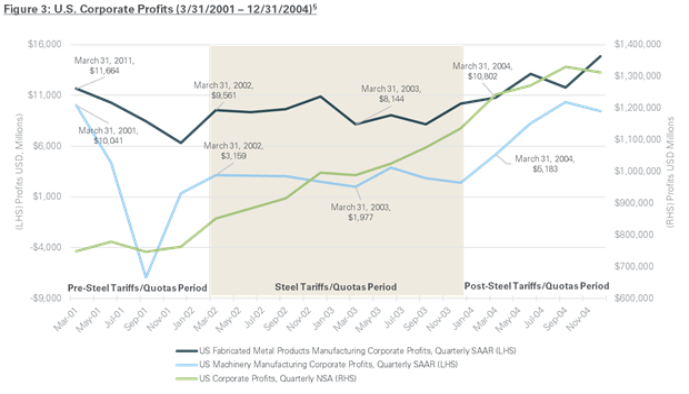

Steel and steel-intensive manufactured products are commodities. For this reason, companies that produce such goods are “price-takers” – meaning prices for their goods are dictated by consumer preferences. This is in contrast to “price-makers” who can more easily dictate prices as producers because of the value, scarcity, or brand recognition of their products (think Apple’s iPhones). When input prices for commoditized goods – like steel in soda can manufacturing – increase, it can be more difficult for “price-takers” to pass on those costs to end buyers. This was true for the steel tariffs of 2002-2003. The profits of steel-intensive manufacturers were significantly negatively impacted relative to the periods pre- and post-tariffs, even as U.S. corporate profits in general were growing strongly (see Figure 3). This represents a secondary effect: because of the increased price of steel due to tariffs, manufacturers of metal and steel products saw a sharp decrease in profits as they couldn’t pass on higher costs to consumers.

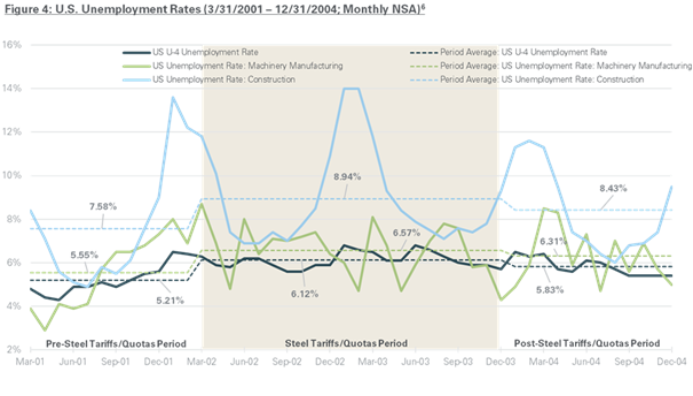

Moving one step forward in the logical chain, as profits are compressed and begin to deteriorate, companies are forced to reduce hiring or layoff existing employees. This is magnified in commoditized industries where profit margins are already slim and production costs are much more sensitive to the prices of inputs. During the Bush steel tariffs, this effect was evident as the unemployment rate for machinery manufacturing and construction – both steel-intensive industries – spiked more than the U.S. Unemployment Rate during the tariff period (see Figure 4). This represents a teritiary impact.

From this historical example, one begins to notice just how detrimental tariffs can be to a single industry. Steel tariffs, over less than a two-year period, increased the import price of steel by approximately 22%, ate into the profits of steel-intensive manufacturers, and reduced employment in related sectors as well. How these tariffs effected the broader economic, market, and employment landscape is much more difficult to isolate. What we can say, is that the protection of one particular (often politically influential) industry through tariffs comes at the cost of consumers, workers, and industries that do not receive this favorable treatment. In the end, the rest of the economy pays in higher prices, lost jobs, and lower productivity so that a globally-uncompetitive domestic industry can stave off either an eventual demise or a much-needed strategic pivot.

Why This Matters Now?

Traditionally, the U.S. Constitution grants Congress alone the power to regulate international trade, impose tariffs, and enact trade agreements. In line with its “Power of the Purse”, the Legislative Branch was bestowed the great authority to draft policy regarding commerce, trade, and taxation through the legislative process. However, over the past several decades, Congress has consistently ceded this authority to the Executive Branch.

- Section 232 of the Trade Expansion Act of 1962 grants the President the ability to regulate trade for national security reasons.

- Section 301 of the Trade Act of 1974 allows the Executive Branch to take any appropriate action, including retaliation, in response to a practice or policy of a foreign country that the President believes unfairly effects U.S. commerce or violates international trading agreements.

- The International Emergency Economic Powers Act of 1977 grants the President broad latitude to regulate trade, commerce, and financial activity with respect to foreign countries during national emergencies.

- Trade Promotion Authority (TPA) allows the Executive Branch to negotiate international trade agreements that promote free trade. Under certain circumstances, such negotiated agreements that require changes to U.S. law can be expedited through Congress using particular procedures.7

We acknowledge that, at the time they were enacted, these policies were well-intentioned. The spirit of the laws is grounded in protecting national security interests, efficiently negotiating trade deals with other countries, and promoting free trade. However, because the language of the laws is quite vague and broad, they can be easily abused to achieve the political objectives of unscrupulous actors.

This is no more apparent than the tariffs the Trump administration threatened to impose on Mexico if they did not do more to stop illegal immigration at the southern U.S. border. Trump invoked the International Emergency Economic Powers Act (IEEPA). After declaring a state of emergency at the U.S.-Mexico border, the White House interpreted wide latitude in this law to impose tariffs. When in reality, the IEEPA has traditionally been used to impose economic sanctions on people, businesses, and governments involved in illicit or nefarious activity. Most would agree it was not designed as an economic weapon in immigration politics.

In much the same way, any rational person would have a hard time arguing that automobiles and related products are a matter of significant national security. Yet, the Trump White House invoked this very clause in Section 232 of the Trade Expansion Act of 1962 to impose auto tariffs on a number of our trading partners. Such broad and unchecked authority accumulating to the Executive Branch is a dangerous precedent to set. Not only is it dangerous constitutionally, as it allows for greater power to accrue to one person, it is incredibly dangerous economically. We have documented the harm caused by trade barriers in single products and industries. Now imagine if tariffs were imposed on the imports of all goods and services. The economic impairment would be unparalleled. This brings in to focus the current U.S. – China trade war, which we discuss at length in our latest View from Here series, “When the Music Stops, Who’s Going to be Left Holding the Bag?”. Now armed with this background knowledge of tariffs, we hope you find our evaluation in that paper more illuminating and compelling.

DISCLOSURES

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This report is a publication of Aaron Wealth Advisors LLC. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication, are subject to change, and may not be the opinion of Aaron Wealth Advisors.

*Information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional adviser should be consulted before implementing any of the strategies or options presented.

*Information is not an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*All investment strategies have the potential for profit or loss. The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.