Introduction

Everyone has heard them ad nauseam throughout their lives, from parents or teachers or a professional mentor, so much so that they are routinely dismissed as white noise or adult condescension:

• There are two sides to every story, and the truth lies somewhere in the middle

• Treat others as you would like to be treated

• Perception is reality

• Never judge a book by its cover

Such axioms are ubiquitous because the values they impart – common decency, empathy, mutual respect, critical thinking – are so foundational to the productive, open, and thoughtful exchange of ideas and interactions that drive society forward. Today, however, one could make the argument that they are slowly becoming a cultural “vestigial tail” left over from a bygone era. Most would likely concede that our current public discourse demonstrates, at least to some meaningful degree, a deviation from what would normally be considered productive dialogue. Without doubt, the root causes that have evolved to shape today’s climate are varied and complex. Attempts to rationalize the key triggers are numerous but routinely inadequate, with the main culprits often attributed to social media, growing distrust of “elite” classes and institutions, seismic changes to the business model of a deteriorating news media industry, falling participation in organized religion, generational value shifts, among others. The goal of this piece, however, is not to construct a sequence of events that led to this point or propose solutions or wax poetically about yesteryear. While important in many respects, it is not germane to our work as investors. Rather, we first acknowledge and accept a key reality of our current landscape – that no issue, no matter how vitally important, is off-limits to politicization, tribalism, and narrative. The next step, which is our primary goal, is to identify how such an environment influences the worlds of economics and markets.

A compelling narrative, often in tandem with a convenient bending of the truth or a slight obfuscation of self-interested motives, has always been an omnipresent, well-understood part of the human condition. In fact, the argument could be made that it has been both beneficial and necessary for the advancement of complex society, essentially greasing the wheels for action and progress. Existing within the same circles though were institutions that served as societal guardrails – framers of public discourse on which the public relied to present an unbiased view and act as a deterrent against the malevolent intentions of unscrupulous actors. Until somewhat recently, the press and news media – our “Fourth Estate” – had a vast legacy of working tirelessly and without agenda to investigate and uncover crucial facts, which were often used to challenge the narrative espoused by key decision-makers. An informed citizenry could then productively debate the most appropriate policies and solutions for moving forward.

Today, on the other hand, narrative is king. As if in reverse order, the narrative is determined (often for political or ideological gain) and then buttressed by aligned media outlets, misleading facts lacking context, half-truths, omissions, or outright fabrications. Unsurprisingly, this practice is not unique to any political or ideological affiliation. The real world is a messy and chaotic place that requires a nuanced and thoughtful approach to understanding it. Narrative, however, is antithetical to such an approach, with its crude oversimplification of complex topics. When weaponized politically, the close but deep chasm between opposing factions grows deeper and polarization intensifies. For instance, one would assume that the sheer human suffering and economic destruction inflicted by a global pandemic would rally people around a sense of common humanity and lead to a unified societal response impervious to political or ideological manipulation. Instead, it appears that such an environment has led to an opportunity for narratives to influence an ever-greater degree of decision-making and behavior.

In the ensuing sections, we turn our attention to a subset of narratives which warrant detailed scrutiny, given their potential implications for our outlook and client’s portfolios. It would be easy to accept at face value the ebullient optimism of a post-Covid world, shared by many, that forecasts a Goldilocks environment for markets – i.e., a period of high growth, low rates, and low inflation. However, we prefer to operate sans rose-colored glasses and believe there is a material probability that the next 10 years will look very different from the last 10 years. This is not to say we are pessimistic about the future by any means, but rather, more accepting of a vastly different set of circumstances that can alter the path ahead. To that end, we analyze the current landscape with a critical, unbiased eye to distinguish unsupported narrative from facts. As we have discussed several times in the past, markets often expose the perceived “wisdom of the crowd” to be a dangerous narrative dressed up in sheep’s clothing.

Narrative 1: Corporations & the Wealthy Need to Pay Their Fair Share

Part I – What Exactly Constitutes a Fair Share?

Thus far into his first year in office, President Biden has been working to deliver on a key policy plank of his campaign, namely economic equality. Included in the White House’s $6 trillion budget outline are proposals for providing additional benefits for families (childcare, paid leave, tax credits), increasing access to education by reducing or eliminating costs entirely, transitioning the country away from fossil fuels, investing in national infrastructure, broadening access to social safety net programs, adjusting the length and amount of unemployment benefits, and creating good, well-paying jobs. While these are certainly admirable pursuits in isolation, the totality of potential impacts must be considered when evaluating costs and benefits. These policies represent a fundamental reshaping of the government’s role in the economy and would require a massive expansion of federal spending on a scale not seen since World War II. The budget request calls for total spending to grow to $8.2 trillion by 2031 and estimates that deficits will run above $1.3 trillion a year over the next decade. Therefore, funding this plan will necessitate enormous increases in taxes, national debt, or a mix of both if outlays are not slashed elsewhere. With mandatory spending on entitlement programs chewing up roughly two-thirds of the federal budget and national defense accounting for another 15%¹, cuts to the remaining discretionary budget will be of little help. Understanding this reality, the administration is seeking an historic revamp of tax policy.

The tax hikes are being marketed to the public as a long-overdue, righteous quest to make “corporations and the wealthy pay their fair share.” This narrative, while a dependable applause line in speeches, is so powerful because it misleads the audience into assuming as true the central premise – that is, corporations and the wealthy do not currently pay their fair share. The message was amplified further in June when ProPublica began reporting on the leaked IRS tax returns of wealthy and notable U.S. citizens. Using a contrived measurement they called the “true tax rate” – calculated as income taxes paid divided by net worth – the journalists claimed these documents unearthed strong evidence that the rich are wildly undertaxed. However, the U.S. does not (yet) have a wealth tax or a tax on unrealized gains, so reporting a “true tax rate” calculated in such a manner strikes us a disingenuous evaluation of the facts.

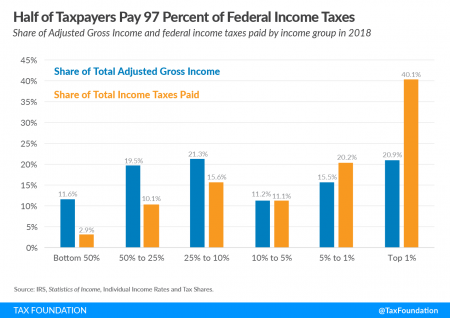

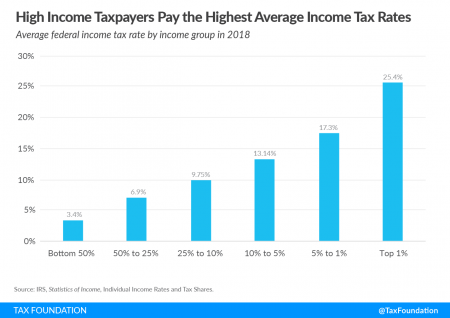

Federal data on income and taxes is published regularly, and we assume most of our readers will be familiar with these trends overtime. So, with minimal elaboration, we will simply share the latest available data from the Tax Foundation (see charts nearby).² This data was released in 2021 for tax year 2018, the first full tax year following the 2017 Tax Cuts and Jobs Act. The Top 5% of U.S. taxpayers by income, those with AGI of at least $217,913, earned 36.4% of total income and paid 60.3% of all federal income taxes. The Top 1% – with AGI of at least $540,009 and one of the groups targeted by the administration’s tax increases – had a 20.9% share of total income but paid over 40% of all income taxes.

Figure A: Income, Taxes, & Effective Rates²

For reference, the minimum Adjusted Gross Income for returns to fall into each percentile is: Top 1% – $540,009; Top 5% – $217,913; Top 10% – $151,935; Top 25% – 87,044; Top 50% – $43,614.

Part II – Biden’s Tax Agenda & Associated Impacts

Let’s delve into a few specific policies currently being debated in Congress. Below are some of the major changes to the tax code that the Biden Administration is pursuing³:

i. increase the top marginal income tax rate from 37% to 39.6%

ii. increase the long-term capital gains and qualified dividends rate to match the ordinary income rate (from a max of 23.8% to 39.6% as

above)

iii. impose the 3.8% Medicare tax on all income – wages, capital gains, and investment income – for households making $400,000 or

more (effectively raising the top marginal income, capital gain, and qualified dividend rate to 43.4%)

iv. eliminate the step-up in cost basis for transfers of appreciated assets by gift or death

v. treat transfers of appreciated assets by gift or death as a taxable event (with a few exclusions)

vi. force capital gain recognition on transfers of assets into, and distributions in-kind from, irrevocable trusts, partnerships, and non-corporate

entities

vii. elimination of lack of marketability or control valuation discounts for asset transfer into irrevocable trusts

viii. increasing corporate tax rates from 21% to 28%

ix. work with OECD countries to set a global minimum tax rate

We want to emphasize upfront that the following evaluation is not a political critique in any way, but rather an assessment of the likely financial impacts and incentives resulting from these proposals. Changes in marginal tax rates assessed on various income sources can be (and should be) debated intelligently between reasonable people. But regardless of whether rates are high or low, at least everyone has known since the early 1900’s – when the 16th Amendment was ratified and gave Congress the power to levy taxes on income – that they will have to pay taxes on the income they earn and can plan accordingly. However, the proposed elimination of the step-up in cost basis and treatment of transfers of appreciated assets by gift or death as a taxable event are fundamental changes to the rules of the game that unfairly impair the long-term planning required for successful financial outcomes.

Below is one example of how these policies could wreak havoc on underserving taxpayers. While President Biden has not formally put forth a reduction in the estate tax exemption, Bernie Sanders – currently chairman of the Senate Finance & Budget Committee – has proposed legislation that would slash this exemption to $3.5 million per person (from the current $11.7 million in 2021) while also enacting higher progressive tax rates. As such, we use these assumptions in the following scenario.

Hypothetical Scenario: Dr. Jane Doe is an entrepreneur who started a small medical device business 10 years ago after retiring from a successful career as an orthopedic surgeon. After showing early promise, she continued reinvesting in the company to facilitate its growth and distributed to herself only a modest amount of earnings needed to meet the living expenses of her family. Dr. Doe has explored various estate and succession planning strategies for the business – such as GRATs (Grantor Retained Annuity Trusts) and other irrevocable trusts – but has been unable to execute any because she lacks the personal funds needed to satisfy the tax obligations that would arise under the new tax regime. Unfortunately, she passes away unexpectedly before any plan can be put into place. Dr. Doe owns 100% of the company, which is valued at $15 million and has a $0 cost basis. Besides the business, her estate consists of approximately $3 million of marketable securities with a cost basis of $1 million. She is survived by a son, her only heir.

Hypothetical Result: Under the above tax policy proposals, the entrepreneur’s estate would have a total federal tax liability of:

• Capital Gains Tax on Business = $6,076,000 (43.4% tax on $15 million of appreciation minus $1 million capital gain exemption)

• Capital Gains Tax on Marketable Securities = $868,000 (43.4% tax on $2 million of appreciation)

• Remaining Taxable Estate = $7,556,000 ($11,056,000 estate after capital gains taxes minus $3.5 million estate tax exemption)

• Estate Tax = $3,400,200 (45% tax on remaining $7.556 million taxable estate)

• Total Federal Tax Liability = $10,344,200 (effective rate of 57.5%)

After using the $3 million of marketable securities, her estate would still owe over $7.3 million of additional federal taxes. Assuming her son is not able to pay this tax bill on his own, only two options remain: 1) sell the company immediately, possibly at a significantly reduced valuation; or 2) defer the tax liability and endure higher costs, potential tax liens, and difficulty obtaining future business financing. For context, under today’s policies, the son would receive a step-up in cost basis for all assets to fair market value, and the total federal tax liability would be roughly $2.87 million. This figure is still a high estimate though because, in the current tax regime, she would not be financially precluded from those estate planning techniques that become too costly to implement under the above proposals.

Recently, we have discussed the inherent contradiction that arises when the goal of raising more federal revenue is pursued by hiking the long-term capital gains rate to over 43%. Studies, such as one released by the Tax Foundation, estimates that this proposal would shrink federal tax revenue by $124 billion over 10 years.⁴ Economists of all stripes agree that the revenue-maximizing rate is somewhere between 15% to 28%. But why let unbiased data and expert studies get in the way of a good narrative…

It is important to keep in mind that these proposed rates are for federal taxes only, and do not include state or local taxes. Top earners in states such as California, New York, and Illinois would see their income and capital gains rates balloon to 56.7%, 54.3%, and 48.4%, respectively. On the corporate side, the average combined federal and state income tax rate would rise from 25.8% to 32.4% – meaning U.S. companies would face the highest combined tax rate of all OECD countries [The Organization for Economic Co-operation and Development (OECD) is an intergovernmental economic organization with 38 member countries, founded in 1961 to stimulate economic progress and world trade]. The average combined rate for OECD countries this year is 23.1%, excluding the U.S. Unfortunately, the tax pain doesn’t stop there because corporate income is double taxed in many countries. According to the Tax Foundation, “Before shareholders pay taxes, the business first faces the corporate income tax. A business pays corporate income tax on its profits; thus, when the shareholder pays their layer of tax they are doing so on dividends or capital gains distributed from after-tax profits. The integrated tax rate on corporate income reflects both the corporate income tax and the dividends or capital gains tax.

Joe Biden’s proposal to increase the corporate income tax rate and to tax long-term capital gains and qualified dividends at ordinary income rates would increase the top integrated tax rate on distributed dividends to 62.73 percent [from 47.47% in 2021], highest in the OECD [2020 average of 41.6%].”⁵

When viewed all together, one could reasonably conclude that such confiscatory taxes have the power to disincentivize the entrepreneurial spirit which drives our economy forward through job creation and value generation. Can anyone rationally justify this as “fair”? And do such policies truly benefit the people for whom many politicians proclaim to advocate? As discussed in Part III, it appears highly unlikely.

Part III – The Backdoor Approach to Soaking All Taxpayers: A How-To Guide

As a candidate and as president, Joe Biden has repeatedly promised that no person making under $400,000 a year would see an increase in taxes. Since his election this has shifted somewhat, from “no person” to “no family.” The distinction is significant from a tax perspective, but we will give him the benefit of the doubt that his intent was consistent. What cannot be ignored, however, is the backdoor approach that the administration plans on employing to increase taxes on everyone making under $400,000 a year. According to budget documents, Biden plans on letting the tax cuts on low- and middle-income earners, enacted in the 2017 Tax Cuts & Jobs Act, expire as scheduled in 2025. This wouldn’t occur until his first year of a potential second term, when he is safe from facing reelection, so concerned voters should be aware in advance.

Given Biden’s tenure as Vice President for eight years, one might assume he would carry forward the beneficial insights gleaned from policies enacted during the Obama administration. Alas, it appears such institutional knowledge may have been either forgotten or ignored. According to Mr. Obama’s 2015 Economic Report of the President:

“When effective marginal rates are higher, potential projects need to generate more income if the business is to pay the tax and still provide investors with the required return. Businesses will therefore limit their activities to higher-return projects. Thus, all else equal, a higher effective marginal rate for businesses will tend to reduce the level of investment, and a lower effective marginal rate will tend to encourage additional projects and a larger capital stock. Increases in the capital available for each worker’s use, also referred to as capital deepening, boost productivity, wages, and output.”⁶

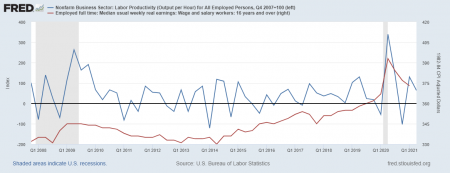

While the 2017 tax legislation was far from perfect, it was a strong step in the right direction towards making the U.S. system more globally competitive. Over the three years spanning 2018 to 2020, U.S. multinational companies repatriated nearly $1.6 trillion of offshore earnings. On an average annual basis, this represents an 18% jump relative to the decade covering 2008 to 2017.⁷ Foreign earnings brought back to the U.S. are often reinvested domestically in American jobs, wages, projects, and capital stocks. As a result, prior to the pandemic-induced recession, productivity and real wages boomed to levels higher than those seen in 2007, just before the Great Financial Crisis (see nearby chart).

We will address the broader knock-on effects in more detail later, but this alone underscores an immutable economic reality: there is no free lunch. So too under Biden’s tax-and-spend policy agenda, everyone ultimately pays.

Figure B: Productivity and Real Earnings

Narrative 2: Inflationary Pressures Are Transitory

Since the beginning of the Covid pandemic, the federal government has passed roughly $5.4 trillion in economic stimulus. Now, quickly on its heels comes budget proposals that will increase spending by more than $6 trillion a year. When viewed together with historically accommodative monetary policy of near-zero interest rates and massive asset purchase programs, as well as a global economy emerging from pandemic shutdowns, it should be no surprise that inflation has soared above 5% year-over-year for the past few months. Supply chain bottlenecks, labor shortages, and surging commodity prices continue to exert upward pressure. Businesses are warning that supply chain issues may run through 2023 and forecast higher prices over the rest of the year. September will prove to be an important month for the job market as enhanced federal unemployment benefits are set to expire.

Employment is unique in that it is by nature a matching problem quite sensitive to financial incentives. As such, structural shifts in the labor market that occur both during and coming out of a recession – as well as government policies implemented to deal with said recession – can result in longer-term dislocations. This is evident in the recently published August jobs report, which was a major disappointment. Despite robust growth in GDP, employment data appears stuck. Net new jobs increased by 235,000 versus consensus estimate of 733,000. The labor force participation rate remained flat at 61.7%, well below January 2020’s pre-pandemic peak of 63.4%. And, according to the National Federation of Independent Business’ August 2021 survey, 50% of firms could not fill available jobs, as job openings continue to outstrip the number of unemployed workers. To attract workers, employers are raising wages and providing financial inducements just to interview. Average hourly wages increased 17 cents in August, equivalent to a 6.9% annualized rate.⁸ The root cause of this is likely a mix of several prevailing conditions that are creating financial disincentives to work, including enhanced unemployment benefits, the expansion of other cash or in-kind benefits (such as the child tax credit and food stamp program), and 7 straight months of declining real wages due to rising inflation. With many of these factors persisting past the expiration of enhanced federal unemployment benefits, as well as much of the world beginning to reimpose pandemic restrictions, it is quite possible that the current structural issues roiling labor markets and supply chains may linger longer than anticipated.

Jerome Powell and the Fed continue to assure markets that this is only a transitory phenomenon due to the low pandemic base levels of 2020. While this very well could be the case, the risk of being wrong is severe. Should inflation continue to overshoot, monetary policy would need to be quickly tightened by raising interest rates and tapering asset purchases, which could come as a large shock to markets if not expected or properly communicated. A fledgling economic recovery that is thrust into a period of sustained increases in interest rates, inflation, and tax increases runs the risk of creating a stagflationary environment – or slow growth coupled with rapidly rising prices – like that experienced in the 1970s. And after over 10 years of historically accommodative fiscal and monetary policy, the levers available to pull to combat such an environment could prove ineffective. We are optimistic that the central bank can thread this needle though as a consensus is building to begin tapering asset purchases soon. In the best-case scenario, politicians in Washington will remove – or more likely fail to pass – poorly conceived legislation from the equation and allow a budding economic recovery to bloom.

Narrative 3: The Great COVID Re-Opening

Conclusion & Outlook

We conclude with our final narrative that happens to tie neatly into the summation of our outlook. In our view, the current economic and market landscape should provide fertile ground for a robust recovery that began after the world emerged from Covid shutdowns. If not already, it will soon be apparent to most that this virus is something we will need to learn to deal with for the foreseeable future. As we have seen with the rapid spread of the Delta variant, quick and complete eradication is highly unlikely, so it is imperative that we keep adapting and managing through it. The world has already proven that this can be accomplished, however. In what will perhaps be considered one of the greatest achievements of our collective human ingenuity and adaptability, we navigated our way through months of social and economic lockdowns, developed and began distributing a vaccine in less than a year, and successfully revamped the way we work and live. More than anything, this should be a resounding source for optimism. If the distortions caused by the pandemic prove to be short-lived, this narrative has the potential to live up to the hype.

The most significant risks to this case, in our opinion, are as follows:

• Implementation of recently proposed tax policies

• Significant and sustained expansions of federal spending, benefits, and regulation

• Persistent and rising inflation resulting in reactionary monetary policy

• Reversion to economic shutdowns due to spikes in Covid case rates

• Escalation of tensions between the U.S. and China coupled with a deterioration in American relationships with key allies

• Irrational exuberance arising from a wide-spread, singular view that markets will only go up

We continue to monitor with heightened diligence this last risk as it is a consistent source of concern and befuddlement. Flush with unprecedented fiscal and monetary policy, U.S. investors continue to push equities to ever-higher record levels. The collective psychology is evident – stocks will go up, they only go up, they must go up. Every momentary dip is viewed as a buying opportunity. This “buy-the-dip” philosophy might be the most successful and longest running trading strategy in market history. And with the amount of capital now sloshing around the economy, the investor attitude of TINA – There is No Alternative (to equities) – has become a self-fulfilling narrative driving markets. As history has demonstrated time and again though, crowded momentum trades always collapse, often in spectacular fashion. The only unknowns are when it will happen and how bad the damage will be. This is not to imply that today’s valuations and levels are in bubble territory, but rather to highlight the need for caution and prudence given the singular, momentum-driven directionality of market trading.

From an asset allocation perspective, we have slightly reduced our tactical overweight to U.S. equities given the frothy valuations and overbought technical signals. By trimming this overweight in favor of International and Emerging Market equities, we find greater medium-term value if equities climb higher and more robust downside protection if equity markets correct. As we have mentioned previously, Emerging Markets especially tend to outperform coming out of a recession historically. However, the success of this decision has the potential to be threatened by delayed vaccination rollouts and pandemic responses in less developed countries. In addition, isolated political upheavals in Asia and South America could pose further risks to Emerging Markets. A key focus will be on the progress of developments in China, especially the social and economic reordering currently underway.

On the fixed income side of the portfolio, we have maintained and tweaked our positioning to reduce sensitivity to interest rates along with being selective in our credit-quality allocations. Specifically, our goal is to ensure we are adequately compensated for the duration and credit risk taken. Given the threat of significant increases in income taxes, Municipal Bonds have the potential to be more heavily favored going forward. Lastly, we are currently evaluating the tactical Agency/Mortgage-Backed Security strategy we began entering in the summer of 2020 as discussions around Fed asset tapering gather steam.

Across public markets, persistent valuation premiums and low interest rates have increasingly limited the availability of attractive opportunities. For this reason, we remain focused on sourcing and uncovering interesting solutions in the private markets, as we believe they offer a better use of the portfolio risk budget and a more attractive entry point for long-term return prospects relative to public markets.

Sources

¹Source: White House Table 3.1 – Outlays by Superfunction and Function: 1940-2026 https://www.whitehouse.gov/omb/historical-tables/

²Source: Tax Foundation – “Summary of the Latest Federal Income Tax Data, 2021 Update” 2/3/2021 https://taxfoundation.org/federal-income-tax-data-2021/

³Source: White House Fact Sheet: The American Families Plan released 4/28/2021 https://www.whitehouse.gov/briefing-room/statements-releases/2021/04/28/fact-sheet-the-american-families-plan/

⁴Source: Tax Foundation – “Top Combined Capital Gains Tax Rates Would Average 48 Percent Under Biden’s Tax Plan” 4/23/21 https://taxfoundation.org/biden-capital-gains-tax-rates/

⁵Source: Combined corporate income tax data for U.S. and OECD countries sourced from Tax Foundation “Combined Corporate Rates Would Exceed 30 Percent in Most States Under Biden’s Tax Plan” 4/1/2021 https://taxfoundation.org/combined corporate-rates-biden/

⁶Source: Economic Report of the President 2015 https://www.govinfo.gov/app/collection/ERP/2015

⁷Source: Bureau of Economic Analysis – Table 4.2. U.S. International Transactions in Primary Income on Direct Investment released 6/23/2021. Data period 1/1/2008 –12/31/2020. https://apps.bea.gov/itable/itable.cfm?reqid=62&step=1

⁸Source for employment data in this section: Bureau of Labor Statistics, U.S. Department of Labor – The Employment Situation August 2021 released 9/3/2021 https://www.bls.gov/news.release/pdf/empsit.pdf

DISCLAIMER

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This report is a publication of Aaron Wealth Advisors LLC. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change.

*Information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional adviser should be consulted before implementing any of the strategies or options presented.

*Information is not an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*All investment strategies have the potential for profit or loss. The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.