It’s just that easy, folks. Step One: After a sharp sell-off at the end of 2018, the Fed reverses monetary policy from “disciplined rate normalization” to “wait and see”. Step Two: Sprinkle in the continuation of robust economic data, especially in jobs and wages. Step Three: Mix in inflation figures that remain below the Fed’s target. And, voila! A headline-driven market now has all the ingredients it needs for a dramatic rebound and the best 4-month start to the year in the past two decades. The S&P 500 returned 18.25% from January 1st to April 30th of 2019; for comparison’s sake, the U.S. market hasn’t seen a rally like this to start a year since 1998 when the S&P 500 returned 15.10% through April. Even the lagging international markets got in on the action, with International Developed Market equities returning 13.07% and Emerging Market equities up 12.23%. What about Real Estate? Small-Caps? Master Limited Partnerships? Yes, those too all produced double digit gains.1 Throughout this time period, levels consistently tested or reached new, all-time highs.

It’s astounding how quickly a market driven by coalesced sentiment can change course and roar the other way. Not too long ago in December, there was ample discussion that the party was over. The music had stopped, and we were heading into a bear market along with an impending recession. In our early January edition of this series, we disagreed with that notion. We argued that the negative turn in sentiment was way overdone. The economy continued to demonstrate its strength and signal there was still room to run. In addition, the Fed was already hinting that their December policy statement was far too rigid and would likely shift to a more dovish stance.

All this is to say, we understand the rebound. The market overreacted and would likely correct itself. But this? The way equities have traded this year could make even the staunchest and resolute bear lose his mind from banging his head against the wall. We have noticed a consistent pattern during intraday trading when the market finally appears to be losing steam. It goes like this: 1) negative news or data is released; 2) the market justifiably and rationally trades lower; 3) dip-buyers swoop in and rally levels back to flat or positive by the end of the day. It has been a very profitable strategy as well as an approach that’s likely being employed by a significant portion of investors. Everyone’s a perma-bull these days. Risk assets won’t and can’t go down, they say. It’s exuberant. In our opinion, however, it’s incredibly dangerous. The music will eventually and most certainly stop, and we don’t want to be in a position where we’re left holding the bag after it inevitably turns. Color us cautious and concerned. When the market crowds into a “can’t-lose” strategy, the historical unwinding or breakdown of such a trade has had some devastating financial consequences.

To say that the current environment isn’t accounting for the true amount of uncertainty on the horizon would be a laughable understatement. The market appears to be evaluating the biggest risks to continued expansion – a breakdown in trade negotiations between the U.S. and China coupled with an escalation of retaliatory measures, the 2020 U.S. presidential election, a bungling of the Brexit process, a hastening of the slow-down in Europe and China – as if the most optimistic resolution will inevitably come to fruition.

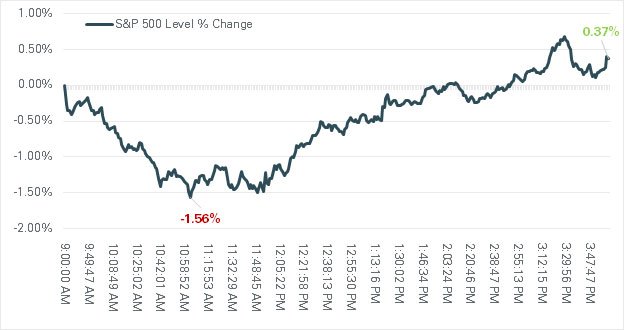

We thought some level of rationality was finding its way back into trading patterns recently in the first full week of May. President Trump announced that additional and increased tariffs on Chinese imports would take effect on May 10th. Trade negotiations between the two countries temporarily halted before resuming at the end of the week. No deal was reached by the deadline, though talks were described as “constructive”. As a result, the expanded tariffs went into effect that Friday, and the administration publicly announced that even more tariffs could come in the next 3-4 weeks. Each day that week the market opened lower and continued its declines throughout the morning, sometimes getting quite nasty. Without fail though, the dip-buyers came to the rescue, bidding up prices until the market closed with meager losses or sometimes modest gains. For example, on May 10th, the S&P 500 was down approximately 1.6% intraday, only to then rally and end up 0.4% at the close. This was despite all the obvious negative news of increased tariffs, with potentially more to come, and promises by China to retaliate in kind. The accompanying chart shows the movement of the S&P 500 on that day for illustrative purposes. The following week saw a severe and broad-based selloff of 2% – 3% across equity markets on Monday. We’re hopeful this is indicative of a willingness to reset expectations and reprice the material risks evident to us across the globe. But we’re not going to hold our breath.

Chart 1: Intraday Percent Change in the S&P 500 Index on May 10th, 2019 (Source: YCharts)

After learning a difficult lesson trading currencies, notable speculator and economist, John Maynard Keynes, summarized this reality quite eloquently: “The market can stay irrational longer than you can stay solvent.” We couldn’t agree more. We’ve reiterated several times before that we maintain no desire to step in front of a bulldozer to pick up a couple extra nickels – which is the feeling conveyed to us in the current environment. However, should the major risks currently threatening the market dissipate or dissolve, we want to be positioned to capitalize on upward movements. The question that follows becomes: “How can we remove meaningful risk from portfolios in down markets while retaining desirable risk in up markets?”

Instead of fighting against the powerful current of prevailing momentum or attempting the impossible feat of timing the top of the market, we decided to get more creative with portfolio construction. Our goal was to develop a basket of thoughtfully designed (but often poorly implemented) investment instruments that could: 1) closely mimic equity exposure when markets are positive, 2) provide a level of protection or even benefit from negative equity returns, and 3) free us from the Herculean task of trying to divine exactly when this current bull run will ultimately come to an end. In our opinion, we successfully achieved that goal and arrived at a “risk-conscious” equity portfolio that is positioned well for the varying environments we could encounter over the coming years. For the remainder of this paper, we will highlight some specific risks that, in our view, warrant serious consideration and close attention. Additionally, context and an overview of our pivot in equity portfolio construction will be discussed.

HOW “NEW” IDEAS AND POLITICAL POLARIZATION THREATEN LONG-TERM ECONOMIC PROSPERITY

Risks in International Trade Policy

We would like to begin this section by stating upfront and without ambiguity that our analysis is not intended to espouse any political view, support the furtherance of any political ideology, or reflect the personal political leanings of any member of the firm. It is our job to remain apolitical in the service of our clients and objectively assess the economic impact of prevailing policies. Doing so allows for the impartial evaluation of potential risks to client portfolios and appropriate maneuvering to protect against those risks. To be sure, the threats to long-term economic prosperity span the political spectrum, as will be seen shortly.

Back in the September edition of this series (“The Good, The Bad, and The Ugly”), we highlighted the danger of Congress gradually ceding more and more trade policy discretion to the Executive Branch over time. Allowing, if not encouraging, the accumulation of such unchecked power can surrender the ability to tame the worst impulses of any single administration. Unfortunately, this is the exact situation in which the U.S. has found itself since the last presidential election. A dramatic rightward shift of the current administration and Republican Party – the party historically associated with free trade and open markets – towards mercantilism and protectionism has subjected the economy to failed and harmful ideals. In the previously referenced paper, we recounted an historical example of the severe ramifications these economic policies can have when implemented:

Those involved would benefit from the lessons learned after the passage of the Smoot-Hawley Tariff Act of 1930. The tariffs enacted with this law were the second highest in 100 years and led to a significant reduction of both American imports

and exports. As a result, economists generally agree that this protectionist law exacerbated the Great Depression, rather than saving jobs and the economy. The overwhelmingly negative effects of tariffs and protectionist trading practices are settled economic science, in our opinion, and should be avoided.2

If that wasn’t concerning enough, the lack of stability and clarity in this administration’s trade policy exposes the global environment to ill-advised presidential whims decreed by Tweet. Such hostage taking has injected unneeded volatility and uncertainty into capital markets. Investors’ only recourse is to await the next breaking headline which details the trade policy du jour, attempt to decipher the latest intentions of the administration, and scramble to adjust accordingly. In our opinion, the potential risk of poor policy strategies is greatly compounded by the uneven and unintelligible execution of those strategies.

While the U.S., Mexico, and Canada have reached some sort of agreement in the renegotiation of NAFTA and our European allies have been willing to work with the administration to find mutually beneficial trades agreements, the process through which these understandings were extracted emphasize just how unstable they truly are. If at any moment any administration can force trading partners back to the negotiating table with threats of tariffs, what weight do those deals carry? Can any party to the agreement rely on their counterparts to uphold their end of the bargain? The enforceability of contracts is a hallmark characteristic of developed, evolved markets. Without confidence in this enforceability, economies break down and regress. One must keep in mind that a resolution to these disputes does not imply that the resolutions themselves were advantageous or value accretive. Real costs have been artificially imposed on trade which are borne by American businesses and consumers. Yet despite, not because of, these flawed policies, the economy has continued to expand strongly.

The situation is markedly different when it comes to the escalating trade war with China, however. China is not an ally but a determined and powerful rival. We’ll refrain from reiterating the sequence of events in the ongoing dispute as we have discussed them in detail earlier in this paper and others prior. Suffice it to say that the administration’s current approach on this front – while admittedly bringing China into negotiations – threatens not only the U.S. economy but the global economic order. Chinese international investment, through policies such as the Belt & Road Initiative, demonstrate clearly their level of commitment to global economic dominance. When combined with the authoritarian state’s ability to unilaterally direct the investment priorities of ample public and private assets, one begins to see just how formidable of a foe China could be. Our two economies are inextricably linked, presently. In our opinion, however, the current strategy of continued threats and increasingly punitive tariffs could spur a fight in which no country is prepared to engage. By not providing an avenue through which the Chinese government can portray strength domestically, both parties lose if China retreats to save face and prepare for economic battle. In the short run, the American economy will continue to pay the costly price of expanding tariffs, not China as several machinations are at their disposal to remain a leading global exporter (e.g. currency manipulation and private sector subsidies). In the long run, and far more concerning, would be an economic Cold War that decouples and realigns the global order along two poles: the U.S. and its allies on one side, China and the countries under its thumb on the other. Countries around the world would be forced to choose sides, and those that have received considerable investment from China – through programs like the Belt & Road Initiative – would face mounting pressure to succumb to financial incentives. The fallout from this conflict would result in painful reductions of economic output, gross misallocation of capital, and an unraveling of the global efficiencies on which our world is built. The very foundation of the global economy could split and crumble.

Instead, a less perilous and more fruitful approach might be a convincing argument for the benefits China could derive from further assimilation into the liberalized economic system. The explosive growth China has experienced over the past two decades can be justifiably attributed to the incremental steps toward full integration that they have already taken, such as joining the International Monetary Fund and World Trade Organization, to name a couple. We applaud the desire to hold China accountable to global norms and practices – particularly in areas like intellectual property/technology protection, fair competition for international businesses, and government interference in markets. However, this can be better accomplished by demonstrating the economic success that comes from further liberalization. At the same time, this strategy allows government leaders and the faction of officials already inclined toward opening the economy to sell these changes from a position of strength. Monumental leaps of progress in geopolitics are rare and extraordinary but that shouldn’t mean incremental progress is viewed as failure, especially when the alternative leaves everyone worse off.

The ripple effects from this standoff have already spread across much of international developed and emerging markets further compounding the headwinds of a generally strong U.S. dollar, slowing growth, and a “risk-off” mentality driving investment outflows. That said, due to relatively attractive valuations, investors are beginning to reconsider these markets from a longer-term perspective. As the situation develops, we will determine if the compressed valuations and economic growth prospects of these markets present opportunistic entry points. At least one headwind which has plagued these markets recently should subside as we believe the U.S. dollar strengthening cycle will begin to wane in severity. However, one must weigh the likelihood of a positive resolution to the trade impasse and be willing to stomach short-term, heightened volatility.

Risks in Domestic Policy

We now turn to U.S. domestic politics, specifically the looming 2020 presidential election. Stump speeches and candidate platforms during an election cycle would not normally be a cause of concern as the most radical policy proposals are typically low probability events. Candidates with such ideas must first win their party’s nomination, next a general election, and then attempt to push legislation through both houses of Congress. Successfully passing through this gauntlet with the purity of the original policy intact is exceedingly difficult as external political forces inherent to the process dilute it at every stage, at least historically. In the end, the hard edges tend to be softened and pulled toward the ideological center.

What concerns us most about this particular election is not any individual candidate, per se, but the institutional shift leftward of the Democratic Party. With 23 candidates now vying for the nomination, each has jostled to outflank their competitors with an increasingly radical platform in order to rise above the crowd and emerge as the most progressive leader. Concurrently, either to project unity or appear diametrically opposed to the current administration, the rest of the party apparatus has coalesced around these ideas and internalized them as sacrosanct truth. Amplifying the reach and normalization of these proposals is the decentralization of media content and a variety of social networks – which give the loudest megaphone to a fringe minority and forcibly suppress the public expression of opposing thoughts. In turn, the resulting echo chamber hardens and affirms elected representatives’ belief that their platform aligns with the envisioned future supported by a majority of the electorate, regardless of the fact that this may only be the vision of a minority faction.

Elections are notoriously fickle and difficult to predict. Therefore, as investors, we must evaluate seriously the potential consequences of outcomes with material probability of occurrence. Given the current political landscape of vigorous polarization, the likelihood of U.S. federal policy jumping towards democratic socialism and becoming more volatile has grown substantially. In our estimation, the market is not accounting for this very real risk and uncertainty.

As wealth management fiduciaries, we have a fundamental duty and obligation to act in the best interests of our clients. It is imperative that personal beliefs and political opinions do not influence our decision-making process, as this could give rise to conflicts we strive to avoid. For this reason, our analysis is performed as an examination of financial impacts while setting aside the merit of moral, ethical, or societal outcomes (unless these too have knock-on financial implications). We view certain proposals as most dangerous to the economy and client portfolios, including Medicare for All, the Green New Deal, federal charters for American corporations, and an expansion of various other entitlements. Some gain more attention than others, but the overarching theme is an explosion of government spending and market intervention. These policies, if enacted as currently outlined, would cost trillions of dollars, require a dramatic increase in taxes on business and individuals, fundamentally alter our economic structure, and roll back market efficiencies which are value-additive. For instance, the Medicare for All initiative originally put forth by Senator Bernie Sanders and supported in principle by most presidential candidates, is estimated to cost approximately $32 trillion over the next ten years. To put this in perspective, the size of the entire U.S. economy in 2018 totaled roughly $20.4 trillion, according to IMF estimates. Doubling current tax rates on all corporations and individuals – the top income tax bracket rises from 37% to 74% – would still be insufficient to cover the price tag. In addition, this program (and similar proposals by others) contains language that would make it illegal to obtain or provide medical services in the private market. When a monopoly exists, public benefits derived from the efficiencies and innovation of competitive markets vanish, costs skyrocket, and incentives no longer drive value production. In a broader context, nationalizing a sector that constitutes a significant portion of the economy and is led globally by U.S. innovation would be detrimental to economic growth, in both the short- and long-run.

The above represents the effects of a single proposal, but several others carry similarly negative consequences. Cost estimates for the Green New Deal range anywhere from $51 trillion to $93 trillion and will require a complete overhaul of U.S. infrastructure. The point being, if even a few of these policies become law, the real costs experienced through economic loss, taxes, and government deficits would be unfathomable. With a national debt that already exceeds $22 trillion, an unprecedented acceleration of government spending will crowd out private investment and halt the efficient allocation of capital to productive enterprise. We are constantly dismayed by lawmakers’ inability or lack of fortitude to reign in runaway deficits, but it is consistent with a pattern of kicking the can down the road that has persisted since the 1990s.

It all started with a hedge fund, Long Term Capital Management (LTCM), that grew to over $120 billion in assets by utilizing an extraordinary amount of leverage. With several Nobel Laureates and legendary investors counted among its ranks, the firm wielded a reputation as “the smartest guys in any room”. Steller returns generated with seemingly minimal risk in the early years of the fund only served to validate this moniker. As a result, they were able to bully liquidity providers and lenders into supplying capital with remarkable terms. Competing banks that were desperate for the fund’s business eagerly offered capital without requiring the customary haircuts on posted collateral or evidence that LTCM’s assets could ever support these obligations. Even more surprising, this dynamic allowed for ultimate secrecy that ensured no outside party had any information about the fund’s positions or use of leverage. By 1998, the cracks of a flawed investment strategy began to show. Fearing that the imminent collapse of LTCM would result in market contagion and a financial crisis, regulators forced several Wall Street banks to bail out the failing fund. Ten years later, in 2008, a very similar story played out. The reckless use of leverage combined with limited understanding of the underlying risks inherent to the mortgage backed security market led to excesses that culminated in another financial crisis. In this instance however, instead of Wall Street banks coming to the rescue, they were the ones in dire need of a bail out by the U.S government and taxpayers. If sovereign governments across the globe continue to spend irresponsibly and accumulate debt burdens that cannot reasonably be serviced, they may find themselves in an all-too familiar situation. Who could bail them out though? Maybe some supranational organization such as the IMF, but we shudder at the thought of having to find out if that’s indeed possible. The only other alternative, in our minds, would be a reliance on monetary policy measures frequently employed by spiraling economies. As debt burdens reach unsustainable levels, the government reverts to printing money required to fulfill obligations. Hyperinflation ensues and, in real terms, the value of debt becomes “cheaper” to finance. This has never been a realistic solution, however, merely a stopgap that temporarily staves off the country’s inevitable default. Meanwhile, the public is left to contend with a hastening of economic deterioration that erodes quality of life standards. Ultimately, the duration and severity of the contraction is intensified as the government siphons off the value of the country’s remaining productive assets.

In our estimation, the Democratic priorities detailed in this section would be a continuation of the recent pattern and, sooner rather than later, lead to a U.S. economy stunted for the foreseeable future. Alas, proponents have begun to tout a new idea that claims to provide evidence this agenda is reasonable and economically feasible – Modern Monetary Theory (MMT). In overly simplified terms, MMT is a disparate set of macroeconomic theories unified around the idea that deficits are irrelevant to the economic health of countries which borrow in their own currencies, so long as inflation is muted. We won’t go into a detailed rebuttal of this theory for the sake of our readers. Instead, we will succinctly state our thoughts on the matter. To put it mildly, MMT is not grounded in economic reality as it equates to the notion that money is free. If money is costless, then it could not possibly be exchanged as a store of value. Should governments accept this theory as sound policy, the likely consequence would be a financial crisis. Slapping an erudite name on the failed practice of money-printing does not imply original thought or creative insight. But we never cease to be amazed by the opportunistic suspension of logic and rationality that politicians will employ if it supports their ability to continue a spending binge of someone else’s money.

“RISK-CONSCIOUS” PORTFOLIO CONSTRUCTION IN A WORLD WHERE RISK ABOUNDS

The risks outlined above can be loosely classified as binary in nature, meaning the resolution will likely be one of two potential outcomes. As an example, either the U.S. will reach a trade deal with China, or it won’t. A binary world requires creative and flexible portfolio construction that is properly positioned for whichever environment we find ourselves when an outcome is eventually reached. Recalling the opening pages of this paper, our goal was to develop a basket of thoughtfully designed (but sometimes poorly implemented) investment vehicles that could: 1) closely mimic equity exposure when markets are positive, 2) provide a level of protection or even benefit from negative equity returns, and 3) free us from the Herculean task of trying to divine exactly when this current bull run will ultimately come to an end. To that end, we arrived at a basket of derivatives which we aim to implement in portfolios as a partial replacement of clients’ U.S. equity exposure.

Derivatives often carry a negative connotation with the public due to misinterpretations of their inherent risk and historical examples of blatant misuse. Instructive case studies, like the 2008 Financial Crisis and LTCM, document the harm that can be done when these instruments are irresponsibly implemented. What is often missed is that these events represent only a small fraction of use cases. Because of their salaciousness and outsized negative effects, however, they are the ones most likely to be detailed in news coverage consumed by the public. The daily utilization of derivatives for risk management by banks, corporations, non-bank financial institutions, and investors do not provide the newsworthy content that media outlets crave because they are routine and banal. In contradiction to public perception though, the ability of oil producers to lock-in future sale prices for their volatile commodity – or banks to offset the credit risk of small business loans, or entrepreneurs to hedge the single stock concentration risk of their net worth – by harnessing the power of derivatives has dramatically improved the stability, efficiency, and value of global commerce. Because of these advanced tools, access to capital has broadened and is more affordable, corporate cash flows have become more predictable and visible, identifiable risks can be better quantified and managed, and the long-term investments needed for innovation have grown in feasibility and profitability. It is not a stretch to state that the development of derivative products, coupled with (mostly) thoughtful and responsible implementation, may be the driving force behind the exponential growth in wealth creation experienced during the industrial era. For this reason, we would be grossly negligent in the service of our clients if we did not leverage these effective risk management tools at our disposal.

We believe incorporating derivatives into our equity allocations will beneficially position portfolios for a variety of environments that may be encountered during this market cycle. As investors, our goal is to be compensated for the risks we take, and we are constantly searching for risks that might not be so obvious. The asymmetrical risk-return profile of intelligently designed derivatives depicts one arrow in our proverbial quiver. This arrow can be deployed to further our dual goals of mitigating the effects of negative outcomes and not sacrificing upside participation should risks dissipate. Given the current market landscape and potential threats we see on the horizon, a prudent approach is required to nimbly navigate such potentially hazardous waters. Traditionally, we would not highlight specific investments or strategies in this series but decided it was important to share. We ask readers to keep in mind that some characteristics of these investments will change with market conditions and are shown here for illustrative purposes only. We will consult with clients individually if such a strategy is suitable.

DISCLAIMER

*Aaron Wealth Advisors LLC is registered as an investment adviser with the Securities and Exchange Commission (SEC). Aaron Wealth Advisors LLC only transacts business in states where it is properly registered or is excluded or exempted from registration requirements. SEC registration does not constitute an endorsement of the firm by the Commission nor does it indicate that the adviser has attained a particular level of skill or ability.

*This report is a publication of Aaron Wealth Advisors LLC. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy and it should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the author as of the date of publication and are subject to change.

*Information contained herein does not involve the rendering of personalized investment advice but is limited to the dissemination of general information. A professional adviser should be consulted before implementing any of the strategies or options presented.

*Information is not an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein.

*Past performance may not be indicative of future results. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by the adviser), or product made reference to directly or indirectly, will be profitable or equal to past performance levels.

*All investment strategies have the potential for profit or loss. The firm is not engaged in the practice of law or accounting. Content should not be construed as legal or tax advice. Always consult an attorney or tax professional regarding your specific legal or tax situation.

*This material is proprietary and may not be reproduced, transferred, modified or distributed in any form without prior written permission from Aaron Wealth Advisors. Aaron Wealth reserves the right, at any time and without notice, to amend, or cease publication of the information contained herein. Certain of the information contained herein has been obtained from third-party sources and has not been independently verified. It is made available on an “as is” basis without warranty. Any strategies or investment programs described in this presentation are provided for educational purposes only and are not necessarily indicative of securities offered for sale or private placement offerings available to any investor.

- Source for paragraph data points: Morningstar Direct. Market indexes used to represent stated asset classes: S&P 500 = S&P 500 TR Index; International Developed Market equities = MSCI EAFE NR USD Index; Emerging Market equities = MSCI Emerging Market NR USD Index; Real Estate = MSCI ACWI/Equity REITS NR USD Index (15.25%); Small Caps = Russell 2000 TR Index (18.48%); Master Limited Partnerships = Alerian MLP TR Index (15.27%). Data shown is for the period 1/1/2019 – 4/30/2019 and is compared against the same annual calendar periods from 1998-2018. It is not possible to invest directly in any index. Past performance is no guarantee of future results.

- View From Here Series, September 2018: “The Good, The Bad, and The Ugly”